Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY:

- GLOBAL EQUITIES CONTINUE TO SLIDE OVERNIGHT

- SUPPLY DRIVES RECORD U.S. PRICE EXPECTATIONS: FED ECONOMIST (MNI INTERVIEW)

- OIL PRICES DROP AS COLONIAL PIPELINE RETURNS TO SERVICE

- CHINA TOP TRADE OFFICIAL NOT BEING REPLACED: MOFCOM

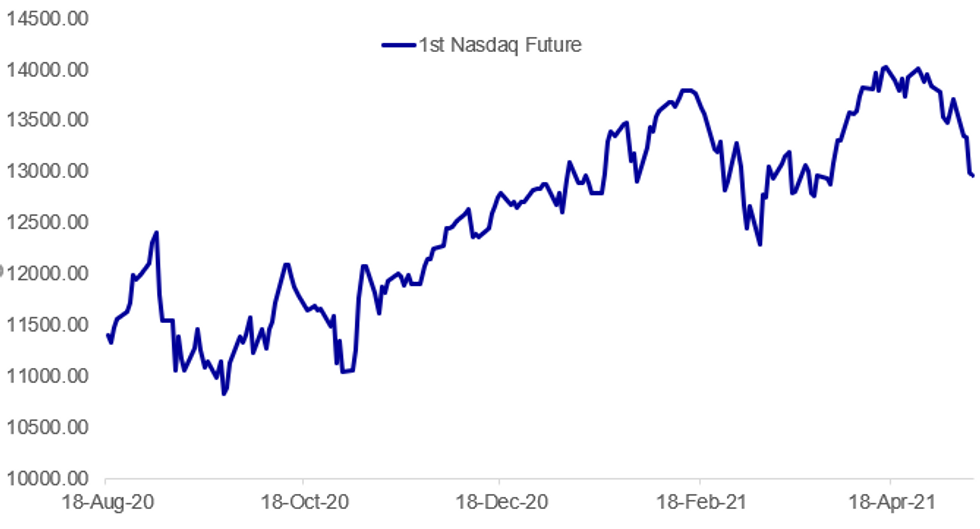

Fig. 1: Tech Stock Rout Continues

BBG, MNI

BBG, MNI

NEWS:

U.S. INFLATION (MNI EXCLUSIVE INTERVIEW): Supply disruptions have propelled firms' short-run inflation expectations to a record high 2.8% this month and may start feeding longer run views, Atlanta Fed policy adviser Brent Meyer told MNI on Wednesday. For full article contact sales@marketnews.com

ENERGY (BBG): Oil snapped a four-day gain as a key U.S. pipeline restarted and China said that it would push back against elevated commodity prices.West Texas Intermediate lost 1.3%, after closing Wednesday at a two-month high, while Brent fell. The Colonial Pipeline Co. -- a key source of gasoline for the East Coast -- is returning to service after a cyberattack last Friday. That'll bring relief to motorists after panic-buying emptied out some gas stations.

US-CHINA: Media suggestions that Beijing is considering replacing its senior economic point person with the U.S. are unfounded, a government spokesperson said Thursday. Referring to a report in the WSJ suggesting Vice Premier Liu He, who headed the 2019 trade negotiations with Washington, would be replaced by vice premier Hun Chunhua were untrue, Ministry of Commerce spokesman Gao Feng told reporters.

U.S. POLITICS (NY TIMES): The Biden administration has quietly approached congressional Democrats about a potential change to their high-profile but long-shot effort to transform most of the District of Columbia into the nation's 51st state, according to executive and legislative branch officials. The deliberations center on the Constitution's 23rd Amendment, which gives three Electoral College votes to the district in presidential elections. If it is not repealed after any statehood, the bill would try to block the appointment of the three presidential electors. But the administration is said to have proposed instead giving them to the winner of the popular vote.

B.O.J. (BBG): Prices in Japan haven't suddenly risen like in the U.S. and China, and the Bank of Japan doesn't feel concerned over that possibility, Governor Haruhiko Kuroda says.Market participants may be thinking the rise in U.S. prices will impact monetary policy, but the increases will be temporary, and won't change U.S. policy and likewise in China, Kuroda says in response to a question in parliament.

SPAIN (RTRS): Spain's economy is expected to bounce back in the second half after a slow start to 2021 and could grow more than expected next year driven by a delayed boost from EU recovery funds, Bank of Spain Chief Economist Oscar Arce told reporters.In its latest economic outlook from March, the central bank expected gross domestic product, which last year slumped by a record 10.8% due to the COVID-19 pandemic, to expand by 6% in its central scenario this year and by 5.3% in 2022.On Thursday, it said in an annual report that Spain's economic recovery also hinged on the progress of the COVID-19 vaccination campaign, the implementation of reforms in the labour market and pension system, as well as private consumption.

UK DATA: The UK service economy continues to emerge from the lockdowns, with spending on debit and credit cards in the latest week higher by 7% over the previous week, the Office for National Statistics said Thursday. The indicator, derived from BOE/CHAPS payment data, is now running at 106% of the level seen in February 2020, driven by a notable increase in social spending on items including eating out and travel.

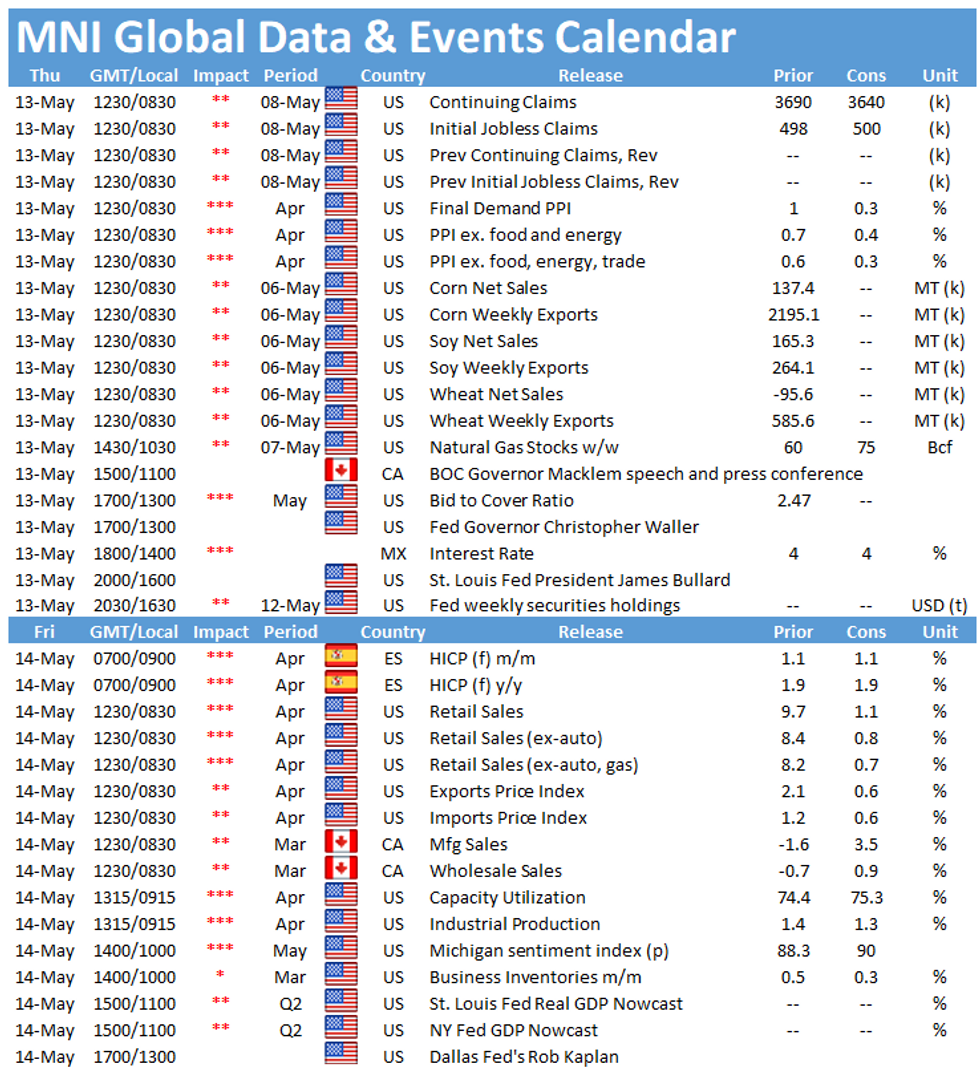

DATA:

No key data in the European morning.

FIXED INCOME: Sell-off continues in Europe

- Gilts and Bunds are under pressure again today as the sell-off continues amid low liquidity today with much of Europe on holiday for Ascension Day.

- Treasuries have been relatively stable today after the sell-off following the CPI print yesterday and then a successful 10-year auction which stemmed the bleeding.

- Today's focus will be on US PPI data which is due for release at 13:30BST/8:30ET. We will also hear from the Fed's Barkin and Waller.

- TY1 futures are up 0-2 today at 131-31+ with 10y UST yields down -1.1bp at 1.689% and 2y yields down -0.5bp at 0.160%.

- Bund futures are down -0.16 today at 168.78 with 10y Bund yields up 1.4bp at -0.111% and Schatz yields unch at -0.662%.

- Gilt futures are down -0.17 today at 127.04 with 10y yields up 2.0bp at 0.905% and 2y yields up 0.3bp at 0.103%.

FOREX: AUD/JPY Approaching Long-Held Support

- Risk-off is pervading through currency markets given the persistent weakness in global stocks since yesterday's US CPI print. AUD is among the weakest in G10, extending the sell-off from the Monday high of $0.7891 to briefly show below the $0.77 mark today. This opens declines toward the May 4 low of $0.7675, which would trigger further bearish signals.

- The main beneficiaries Thursday have been the JPY and USD, which sit firmer against most others in DMFX. AUD/JPY is on track to have declined in every session so far this week, and is narrowing the gap with key support at the 84.09 50-dma, a level that's largely held for months.

- Recent weakness in EUR/USD has put the pair at new weekly lows, opening 1.1986 as next key downside level.

- Focus turns to US PPI data due later today, with markets cognizant of the risk of a sizeable upside surprise after the eventful CPI reading out yesterday. Consensus looks for a modest slowdown in PPI later today, to +0.3% for the headline M/M and to +0.4% for ex-food and energy figures.

- Weekly US jobless claims data also cross, as well as speeches from BoE's Cunliffe & Bailey, Fed's Barkin, Waller & Bullard, BoC's Macklem and the Banxico rate decision.

EQUITIES: Sell-Off Continues

- Asian stocks closed sharply lower, with Japan's NIKKEI down 699.5 pts or -2.49% at 27448.01 and the TOPIX down 28.91 pts or -1.54% at 1849.04. China's SHANGHAI closed down 33.215 pts or -0.96% at 3429.536 and the HANG SENG ended 512.37 pts lower or -1.81% at 27718.67.

- European equities are likewise lower, with the German Dax down 288.02 pts or -1.9% at 14862.58, FTSE 100 down 168.43 pts or -2.4% at 6893.73, CAC 40 down 121.55 pts or -1.94% at 6192.17 and Euro Stoxx 50 down 77.68 pts or -1.97% at 3868.37.

- U.S. futures are lower, reversing modest overnight gains, with the Dow Jones mini down 243 pts or -0.73% at 33265, S&P 500 mini down 20.75 pts or -0.51% at 4038, NASDAQ mini down 53.75 pts or -0.41% at 12944.75.

COMMODITIES: Oil Leads Commodities Lower

- WTI Crude down $1.55 or -2.35% at $64.98

- Natural Gas up $0 or +0.03% at $2.971

- Gold spot down $1.06 or -0.06% at $1815.52

- Copper down $3.05 or -0.64% at $472.55

- Silver down $0.13 or -0.49% at $26.9166

- Platinum down $3.56 or -0.29% at $1212.48

LOOK AHEAD:

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.