Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US DATA

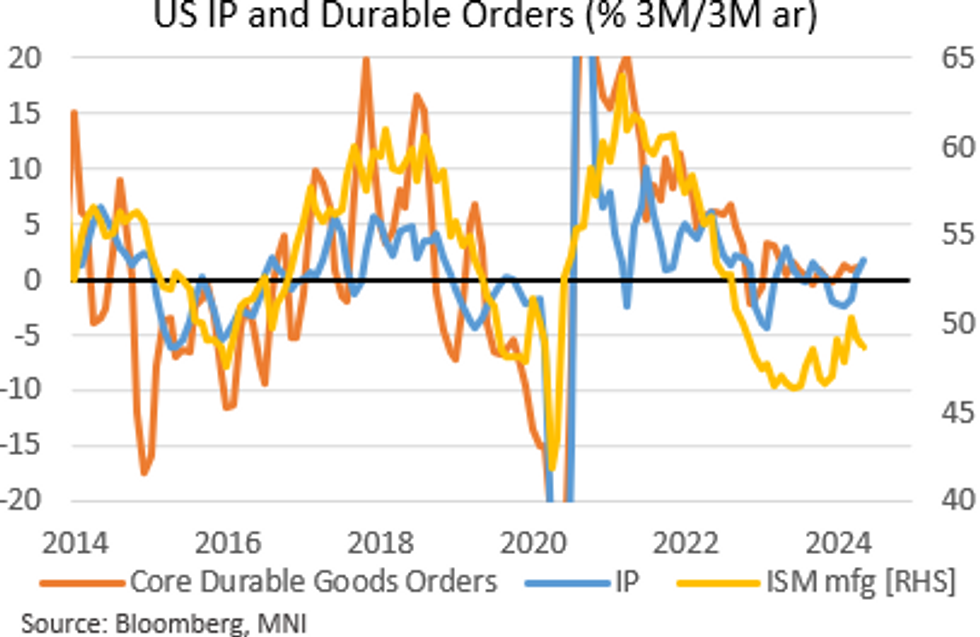

Industrial production rose 0.9% M/M in May, well above the 0.3% expected and 0.0% (unrev) prior. Manufacturing production likewise rose 0.9% (-0.4% prior rev from -0.3%; March rev to -0.1% from +0.2%). Utilities jumped by 1.6% M/M (4.0% prior rev from 2.8%, though March was rev down sharply to -0.3% from the previous +1.6% estimate).

- Mining output rose 0.3% after two consecutive declines. Durable goods manufacturing rose 0.6%, while nondurables rose 1.1%.

- This was a solid report after a cumulatively flat several months (the level of industrial production is now back at an 8-month high). Indeed, beyond the month-to-month noise in areas such as utilities, industrial production is regaining momentum despite continued weakness in major surveys.

- The 1.8% 3M/3M annualized print in May was the highest since May 2023, with manufacturing's 2.3% rate the fastest since June 2022. Capacity utilization is now at its highest since November 2023.

- While IP contracted in Q1, as one of the quasi-official "recession indicators", the pickup in IP over the last couple of months confirms that there is little hard evidence of recession - industrial or otherwise - in the 2nd quarter.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok