Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US TSYS: Anticipating Higher Inflation, How Much Priced in Ahead Fri CPI?

Broader markets caught up to ECB hawkish hold early Thursday, rates extending lows on ECB guidance of additional rate hikes in Sep and on w/potential for 50bp move anticipated.

- After some early volatility, yield curves extended flatter, 2s10s -2.338 at 22.212 vs. 25.237 early high. Large front end sales/crosses contributed to curve bear flattening after -12,434 TUU2 104-30.62 (-4.88), sell through 104-31.12 post-time bid at 1102:04ET.

- Tys pared losses, bonds back steady immediately after $19B 30Y auction re-open (912810TG3) stops through: 3.185% high yield vs. 3.200% WI; 2.35x bid-to-cover vs. 2.38x last month.

- stocks extending lows in late NY trade (ESM2 -40.0 at 4076.0) as markets contemplated already high CPI estimated read for May CPI (+0.7% vs. 0.3% prior) in the aftermath of the ECB's hawkish hold policy annc this morning.

- Support for stocks evaporated after the ECB said it would aim to raise its key interest rate for the first time since 2011 by 25 basis points in July, and said it could increase rates by a greater increment in September unless the inflation outlook moderates.

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements

- O/N +0.00043 to 0.82000% (+0.00086/wk)

- 1M +0.05500 to 1.25471% (+0.13500/wk)

- 3M +0.03358 to 1.72129% (+0.09529/wk) * / **

- 6M +0.02786 to 2.29429% (+0.18500/wk)

- 12M +0.04643 to 2.95857% (+0.18314/wk)

- * Record Low 0.11413% on 9/12/21; ** New 2Y high: 1.72129% on 6/9/22

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 0.83% volume: $79B

- Daily Overnight Bank Funding Rate: 0.82% volume: $247B

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 0.76%, $959B

- Broad General Collateral Rate (BGCR): 0.78%, $372B

- Tri-Party General Collateral Rate (TGCR): 0.78%, $354B

- (rate, volume levels reflect prior session)

FED Reverse Repo Operation, Third Consecutive Record High

NY Federal Reserve/MNI

NY Fed reverse repo usage climbs to new record high of 2,142.318B w/ 101 counterparties vs. Wednesday's prior record of 2,140.277B.

EURODOLLAR/SOFR/TREASURY OPTIONS SUMMARY

Aside from a massive conversion strip in Eurodollar options, FI option trade revolved around puts and put spreads ahead of Friday's May CPI.- Eurodollar option volume will see a massive jump in open interest, 720,000 to be exact after 90,000 conversion strips traded early in the first half: 90,000 in each of the Dec'22/Mar'23/Jun'23 97.00 conversion w/ Jun'23 97.50 conversion, 4.75 total/package. While large, the structure most likely involving one large account lending to another for the duration of the trade.

- Other Eurodollar trade included 17,200 short Aug 96.25 puts, 13.0-12.5 and 4,300 Blue Jun 96.75 puts, 0.5.

- 5Y Tactical Play For Stronger Than Expected CPI. Paper bought +10,000 wk2 5Y 111/111.25 put spds, 1.5 vs. 111-24.5/0.05%, a relatively cheap data hedge, but with markets anticipating 0.7% CPI, the actual number would have to be greater than that for the put spd to go bid.

- Early profit taking/unwind in 5Y options when underlying was trading near lows: paper sold -11,000 FVN 111.111.5 put spds, 10 ref 111-21.75 as well as -6,000 FVN 111.5/112 put spds.

- Block, 8,000 OQN2 97.00 calls 5.0 over short Jul Eurodlr 97.00 calls

- Blocks, 15,542 OQM2 96.75/97.00 put spds, 21.5

- 3,800 SFRN 97.50 puts, 5.0

- Block, 5,000 OQU2 96.50/96.75 3x2 put spds, 0.5 net/2-legs over

- +90,000 Dec'22/Mar'23/Jun'23 97.00 conversion w/ Jun'23 97.50 conversion, 4.75 total/package

- +5,000 Sep 96.87 puts, 3.5 vs. 97.295/0.12%

- 17,200 short Aug 96.25 puts, 13.0-12.5

- 4,300 Blue Jun 96.75 puts, 0.5

- 2,000 Sep 97.12/97.31/97.44 put flys

- +10,000 wk2 FV 111/111.25 put spds, 1.5 vs. 111-24.5/0.05%

- 5,000 FVN 111.75/112.75 put spds

- 6,000 wk3 TY 116.75 puts, 9

- Block, 9,000 wk3 TY 116.5 puts, 12

- -11,000 FVN 111.111.5 put spds, 10 ref 111-21.75, unwind

- -6,000 FVN 111.5/112 put spds

- 1,500 TYN 119/119.75/120.25 call flys

- 4,000 TYQ 116/117 put spds, 19

- 2,000 USQ 133/136 put spds, 103

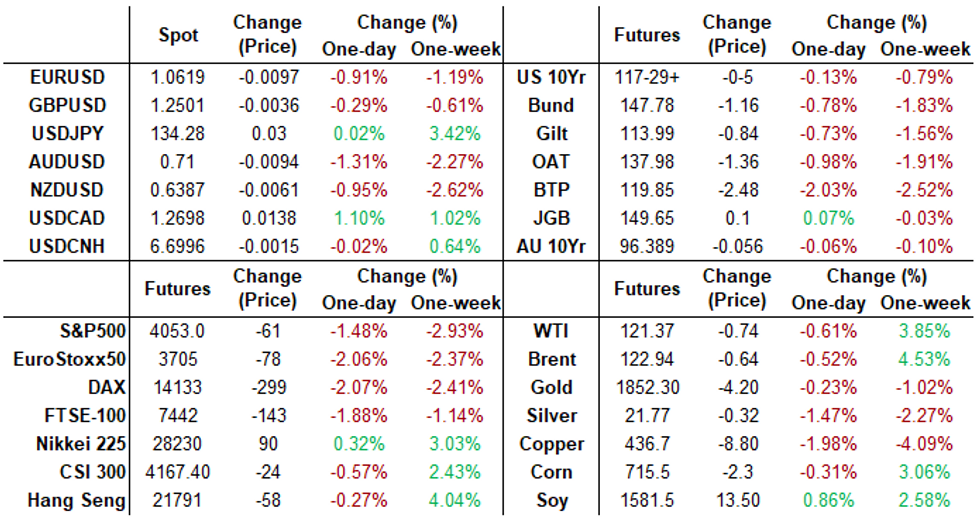

EGBs-GILTS CASH CLOSE: Bear Flattening On Hawkish ECB Signals

European bonds sold off Thursday on what was perceived as a hawkish signal from the ECB meeting, with periphery EGBs underperforming.

- The ECB's signaling hikes in July (25bp) and September (probably >25bp), with an open path to further hikes in order to quell inflation, helped short-end rate expectations sell off.

- July pricing was pared as a 50bp move was faded, but Sep thru Dec implied rates hit cycle highs.

- The German curve flattened accordingly, with the UK following suit.

- Italian 10Y reached the widest since May 2018 (+ bp) on the combination of incoming rate hikes and an apparent lack of progress on an anti-fragmentation tool (reinforced later in the session by a Reuters sources piece).

Closing Yields / 10-Yr Periphery EGB Spreads To Germany:

- Germany: The 2-Yr yield is up 13.4bps at 0.835%, 5-Yr is up 11.8bps at 1.195%, 10-Yr is up 7.6bps at 1.43%, and 30-Yr is up 3.4bps at 1.626%.

- UK: The 2-Yr yield is up 7.5bps at 1.855%, 5-Yr is up 8.2bps at 1.963%, 10-Yr is up 7.7bps at 2.323%, and 30-Yr is up 3.3bps at 2.491%.

- Italian BTP spread up 15.2bps at 217.3bps / Spanish up 6.5bps at 119.3bp

EGB Options: Hawkish ECB Plays Feature

Thursday's Europe rate/bond options flow included:

- DUN2 109.10/109.20/109.30/109.40c condor, bought for 2 in 1.5k

- DUU2 108.00/107.40 1x2 put spread bought for 2 in 5k

- RXN2 152.00/153.50cs, bought for 14 in ~4.4k

- RXN2 155.50/157.00cs, bought for 1.5 in 13.5k (short cover)

- 0RM2 98.37p vs 2RM2 98.12p, sold the 1y at 5 in 3k

- ERZ2 99.50/99.37/99.25/99.12p condor, sold at 1.75 in 4.75k

- OEQ2 122/121ps 1x1.5, bought for 7 in 2k

Of note this morning were multiple Euribor options ahead of the ECB meeting, which would have benefited from the ultimately hawkish market reaction to the meeting:

- ERN2 99.37/99.25/99.15p fly, bought for 1.5 in 8k 36 days to expiry

- ERQ2 99.375/99.25/99.125 put fly, bought for 1.5 in 15k

- ERU2 99.50/99.375/99.25p ladder, bought for flat in 2.5k

- ERU2 99.50/99.375ps vs 99.75c, bought the ps for 2 in 5k

FOREX: Volatile Euro Ends At Week’s Lows Following ECB

- EURUSD initially traded well on the back of the ECB rate decision, showing above the bear channel top and printing 1.0774 - albeit briefly. The pair was unable to maintain its bid and sharply reversed course into the European close, taking out the week's lows in the process. Having failed above the bear channel top, key short-term support at 1.0627, the Jun 01 low, was then breached with the next notable support residing at 1.0533, the May 20 low.

- Broad dollar indices are extending gains late Thursday, having risen over 0.6% to the best levels of the week. Downward pressure on equities and higher US yields supporting the price action and weighing on the likes of AUD, CAD and NZD.

- AUDUSD the notable underperformer across G10, retreating 1.29%. The pair has traded back below the 20-day EMA, at 0.7153 today and a sustained break of this average would threaten the recent recovery. A stronger reversal would refocus attention on the bear trigger at 0.6829, May 12 low.

- In emerging markets, it is worth noting a particularly volatile session for the Turkish Lira. After an aggressive, albeit brief, spike to fresh recent highs of 17.3717, price had consolidated somewhat before the finance ministry stated that Turkey would announce new economy steps later today. As of writing, no announcement has been made, however, TRY has been significantly bolstered by the news.

- A sharp reversal lower for USDTRY saw the pair briefly print below 16.80 and remains just above 16.90, down 1.25% for the session. Firm support lies at 16.1964, the 20-day EMA.

- US CPI headlines the data docket on Friday. Core CPI inflation is expected to dip slightly from +0.57% M/M in April to +0.5% M/M, with a faster rise in headline CPI at +0.7% M/M amid energy price rises. Canadian employment data also round off the week’s calendar.

FX: Expiries for Jun10 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0700(E905mln), $1.0790-00(E1.8bln), $1.0900(E1.3bln)

- USD/CAD: C$1.2600($525mln), C$1.2735-50($1.1bln)

Late Equity Roundup: Extending Lows in Late NY Trade

After a firmer open, stocks extending lows in late NY trade (ESM2 -40.0 at 4076.0) as markets contemplated already high CPI estimated read for May CPI (+0.7% vs. 0.3% prior) in the aftermath of the ECB's hawkish hold policy annc this morning.

- Nascent carry-over support on rumors China would revive Alibaba's ANT IPO didn't last long, SPX traded lower after China denied they were working on restructuring the company.

- Support for stocks evaporated after the ECB said it would aim to raise its key interest rate for the first time since 2011 by 25 basis points in July, and said it could increase rates by a greater increment in September unless the inflation outlook moderates.

- SPX leading/lagging sectors: Softer but still outperforming, Consumer Staples (-0.10%) and Consumer Discretionary (-0.51%), the latter with autos sector firmer mostly due to Tesla trading +0.90% at 732.15. Energy recovered off earlier levels, sector -0.65% in late trade. Laggers: Financials (-1.32%) with carry-over weakness in Banks followed by Communication Services (-1.29%) and Materials (-1.20%).

- DJIA -226.02 (-0.69%) at 32684.27; Nasdaq -159.6 (-1.3%) at 11927.05.

- Dow Industrials Leaders/Laggers: Home Depot (HD) +5.77 at 303.30, United Health Care (UNH) +1.56 at 495.09, Salesforce.com (CRM) +0.94 at 190.13. Laggers: Goldman Sachs (GS) -6.22 at 308.46, Boeing (BA) -4.35 at 135.28 and Visa (V) -4.24 at 209.26.

STOCKS: E-MINI S&P (M2): Range Bound

- RES 4: 4509.00 High Apr 21

- RES 3: 4393.25 High Apr 22

- RES 2: 4303.50 High Apr 26/28 and a key short-term resistance

- RES 1: 4178.11/4202.25 50-day EMA / High May 31

- PRICE: 4097.25 @ 14:16 BST June 9

- SUP 1: 3960.50/3807.50 Low May 26 / Low May 20 and bear trigger

- SUP 2: 3801.97 38.2% of the Mar ‘20 - Jan ‘22 bull leg (cont)

- SUP 3: 3787.74 2.618 proj of the Mar 29 - Apr 18 - 21 price swing

- SUP 4: 3747.52 2.764 proj of the Mar 29 - Apr 18 - 21 price swing

S&P E-Minis are still range bound. The current sideways move appears to be a bull flag, this reinforces short-term bullish conditions. Attention is on the 50-day EMA, at 4178.11 today. A clear break of this EMA would strengthen a bullish outlook and open 4303.50, the Apr 26/28 high. Gains are still considered corrective however and the primary trend direction is down. First support to watch is 3960.50, May 26 low.

COMMODITIES: Gas Dominates On Continued Fallout From Freeport Fire

- Crude oil prices have been trimmed today after yesterday’s new cycle highs with Brent getting close to $125/bbl, on a day where more focus has been on gas in the continued fallout from the fire at the Freeport LNG terminal in Texas.

- WTI is -0.34% at $121.68, maintaining below yesterday’s high of $123.18 with support at $117.14 (Jun 7 low). Today’s most active strike in CLN2 has been $125/bbl calls.

- Brent is -0.16% at $123.39, also off yesterday’s low of $124.4 and more comfortably above support at the 20-day EMA of $114.88.

- Gold is -0.27% at $1848.48 as it remains largely rangebound this week, surprisingly resilient to USD strength following the ECB decision. Resistance remains the 50-day EMA of $1872.7 with support at $1828.6 (Jun 1 low).

- US natural gas unwound some of the post-Freeport fire drop on a modestly smaller than expected rise in gas stockpiles plus news that the terminal is set to remain shut for a minimum of three weeks, bouncing +2.4% on the day but still almost 5% lower from early yesterday levels.

- In contrast, European gas prices settle sharply higher, rising 16% in the UK and with the Dutch TTF up almost 7%.

Friday Data Calendar

| Date | GMT/Local | Impact | Flag | Country | Event |

| 10/06/2022 | 0001/0101 | ** |  | UK | IHS Markit/REC Jobs Report |

| 10/06/2022 | 0130/0930 | *** |  | CN | CPI |

| 10/06/2022 | 0130/0930 | *** | | CN | Producer Price Index |

| 10/06/2022 | 0600/0800 | * |  | NO | CPI Norway |

| 10/06/2022 | 0700/0900 | *** |  | ES | HICP (f) |

| 10/06/2022 | 0800/1000 | * |  | IT | Industrial Production |

| 10/06/2022 | 0830/0930 | ** | | UK | Bank of England/TNS Inflation Attitudes Survey |

| 10/06/2022 | 1230/0830 | *** |  | CA | Labour Force Survey |

| 10/06/2022 | 1230/0830 | *** |  | US | CPI |

| 10/06/2022 | 1345/1545 |  | EU | ECB Lagarde Message for Goethe Uni Law & Finance Institute | |

| 10/06/2022 | 1400/1000 | *** | | US | University of Michigan Sentiment Index (p) |

| 10/06/2022 | 1400/1000 | * | | US | Services Revenues |

| 10/06/2022 | 1600/1200 | *** | | US | USDA Crop Estimates - WASDE |

| 10/06/2022 | 1800/1400 | ** | | US | Treasury Budget |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.