Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US TSYS: There's Always Time For Diplomacy

Risk-on carried over from early London hours: Russia/Ukraine tensions cool after reports that Russia withdrawing some troops from Ukraine border. NATO head Stoltenberg said there's "no concrete sign of de-escalation", yet remains "cautiously optimistic", Bbg.

- Tsys extended lows after the bell (30YY tapped 2.3669% high) as US President Biden commented on Ukraine situation: "As long as there is hope for diplomatic resolution, we will pursue it. Russian defense ministry reported some units are leaving but US has not verified this yet. Analysts believes they are still in a very threatening position." However, Biden added "invasion remains distinctly possible and Americans should leave Ukraine now. If Russia attacks Ukraine it will be a war of choice not of necessity."

- Higher than forecasted PPI for Jan (+1.0% vs. 0.05% est) weighed on FI and pre-open stocks.

- Contributing to bear steepening (5s30s +5.5 at 42.69 late), trading desks report real$ buying short end and separately selling 30s, deal-tied rate lock selling keeping pressure on as markets hedged $6B Bristol Myers 4pt jumbo (10s, 20s, 30s and 40s).

- Eurodollar/Treasury option flow was mixed, two-way call interest in the former: Scale buyer 38,000 short Sep 99.00 calls, 2.0 ref: 97.615-.62, after a Block sale of -20,000 Sep 98.50/98.75 call spds, 0.5 over Sep 97.37 puts vs. 98.33/0.30%.

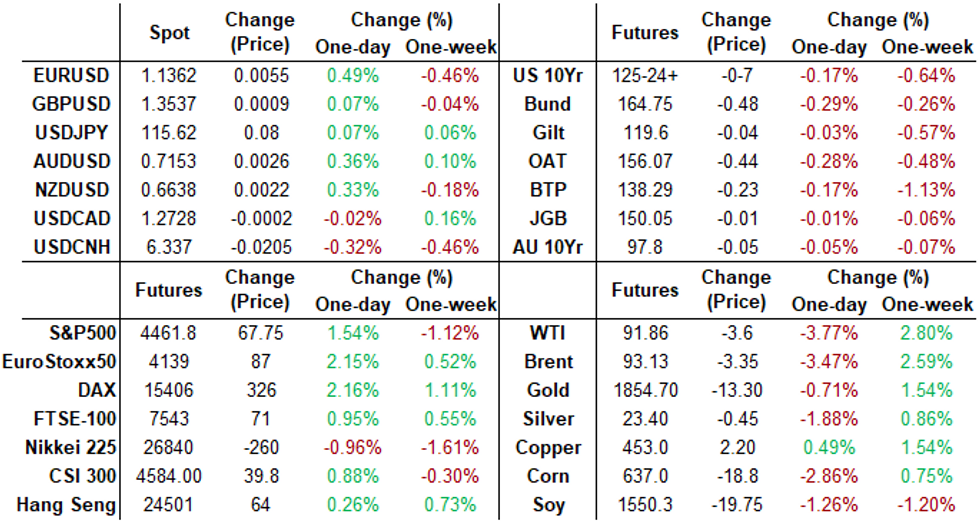

- After the close 2-Yr yield is down 0.5bps at 1.5692%, 5-Yr is up 2.4bps at 1.9351%, 10-Yr is up 5.8bps at 2.0451%, and 30-Yr is up 7.5bps at 2.3609%.

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements:

- O/N -0.00257 at 0.07414% (-0.00429/wk)

- 1 Month -0.00600 to 0.11971% (-0.07143/wk)

- 3 Month +0.01014 to 0.46871% (-0.03772/wk) ** Record Low 0.11413% on 9/12/21

- 6 Month -0.00115 to 0.79271% (-0.04772/wk)

- 1 Year +0.02057 to 1.34271% (-0.04958/wk)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 0.08% volume: $63B

- Daily Overnight Bank Funding Rate: 0.07% volume: $249B

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 0.05%, $895B

- Broad General Collateral Rate (BGCR): 0.05%, $329B

- Tri-Party General Collateral Rate (TGCR): 0.05%, $325B

- (rate, volume levels reflect prior session)

NY Fed Purchase Operation: The Desk plans to purchase approximately $20 billion, ending Thu, March 9.

- Tsy 4.5Y-7Y, $3.201B accepted vs. $16.425 submission

- Next scheduled purchases:

- Thu 02/17 1010-1030ET: Tsy 10Y-22.5Y, appr $1.625B steady

- Tue 02/22 1010-1030ET: TIPS 1Y-7.5Y, appr $1.025B vs. $2.025B prior

- Thu 02/24 1010-1030ET: Tsy 0Y-22.5Y, appr $6.225B steady

- Tue 03/01 1100-1120ET: TIPS 7.5Y-30Y, appr $0.625B vs. $1.225B prior

- Thu 03/03 1100-1120ET: Tsy 7Y-10Y, appr $1.625B vs. $3.225 prior

- Tue 03/08 1010-1030ET: Tsy 22.5Y-30Y, appr $1.825B steady

- Thu 03/09 1010-1030ET: Tsy 2.25Y-4.5Y, appr $4.025B

FED Revers Repo Operation

NY Federal Reserve/MNI

NY Fed reverse repo usage fall to $1,608.494B w/ 81 counterparties vs. $1,666.232B prior session -- remains well off all-time high of $1,904.582B on Friday, December 31.

EURODOLLAR/SOFR/TREASURY OPTIONS SUMMARY

Eurodollar Options:- +15,000 Dec 99.62 calls, 1.5

- Update, over +38,000 short Sep 99.00 calls, 2.0 ref: 97.615-.62

- Block, -20,000 Sep 98.50/98.75 call spds, 0.5 over Sep 97.37 puts vs. 98.33/0.30%

- 10,000 Green Mar 97.31/97.37 put spds, 1.0

- +2,500 Dec 98.25/98.50/98.75 call trees, 0.5

- +5,000 Dec 99.62 calls, 1.5

- +2,000 Dec 98.00 straddles, 79.0

- Overnight trade

- 25,000 short May 97.50/97.62 put spds

- 10,000 short Sep 97.37/97.50 put spds

- 5,000 TYH 126.75/127.25 call spds, 2

- 3,000 FVJ 117.5/118/118.5 call flys

- -10,000 TYH 127/TYJ 124.5 put calendar/diagonal, 49 vs. 125-23

- over 6,000 TYH 126.5 puts, 57

- 5,500 FVJ 120 calls, 2

- 5,000 TYH 124/125 put spds, 7

- -2,700 TYM 125.5/127.5 strangles, 210-207

EGBs-GILTS CASH CLOSE: Safe Haven Bid Continues To Unwind

Geopolitical risk once again drove European FI Tuesday, with yields continuing to rise from Monday's lows on signs of de-escalation between Russia and Ukraine.

- Periphery spreads narrowed in a broad risk-on move, with equities in the green. Though 10Y BTP yields rose to just shy of 2% (post-May 2020 high).

- German 10Y Bund yields hit the highest since Nov 2018 (0.3254% intraday) as safe haven bids unwound further and the curve bear steepened.

- With attention on Wednesday's UK CPI data, 2 Year UK yields continued their ascent (reversing an early drop), in a flattening move on the curve.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is up 1.6bps at -0.347%, 5-Yr is up 1.1bps at 0.055%, 10-Yr is up 2.5bps at 0.308%, and 30-Yr is up 5.6bps at 0.551%.

- UK: The 2-Yr yield is up 2.7bps at 1.537%, 5-Yr is up 2.2bps at 1.526%, 10-Yr is down 0.7bps at 1.582%, and 30-Yr is down 3.7bps at 1.609%.

- Italian BTP spread down 3.9bps at 164.9bps / Spanish down 1.6bps at 99.8bps

EGB Options: Some Sterling Upside Post-Jobs, Pre-Inflation

Tuesday's Europe rates / bond options flow included:

- RXH2 165/164.5ps, sold at 28 in 2.7k

- RXJ2 160.50/159.50ps, bought for 29 in 20k (rolling down strike)

- 2RH2 99.25/99.125ps sold down to 6.75 (ref 99.14)

- ERZ2 100.37/100.50cs 1x2, bought the 1 for 1 in 20k

- OEJ2 129.75/129.25ps, bought for 12 and 13 in 13k (was bought yesterday for 10/11 in 10k)

- SFIK2 98.70/98.80/98.90/99.00c condor for 1.75 in 10k With, SFIM2 98.80/99.00/99.10c fly, bought for 2.5 in 10k

- SFIM2 98.40/98.60/98.75 broken c fly, bought for 4.75 in 5k

FOREX: US Dollar Retraces Monday’s Gains As Equities Recover

- The greenback lost favour on Tuesday as Equity indices recovered on reports of de-escalation at the Ukraine border, reviving risk appetite across global equity markets.

- The dollar index find itself 0.4% lower approaching the end of the US session, giving up the entirety of yesterday’s advance.

- EURUSD found good support below 1.1300 and has bounced. The pair now sits between key short-term resistance at 1.1495 and strong support of 1.1267, the Feb 2 low. A breach of this support would signal scope for a deeper retracement of recent gains.

- Risk-tied Antipodean FX had a good showing with both AUD and NZD rising 0.35%, however, GBP and CAD remained broadly unchanged ahead of their respective inflation prints, scheduled for tomorrow.

- With the Euro strength and the easing geopolitical tensions, CEE FX saw strong support, with RUB, PLN, HUF and CZK all rising over 1%. SEK was a notable outperformer (USDSEK -1.07%), continuing to unwind the post Riksbank Krona losses.

- Overnight, markets will receive CPI/PPI data from China before later in the day, both the UK and Canada also release consumer price data. The early US session will be headlined by January retail sales before markets try and extrapolate any clues from the slightly dated FOMC minutes of the January meeting.

FX: Expiries for Feb16 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1250(E860mln), $1.1280-00(E1.0bln), $ $1.1400-05(E1.1bln), $1.1425-30(E1.0bln)

- USD/JPY: Y114.40-50($1.6bln), Y115.00($619mln), Y115.25-40($1.0bln), Y116.00-05($1.0bln)

- EUR/JPY: Y128.50(E1.4bln)

- USD/CAD: C$1.2600($837mln), C$1.2785-90($630mln)

EQUITIES: Stocks Bounce as Russia Demobilize, But Last Week's Highs Out of Reach

- Wall Street opened well, and held the day's gains into the close as reports of demobilization of Russian troop units on both the eastern and southern Ukrainian borders prompted markets to re-assess the risk of a near-term military conflict. This allowed the e-mini S&P to rise back above the 200-dma, although rallies remained well shy of last week's best levels.

- While a relief rally was evident across all three major indices, some concerns remain, with neither the UN nor NATO confirming a withdrawal of military units from war footing. This puts Biden's speech on Russian relations in focus, with POTUS speaking at 1530ET/2030GMT.

- The tech and growth sectors led the bounce Tuesday, with the semiconductors sub-index seeing particular strength. Energy names were the laggards, with Marathon Oil, Occidental Petroleum and Diamondback Energy off as much as 4%.

- European indices were uniformly positive, with gains consistent across both core and peripheral stock markets. The UK's FTSE-100 was the underperformer, rising just 1% as soft energy and metals prices weighed on the FTSE-100's outsized mining and resource exploration sectors.

- Despite the intraday recoveries posted Tuesday, the medium-term technical signals may suggest the uptrend in stocks has reversed, with a key technical signal shifting from a bull phase to a bearish cycle. Read more here: https://marketnews.com/mni-market-analysis-sp-500-...

COMMODITIES: Oil And Gold Slide On Russian De-Escalation

- Crude oil prices are down heavily today on Russian de-escalation after some units returned to bases. US Secretary of State Blinken has said more recently that the window remains to resolve the crisis peacefully but that the US needs to see verifiable, meaningful de-escalation.

- WTI is -3.6% at $92.01 in the March contract, but with large declines throughout the curve. It sits above the key short-term support of $88.41 (Feb 9 low) whilst resistance is yesterday’s high of $95.82. Prices are however still up 3% on the week and 22% YTD.

- Today's most active strikes in the H2 contract have been $95/bbl calls followed by $90/bbl puts.

- Brent is -3.3% at $93.33, sitting above support at $89.93 (Feb 8 low) with resistance yesterday’s high of $96.78.

- Similarly, gold is down -1.0% at $1853.3 but bullish conditions remain after a recent clearance of resistance at $1853.9, the Jan 25 high, and it earlier today clearing the Nov 16 high of $1877.2.

Wednesday Data Calendar

| Date | GMT/Local | Impact | Flag | Country | Event |

| 16/02/2022 | 0700/0700 | *** |  | UK | Consumer inflation report |

| 16/02/2022 | 0700/0700 | *** | | UK | Producer Prices |

| 16/02/2022 | 0700/0800 | ** |  | NO | Norway GDP |

| 16/02/2022 | 0930/0930 | * | | UK | ONS House Price Index |

| 16/02/2022 | 1000/1100 | ** |  | EU | industrial production |

| 16/02/2022 | 1200/0700 | ** |  | US | MBA Weekly Applications Index |

| 16/02/2022 | 1330/0830 | *** | | US | Retail Sales |

| 16/02/2022 | 1330/0830 | ** | | US | import/export price index |

| 16/02/2022 | 1330/0830 | *** |  | CA | CPI |

| 16/02/2022 | 1330/0830 | ** | | CA | Monthly Survey of Manufacturing |

| 16/02/2022 | 1330/0830 | ** | | CA | Wholesale Trade |

| 16/02/2022 | 1415/0915 | *** | | US | Industrial Production |

| 16/02/2022 | 1500/1000 | * | | US | business inventories |

| 16/02/2022 | 1500/1000 | ** | | US | NAHB Home Builder Index |

| 16/02/2022 | 1530/1030 | ** | | US | DOE weekly crude oil stocks |

| 16/02/2022 | 1800/1300 | ** | | US | US Treasury Auction Result for 20 Year Bond |

| 16/02/2022 | 1830/1330 | | CA | BOC Deputy Lane speech | |

| 16/02/2022 | 1900/1400 | * | | US | FOMC Minutes |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.