Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

HIGHLIGHTS

- BRAINARD: PROBABLY APPROPRIATE TO SOON MOVE TO SLOWER HIKE PACE, Bbg

- NEW YORK FED SAYS INFLATION EXPECTATIONS RISE IN OCTOBER

- NY FED: OCT. INFLATION EXPECTATIONS ONE YEAR AHEAD 5.9% VS 5.4%

- US PRES BIDEN: THERE NEED NOT BE A NEW COLD WAR ... I DO NOT THINK THERE IS ANY IMMINENT ATTEMPT BY CHINA TO INVADE TAIWAN, Bbg

- AMAZON PLANS TO LAY OFF APPROXIMATELY 10,000 PEOPLE IN CORPORATE AND TECHNOLOGY JOBS STARTING AS SOON AS THIS WEEK - NYT

Key links: MNI: US Treasury Clearing To Limit Contagion, Create New Risks / US Treasury Auction Calendar / US$ Credit Supply Pipeline

US TSYS: Terminal Rates vs. Pace of Rate Hike Step-Down

Tsys moderately weaker after the bell, upper half of session range as focus remains on Fed speak and inflation metrics after last Thu's softer than anticipated CPI.

- Fed Gov Waller eco-outlook from Australia last night: ""We're at a point we can start thinking maybe of going to a slower pace," Waller said, but "we're not softening...Quit paying attention to the pace and start paying attention to where the endpoint is going to be. Until we get inflation down, that endpoint is still a ways out there" DJ reported.

- Rates bounced after Fed VC Brainard eco-outlook comments: "PROBABLY APPROPRIATE TO SOON MOVE TO SLOWER HIKE PACE".

- Flipside: jump in median inflation expectations (1-Year: 5.94% in Oct vs 5.44% Sep) in the NY Fed's consumer survey looks largely a result of a rebound in food and energy price expectations.

- Short end selling evaporated after the Brainard comments, Fed funds implied hike in Dec'22 steady at 50.9bp, Feb'23 cumulative 86.9bp to 4.717% vs. 86.9bp earlier, terminal slips to 4.93% in Jun'23 (5.08% pre-CPI).

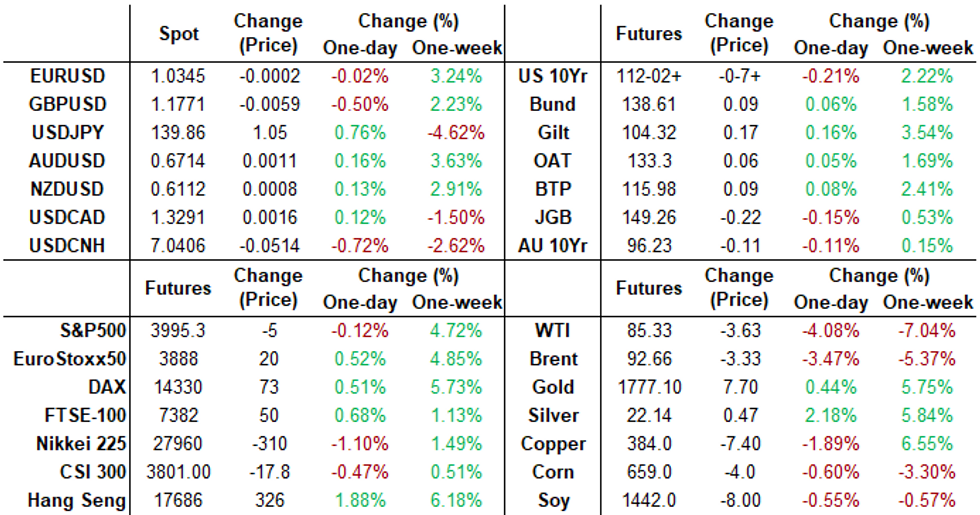

- Current 2-Yr yield is up 7.6bps at 4.4077%, 5-Yr is up 6.8bps at 4.0055%, 10-Yr is up 6.4bps at 3.8761%, and 30-Yr is up 4.7bps at 4.0625%.

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements:- O/N +0.00371 to 3.81857% (-0.00143 total last wk)

- 1M +0.01128 to 3.88657% (+0.01715 total last wk)

- 3M +0.03772 to 4.64386% (+0.05585 total last wk) * / **

- 6M +0.01986 to 5.10386% (+0.07271 total last wk)

- 12M +0.03228 to 5.48357% (-0.21514 total last wk)

- * Record Low 0.11413% on 9/12/21; ** New 14Y high: 4.64971% on 11/10/22

- Daily Effective Fed Funds Rate: 3.83% volume: $97B

- Daily Overnight Bank Funding Rate: 3.82% volume: $283B

- Secured Overnight Financing Rate (SOFR): 3.78%, $987B

- Broad General Collateral Rate (BGCR): 3.75%, $411B

- Tri-Party General Collateral Rate (TGCR): 3.75%, $395B

- (rate, volume levels reflect prior session)

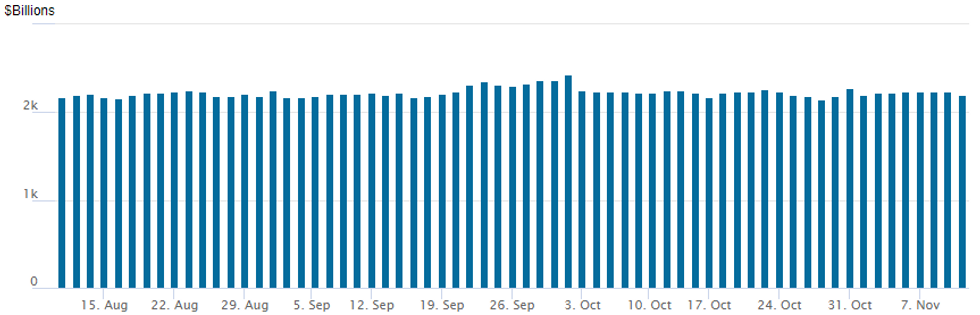

FED Reverse Repo Operation

NY Federal Reserve/MNI

NY Fed reverse repo usage recedes to $2,200.586B w/ 95 counterparties vs. $2,237.812B in the prior session. Prior record high stands at $2,425.910B on Friday, September 30.

EURODOLLAR/SOFR/TREASURY OPTIONS SUMMARY

Mixed trade on moderate volumes Monday, Treasury options seeing better flow centered on upside 10Y call buying as underlying futures climb off weaker opening levels. Markets not quite committed to last Thu's softer CPI with some speculative call buyers look to catch the highs in yields.- SOFR Options:

- Block, 3,000 SFRZ2 95.37 puts vs. 4,500 SFRZ 95.50/95.56 call spds, 0.5 net/puts over

- +1,500 SFRZ2 95.62/95.75 call spds 0.5

- +5,000 SFRZ2 95.50/95.62 call spds, 1.75

- +15,000 SFRM3 94.62/94.75 put spds, 3.75 vs. 95.10/0.06%

- Eurodollar Options:

- 12,200 EDM 97.50 calls, 2.5

- Block, 2,000 short Jun 95.00/95.50/96.00 put flys

- 5,000 Dec 97.12 calls, cab

- Treasury Options:

- 2,400 FVZ2 106.75/107.25 put spds

- +5,000 FVZ 105 puts, 1

- +10,000 TYF 113 calls 55 rev 112-13

- 3,600 TYZ 112.25 calls, 32

- Over 12,000 TYZ 112.5 calls, 26

- Over +16,000 TYF 112.5 calls, 105-106 vs. 112-03/0.49%

- Over 14,000 TYZ 113 calls, 15 ref 112-05.5

- -9,000 TYZ 113.25 calls, 11 vs. 112-04/0.20%

- 2,000 TYZ2 112 puts, 36

- 3,000 FVZ2 107.75 calls, 21.5 vs. 107-21/0.46%

- Block, -11,185 wk1 10Y 113/114.5 2/3 call spds vs. wk3 10Y 110.5/112.5 call spds - more on screen

- 2,500 TYF 114.5/115.5 call spds ref

- 1,000 FVZ 108.5/109.25 2x3 call spds

EGBs-GILTS CASH CLOSE: ECB Dec Hike In Focus

European yields reversed a an early drop with a sharp rise in the afternoon, leaving them largely flat on Monday's session.

- ECB hike pricing faded and EGB yields fell mid-morning amid comments by ECB's Panetta (who said aggressive tightening is not advisable) and an MNI sources story pointing to a 50bp December hike with some risks of 75bp.

- A jump in equities in the afternoon put the pressure back on core FI, and yields erased most of their earlier drop, though largely shrugged off a dip in US yields toward the cash close.

- Periphery EGB spreads were mostly flat. Greece bucked the trend with sharp spread narrowing after a successful 10Y reopening operation.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is up 0.9bps at 2.216%, 5-Yr is down 0.5bps at 2.082%, 10-Yr is down 1.3bps at 2.147%, and 30-Yr is down 0.9bps at 2.103%.

- UK: The 2-Yr yield is down 0.6bps at 3.159%, 5-Yr is down 0.8bps at 3.359%, 10-Yr is up 1bps at 3.368%, and 30-Yr is up 0.6bps at 3.497%.

- Italian BTP spread unchanged at 204.5bps / Greek down 18.3bps at 219.2bps

EGB Options: Both Near- And Far-Dated Euribor Upside Dominates

Monday's Europe rates / bond options flow included:- OEZ2 116.75 put bought for 2 in 5k

- ERZ2 98.00/97.875 put spread sold at 11 in 9k

- ERZ2 97.875/98.00 call spread bought for 1.75 in 3k

- ERZ2 97.75/97.875/98.00 1x3x2 call fly bought for 2.75 in 2.5k

- ERZ2 97.75/97.375 1x2 put spread, bought for 8 in 5k (v 97.72)

- 0RF3 97.125/97.375/97.50 call ladder bought for 2 in 8k

FOREX: Greenback Recovery Fades As Equities Pick Up Late Bid

Despite a solid bounce for the US Dollar during the first half of Monday’s session, a late grind through the highs for major equity indices has taken the shine off the greenback recovery. The USD index (0.35%) does look set to halt its losing streak since the US inflation data last week, however, gains appear much more modest approaching the APAC crossover.

- Early USD strength was largely attributed to comments from Fed's Waller, stating that the FOMC need to see more than just a single lower CPI print before being comfortable that inflation is in decline. Waller added that "The market seems to have gotten way out in front on this".

- The JPY (-0.77%) remains the poorest performer in G10 after a near 200-point USDJPY rally from the open met stiff resistance at the 100-dma of 140.82, the first upside technical level of note. The pair has drifted back below 140.00 throughout US hours in line with the general softer tone for the dollar.

- The extension of equity strength continues to underpin both AUD and NZD, rising around a quarter of a percent. Outperforming is the Chinese Yuan, supported by Chinese authorities moving to support the local property market. Regulators rolled out a series of 16 policy measures, from liquidity support to looser pre-payment conditions. USDCNH (+0.65%) traded within close range of the October lows at 7.0127, extending the three-day rally for the Yuan.

- EURUSD continues to trade with a bid tone and is hovering right at significant resistance between 1.0350-1.0368, the latter level representing the August highs, the best level traded since the July breakdown.

- RBA minutes are due overnight before a set of Chinese activity/employment data. The European session features UK employment figures as well as German ZEW sentiment data. In the US, empire state manufacturing and PPI highlight the docket.

FX: Expiries for Nov15 NY cut 1000ET (Source DTCC)

- EUR/USD: $0.9935-55(E1.2bln), $1.0075(E844mln), $1.0175-00(E1.2bln)

- USD/JPY: Y139.00($500mln), Y140.00($663mln)

- AUD/NZD: N$1.1000(A$511mln)

- USD/CNY: Cny7.0000($1.1bln)

Late Equity Roundup: Paring Late Gains, Pharma Outperforming

Late session support for stocks evaporating a little, SPX and Dow components firmer but off highs, vs. mildly weaker Nasdaq shares. SPX eminis currently trading +2.75 (0.07%) at 4003.5; DJIA +84.07 (0.25%) at 33836.97; Nasdaq -18.7 (-0.2%) at 11305.68.

- SPX leading/lagging sectors: Healthcare (+1.14%) sector took the lead in the second half lead by pharmaceuticals and biotechs (Moderna +6.05%, Biogen +5.11%, Pfizer +4.55%). Materials (+0.76%) sector follows, mining shares outperforming. Laggers: Real Estate (-1.72%), Consumer Discretionary (-0.85%) w/ autos underperforming, Financials (-0.68%) weighed by banks and diversified financials.

- Dow Industrials Leaders/Laggers: Pharmaceuticals outperforming w/ JNJ +3.85 at 173.10, Amgen (AMGN) +3.43 at 288.45, Merck (MRK) +3.42 at 101.38. Laggers: Microsoft (MSFT) -3.52 at 243.59, Home Depot (HD) -4.77 at 310.17, Walmart -1.92 at 140.66.

E-MINI S&P (Z2): Trend Needle Points North

- RES 4: 4175.00 High Sep 13 and a key resistance

- RES 3: 4146.63 76.4% retracement of the Aug 16 - Oct 13 downleg

- RES 2: 4100.00 Round number resistance

- RES 1: 4023.44 61.8% retracement of the Aug 16 - Oct 13 downleg

- PRICE: 4004 @ 1500ET Nov 14

- SUP 1: 3837.45 50-day EMA

- SUP 2: 3750.00 Low Nov 9

- SUP 3: 3704.25 Low Nov3 and key short-term support

- SUP 4: 3641.50 Low Oct 21

S&P E-Minis remain bullish. The contract rallied sharply higher last week and in the process cleared resistance at 3928.00, Nov 1 high. The break strengthens a short-term bullish condition and price has established a sequence of higher highs and higher lows on the daily scale. This opens 4023.44 next, a Fibonacci retracement. On the downside, key short-term support has been defined at 3704.25, the Nov 3 low.

COMMODITIES: Natural Gas Set For Further Upside Pressure From Freeport Delay

- Crude oil has slipped 2.5-3% today, reversing Friday’s gains with the US out for Veterans Day with the main driver seen as fading optimism over China’s recovery from lockdowns despite equities firming after Fed VC Brainard said it would be appropriate for the Fed to soon slow its pace of hikes.

- The EIA meanwhile showed the first US build in drilled, unfracked wells since Jun 2020.

- WTI is -3.3% at $86.00, moving closing to key support at $84.70 (Nov 10 low).

- Brent is -2.8% at $93.36, moving closer to a key support at $91.73 (Nov 10 low).

- Gold is +0.07% at $1772.57 having briefly cleared Friday’s high of $1772.8 to open $1783.6 (Aug 16 high).

- In gas space, Asian and European gas is set for an eventful open tomorrow after Freeport LNG said it will likely cancel shipments scheduled for Nov-Dec as it continues to repairs and regulatory approval, with US gas paring gains accordingly. EU TTF prices had already increased 16% today ahead of the news.

Tuesday Data Calendar

| Date | GMT/Local | Impact | Flag | Country | Event |

| 15/11/2022 | 0200/1000 | *** |  | CN | Fixed-Asset Investment |

| 15/11/2022 | 0200/1000 | *** | | CN | Retail Sales |

| 15/11/2022 | 0200/1000 | *** | | CN | Industrial Output |

| 15/11/2022 | 0200/1000 | ** | | CN | Surveyed Unemployment Rate |

| 15/11/2022 | 0700/0700 | *** |  | UK | Labour Market Survey |

| 15/11/2022 | 0700/0800 | *** |  | SE | Inflation report |

| 15/11/2022 | 0745/0845 | *** |  | FR | HICP (f) |

| 15/11/2022 | 0800/0900 | *** |  | ES | HICP (f) |

| 15/11/2022 | 1000/1000 | ** | | UK | Gilt Outright Auction Result |

| 15/11/2022 | 1000/1100 | *** |  | DE | ZEW Current Conditions Index |

| 15/11/2022 | 1000/1100 | *** | | DE | ZEW Current Expectations Index |

| 15/11/2022 | 1000/1100 | * |  | EU | Trade Balance |

| 15/11/2022 | 1000/1100 | * | | EU | Employment |

| 15/11/2022 | 1000/1100 | *** | | EU | GDP First Estimates |

| 15/11/2022 | 1130/1130 | ** | | UK | Gilt Outright Auction Result |

| 15/11/2022 | - |  | ID | G20 Summit in Indonesia | |

| 15/11/2022 | - |  | TH | APEC Leaders’ Summit | |

| 15/11/2022 | 1330/0830 | *** |  | US | PPI |

| 15/11/2022 | 1330/0830 | ** | | US | Empire State Manufacturing Survey |

| 15/11/2022 | 1355/0855 | ** | | US | Redbook Retail Sales Index |

| 15/11/2022 | 1400/0900 | * |  | CA | CREA Existing Home Sales |

| 15/11/2022 | 1400/0900 | | US | Philadelphia Fed's Patrick Harker | |

| 15/11/2022 | 1400/0900 | | CA | BOC Deputy Kozicki moderates panel on diversity | |

| 15/11/2022 | 1400/0900 | | US | Fed Governor Lisa Cook | |

| 15/11/2022 | 1500/1000 | | US | Fed Vice Chair for Supervision Michael Barr | |

| 15/11/2022 | 1730/1830 | | EU | ECB Elderson Speech at Euro Finance Week |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.