Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- FED OFFICIALS PREPARING TO LIFT INTEREST RATES BY ANOTHER 0.75PPT (WSJ)

- SUNAK STILL THE APPARENT FAVOURITE AS UK TORY LEADERSHIP RACE INTENSIFIES

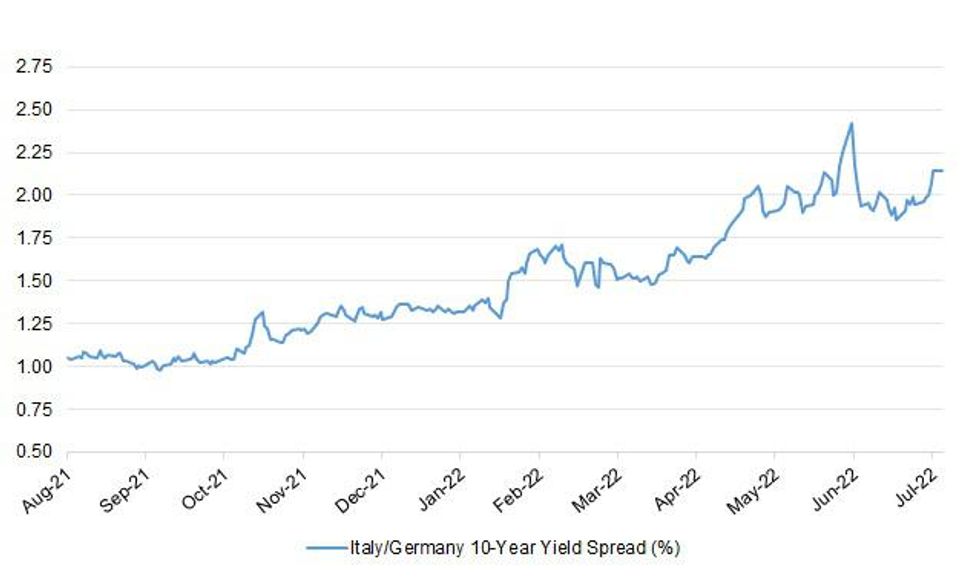

- DRAGHI IS SIGNALING THAT HE’S DETERMINED TO QUIT GOVERNMENT

- ITALY CENTER-RIGHT SAYS DRAGHI’S COALITION PACT HAS BEEN BROKEN

- SWISS CENTRAL BANK PLANS AT LEAST 50 BPS RATE HIKE IN SEPTEMBER, NEWSPAPER REPORTS

- CHINA SET TO UP ECONOMIC SUPPORT , EYES SUPPORT FOR PROPERTY SPACE ON MORTGAGE NON-PAYMENTS

- NO IMMEDIATE SAUDI PLEDGE FOR OIL OUTPUT HIKE AFTER BIDEN TRIP

Fig. 1: Italy/Germany 10-Year Yield Spread (%)

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

UK

POLITICS: Tory leadership rivals stepped up their attacks on each other's records and policies in their latest TV debate. (BBC)

POLITICS: Sunak, who currently has the most support among MPs in the Conservative leadership contest, on Sunday sought to reassure Eurosceptic Tories that he would take a tough stance on Brexit and “capitalise on the freedoms” it offered. But Johnson’s supporters are determined to stop Sunak, whom they said betrayed the prime minister, and are now mounting a sustained briefing campaign against him. (FT)

POLITICS: Almost half of Conservative voters believe Rishi Sunak would make a good prime minister, according to a poll that puts Penny Mordaunt behind both Liz Truss and the former chancellor. (Telegraph)

FISCAL: Tax cuts are being promised by several Conservative party leadership hopefuls, but a top official at the International Monetary Fund has warned it might be better to raise them instead. "I think debt-financed tax cuts at this point would be a mistake," said Mark Flanagan, who leads the Fund's UK team, speaking to BBC News. (BBC)

FISCAL: All five candidates for the Tory leadership vowed to impose real-terms pay cuts on millions of public sector workers as they held the second televised debate in the contest to succeed Boris Johnson as prime minister. Johnson is expected this week to accept the recommendation from various public pay bodies for an increase in salaries for state workers of close to 5 per cent. But union leaders have already threatened strikes, warning that this is far from enough when inflation has already soared past 9 per cent. (FT)

BOE: The Bank of England’s struggle to restrain the fastest inflation in four decades drew fire from two lawmakers seeking to become the UK’s next prime minister, with Foreign Secretary Liz Truss hinting she may change the central bank’s mandate if she wins power. (BBG)

EUROPE

FISCAL: Hungary says it is increasingly confident that pledges to wean itself off Russian fossil fuels and tackle corruption will enable it to strike a deal with Brussels aimed at unlocking billions of euros in recovery funding. (FT)

EU: North Macedonia’s parliament on Saturday gave Skopje’s government the go-ahead to resolve a dispute with neighboring Bulgaria, paving the way for EU membership talks to begin. (POLITICO)

ITALY: Mario Draghi has signaled that he’s determined to resign as Italy’s prime minister next week since he doesn’t have the backing of all the parties in his splintered governing alliance, according to people familiar with the matter. (BBG)

ITALY: The League and Forza Italia said Sunday that their alliance backing Prime Minister Mario Draghi has been broken, signaling the biggest political forces are readying for possible snap elections after the premier announced his resignation last week. (BBG)

SNB: The Swiss National Bank is currently planning to raise interest rates by 50 or 75 basis points in its next scheduled monetary policy announcement in September, a Swiss newspaper reported on Saturday, citing one or more people involved in the matter. (RTRS)

RATINGS: Sovereign rating reviews of note from Friday included:

- Fitch affirmed Luxembourg at AAA; Outlook Stable

- Moody's upgraded Croatia to Baa2; Outlook Stable

- Moody's affirmed Spain at Baa1; Outlook Stable

- DBRS Morningstar confirmed Ireland at AA (low), Stable Trend

BONDS: Dozens of corporate bond deals have failed to launch in recent months as the end of central bank stimulus leaves companies starved of cheap funds. (FT)

U.S.

FED: Federal Reserve officials have signaled they are likely to raise interest rates by 0.75 percentage point later this month, for the second straight meeting, as part of an aggressive effort to combat high inflation. Policy makers left the door open to a larger, full-percentage-point increase at the July 26-27 gathering. But some of them simultaneously poured cold water on the idea in recent interviews and public comments ahead of their premeeting quiet period, which began Saturday. (WSJ)

FED: More firms now expect inflation to exceed 5% over the longer run than any other outcome, according to the Atlanta Fed's latest business inflation expectations survey, a "worrisome" development in a high inflation environment, bank economist Brent Meyer told MNI. (MNI)

INFLATION: There are tentative signs consumers expect inflation to come down from recent highs as many feel gas prices may have crested and the economic outlook darkens, the head of the University of Michigan's Survey of Consumers, Joanne Hsu, told MNI. (MNI)

OTHER

U.S./CHINA/TAIWAN: The U.S. State Department has approved the potential sale of military technical assistance to Taiwan worth an estimated $108 million, the Pentagon said on Friday. (RTRS)

G20: Division over Russia’s war in Ukraine meant a meeting of Group of 20 finance chiefs ended without the usual communique, though there was incremental progress on issues such as food and energy security. (BBG)

AUSTRALIA: Australian Treasurer Jim Chalmers warned that his first budget update to parliament next week will have some “confronting” news on inflation, interest rates and wages. Chalmers, who took office in May, has said the new Labor government was inheriting the “trickiest” set of economic circumstances in living memory. He took over a budget forecasting a combined A$224.7 billion ($153.1 billion) in deficits over the next four years, providing little leeway for new spending plans. (BBG)

AUSTRALIA: A key union is threatening to pursue pay increases of 8 per cent, amid warnings of more strikes by workers angry at employers for what they claim are ‘low-ball’ wage offers. (The Australian)

RBNZ: The Reserve Bank today announced a facility to improve the anchoring of wholesale short-term interest rates at the Official Cash Rate (OCR). From 20 July 2022, the Reserve Bank will allow eligible counterparties to lend New Zealand dollars (NZD) through a Standing Repurchase (Repo) Facility. (Scoop NZ)

SOUTH KOREA: South Korea’s finance minister has shrugged off short-term risks of capital outflows from the Asian economy as gaps in global rates widen. (CNBC)

SOUTH KOREA: South Korea will exempt taxes on income from investing in Korean treasury bonds to attract foreign investment, Finance Minister Choo Kyung-ho told reporters in Bali, according to a statement from the ministry. (RTRS)

BOC: The Bank of Canada expects inflation to go "a little over" 8%, as soon as next week when June's data is released, and stay in that range for a few more months, Governor Tiff Macklem told a business group in a webcast transcript released late Friday. (RTRS)

BOC: The Bank of Canada will likely dial back to half-point interest rate hikes after Wednesday's surprise full-point move sent a clear message about winning the inflation fight, former central bank and finance department adviser Chris Ragan told MNI. (MNI)

MEXICO: Mexico’s peso strength favors importers and affects exporters, Deputy Central Bank Governor Gerardo Esquivel wrote in a series of tweets on Sunday. Setting the exchange rate isn’t a goal of monetary policy, but it’s a factor in decision-making. (BBG)

RUSSIA: Agreements on export of the Ukrainian grain will not lead to the resumption of Russia-Ukraine talks, Leonid Slutsky, a Russian lawmaker who had taken part in peace talks with Kyiv in the past, said on Friday, state news agency TASS reported. Russia's proposals on how to resume Ukrainian grain exports were "largely supported" by negotiators at talks this week in Istanbul and an agreement was close, the Russian defence ministry said on Friday. (RTRS)

RUSSIA: Russian Defence Minister Sergei Shoigu has ordered Russian military units operating in all areas of Ukraine to step up their operations in order to prevent strikes on eastern Ukraine and other territories controlled by Russia, the ministry said in a statement on its website on Saturday. (RTRS)

RUSSIA: President Volodymyr Zelenskyy fired the head of Ukraine’s state security service and the chief prosecutor on Sunday over allowing alleged treachery and collaboration by scores of their officials with Russian forces in occupied territories. Announcing the sackings in his nightly television address, Zelenskyy said more than 60 staff belonging to the two law enforcement agencies had “remained in the occupied territory and are working against our state” (FT)

RUSSIA: The EU’s foreign policy chief defended the Western focus on economic sanctions against Vladimir Putin’s regime, saying the measures are working, and urging “strategic patience” at a time Moscow has indicated it’s ramping up its war effort. (BBG)

RUSSIA: The Japanese government has urged trading houses Mitsui & Co. and Mitsubishi Corp. to maintain their stakes in Russia's Sakhalin-2 liquefied natural gas project under its new operator. (Nikkei)

RUSSIA: The Ukrainian government has told US and European bank bosses to sever ties with groups that trade Russian oil, as a top aide to president Volodymyr Zelenskyy accused the lenders of “war crimes”. (FT)

SOUTH AFRICA: The chief executive of South Africa's state power utility Eskom, Andre de Ruyter, said on Saturday rolling power cuts should come to an end by the end of next week. (RTRS)

IRAN: Iran is technically capable of making a nuclear bomb but has not decided whether to build one, a senior adviser to Iranian Supreme Leader Ayatollah Ali Khamenei told Qatar's al Jazeera TV on Sunday. (RTRS)

IMF: The International Monetary Fund will cut its global economic growth outlook “substantially” in its next update, as finance chiefs grapple with a shrinking list of options to address the worsening risks. (BBG)

ENERGY: The risk of a cutoff in Russian gas supplies appears to be fully priced by the market, the head of Germany’s top power grid regulator said in an interview. (BBG)

ENERGY: Europe will need to ration natural gas to meet winter heating demand if the Nord Stream pipeline doesn’t restart after planned maintenance, according to Ineos Group. (BBG)

OIL: President Joe Biden said he expects further oil supply increases from Saudi Arabia to help tame fuel costs at home after a landmark meeting with the kingdom’s rulers. Biden’s trip didn’t result in an immediate pledge for a production hike, but US officials said they were confident that Riyadh would lead the OPEC+ alliance to an agreement for a gradual boost. (BBG)

OIL: Saudi Arabia's foreign minister said a U.S.-Arab summit on Saturday did not discuss oil and that OPEC+ would continue to assess market conditions and do what is necessary. (RTRS)

OIL: Saudi Arabia's Crown Prince Mohammed bin Salman said on Saturday more investment was needed in fossil fuel and clean energy technologies to meet global demand, and that unrealistic emission policies would lead to unprecedented levels of inflation. The prince said Saudi Arabia had announced raising its production capacity to 13 million barrels per day by 2027 from a nameplate capacity of 12 million now and "after that the Kingdom will not have any more capability to increase production". (RTRS)

OIL: Libya’s National Oil Corp (NOC) is continuing to do its job according to the law, it said on its social media feeds on Sunday, days after the Government of National Unity (GNU) sought to replace the NOC chief and its board of directors. (RTRS)

OIL: Libya, which replaced the board of state-owned National Oil Corp., is loading its first cargo of condensate since the lifting of force majeure from all ports and fields, though the legitimacy of the company's new leadership remains contested. (Platts)

OIL: U.S. Treasury Secretary Janet Yellen will meet with South Korean President Yoon Suk-yeol and other senior officials in Seoul on Tuesday as she wraps up her first visit as secretary to the Indo-Pacific region, the Treasury Department said. During her meetings in Seoul, Yellen will continue to push for a proposed cap on the price of Russian oil and discuss efforts to address supply chain bottlenecks through "friendshoring" - or boosting trade ties with trusted economic partners like South Korea, Treasury said. (RTRS)

CHINA

ECONOMY: China is likely to reach an over 5% GDP growth in the second half and the country should not pursue an overly high target on stimulus which will hurt long-term development, said advisors and former officials in a summit held by China Wealth Management 50 Forum on Saturday. (MNI)

PBOC: China’s central bank will step up the implementation of its prudent monetary policy to provide stronger economic support, Governor Yi Gang said. (BBG)

PBOC: China’s monetary policy has sufficient space and tools to cope with any new challenges in the second half of the year, the Economic Daily said in a commentary. There is still room for lowering the reserve requirement ratio, as the weighted average deposit reserve ratio of financial institutions is currently 8.1%, the newspaper said. Meanwhile, the foreign exchange market is more resilient with more stable cross-border capital flows, as market players are more adaptable and tolerant to the ups and downs of the yuan, providing a better foundation to resist external shocks, the daily said. (MNI)

PBOC: The People's Bank of China should save policy ammunition to prevent a surge in debt as market liquidity has been excessive and it should focus instead on boosting credit in the property sector in the second half, PBOC advisors and former officials said in a summit held by China Wealth Management 50 Forum on Saturday. (MNI)

ECONOMY: Chinese Vice Premier Hu Chunhua called on local governments to stabilize employment with “stronger and more effective measures,” Xinhua News Agency reported late Sunday. Promoting employment of college graduates should be placed at an important position, Hu said during a visit to eastern province of Zhejiang. Hu also pledged support for migrant workers to return to their hometown and start a business there. (BBG)

CORONAVIRUS: China’s Covid-19 cases remain elevated, with Shanghai rolling out mass testing in nine districts as the financial hub seeks to stamp out infections, while the gaming enclave of Macau extended its lockdown. Tianjin, a port city near Beijing, also plans a mass-testing drive after finding two cases, CCTV reported. (BBG)

BANKS/PROPERTY: China's banking and insurance regulator vowed on Sunday to handle the risks associated with five rural banks in Henan and Anhui provinces in accordance with laws and regulations, as well as to ensure financial services for the delivery of home projects. (Global Times)

CHINA MARKETS

PBOC INJECTS NET CNY9 BILLION VIA OMOS MONDAY

The People's Bank of China (PBOC) injected CNY12 billion via 7-day reverse repos with the rate unchanged at 2.1% on Monday. This led to a net injection of CNY9 billion after offsetting the maturing CNY3 billion reverse repos today, according to Wind Information.

- The operation aims to keep liquidity reasonable and ample, the PBOC said on its website.

- The 7-day weighted average interbank repo rate for depository institutions (DR007) rose to 2.0500% at 9:43 am local time from the close of 1.5602% on Friday.

- The CFETS-NEX money-market sentiment index closed at 48 on Friday vs 42 on Thursday.

PBOC SETS YUAN CENTRAL PARITY AT 6.7447 MON VS 6.7503

The People's Bank of China (PBOC) set the dollar-yuan central parity rate lower at 6.7447 on Monday, compared with 6.7503 set on Friday.

OVERNIGHT DATA

NEW ZEALAND Q2 CPI +7.3% Y/Y; MEDIAN +7.1%; Q1 +6.9%

NEW ZEALAND Q2 CPI +1.7% M/M; MEDIAN +1.5%; Q1 +1.8%

NEW ZEALAND JUN PERFORMANCE SERVICES INDEX 55.4; MAY 55.3

Activity levels for New Zealand's services sector in June displayed almost identical levels to last month, according to the BNZ - BusinessNZ Performance of Services Index (PSI). The fact that the two key sub-indexes of New Orders/Business (61.7) and Activity/Sales (56.5) remained at very healthy levels of expansion has more than compensated with other issues at play, such as supplier deliveries (47.8) still stuck in contraction. (BusinessNZ)

NEW ZEALAND JUN NON-RESIDENT BOND HOLDINGS 58.4%; MAY 58.3%

UK JUN RIGHTMOVE HOUSE PRICES +0.4% M/M; MAY +0.3%

UK JUN RIGHTMOVE HOUSE PRICES +9.3% Y/Y; MAY +9.7%

MARKETS

SNAPSHOT: Back To 75

Below gives key levels of markets in the second half of the Asia-Pac session:

- Nikkei 225 is closed

- ASX 200 up 55.129 points at 6660.7

- Shanghai Comp. up 48.108 points at 3276.169

- JGBs are closed

- Aussie 10-Yr future down 0.5 ticks at 96.545, yield up 0.6bp at 3.414%

- U.S. 10-Yr future +0-06+ at 118-27, yield down 4.43bp at 2.915%

- WTI crude up $0.29 at $97.88, Gold up $6.5 at $1714.67

- USD/JPY down 25 pips at Y138.32

- FED OFFICIALS PREPARING TO LIFT INTEREST RATES BY ANOTHER 0.75PPT (WSJ)

- SUNAK STILL THE APPARENT FAVOURITE AS UK TORY LEADERSHIP RACE INTENSIFIES

- DRAGHI IS SIGNALING THAT HE’S DETERMINED TO QUIT GOVERNMENT

- ITALY CENTER-RIGHT SAYS DRAGHI’S COALITION PACT HAS BEEN BROKEN

- SWISS CENTRAL BANK PLANS AT LEAST 50 BPS RATE HIKE IN SEPTEMBER, NEWSPAPER REPORTS

- CHINA SET TO UP ECONOMIC SUPPORT , EYES SUPPORT FOR PROPERTY SPACE ON MORTGAGE NON-PAYMENTS

- NO IMMEDIATE SAUDI PLEDGE FOR OIL OUTPUT HIKE AFTER BIDEN TRIP

US TSYS: Futures Better Bid On Fed Exp., Market Limited By Japanese Holiday

TYU2 deals +0-06 ahead of London hours, printing 118-26+, 0-03 off its session peak, although volume is sub-par running at ~35K lots, with the illiquidity inked to a Japanese national holiday and the resultant close of cash Tsys until London trade limiting wider activity.

- Tsy futures drew support from Friday’s Fedpeak (where only ’22 voter Bullard pointed to the need for a potential 100bp rate hike later this month) and a weekend article from WSJ Fed whisperer Timiraos, who flagged that a 75bp rate hike is the most likely scenario come the end of the central bank’s July meeting.

- Continued COVID worry in China, alongside an early downtick in crude oil futures, also fed into the early bid, although a subsequent recovery in the latter, alongside an uptick in e-minis & Chinese equities (which benefitted from the hope of apparent impending support for Chinese property developers, per weekend press reports surrounding comments from a CBIRC official) limited the early bid, with Tsy futures operating off of best levels into European hours as a result.

- Looking ahead, only second tier domestic data is due later today, while the Fed has entered its pre-FOMC blackout period.

AUSSIE BONDS: Twist Flattening

ACBGs edged away from cheapest levels witnessed after the release of firmer than expected NZ inflation data as we worked our way through the Sydney day, with an uptick in U.S. Tsy futures on previously fleshed-out reactions to Friday’s market moves, Fed expectations and developments in China’s ongoing COVID outbreak lending support to the space. The cash ACGB curve has twist flattened, with the major benchmarks running 0.5bp richer to 5.0bp cheaper across the curve, pivoting around 20s. YM and XM are -2.5 and -1.5, a little below their respective session highs but getting nowhere near to challenging the boundaries of their overnight ranges, while bills run 2 to 5 ticks cheaper through the reds, bear steepening.

- Looking ahead, Tuesday will see the RBA release the minutes of its Jul policy meeting, with a speech by RBA Deputy Gov Bullock (on “How are Households Placed for Interest Rate Increases?”) due to cross after the minutes.

EQUITIES: Higher In Asia; Chinese Developers Halt Five-Day Slide As Banking Regulator Steps In

Major Asia-Pac equity indices are higher at typing on a positive lead from Wall St. following Friday’s U.S. data, with Chinese and Hong Kong markets outperforming in the wake of statements from PBOC Governor Yi Gang on Saturday and banking regulator China Banking and Insurance Regulatory Commission (CBIRC) re: weaker growth and well-documented woes faced by Chinese developers respectively. Japanese markets are shut for a holiday.

- The Hang Seng leads gains amongst regional peers, dealing 2.6% firmer at typing on the back of gains in almost every constituent. The property (+3.2%) and financial (+2.4%) sub-indices outperformed, with both on track to snap a five-session streak of lower closes, likely catching a bid on a statement from Chinese banking regulator CBIRC on Monday urging banks to provide credit for developers to complete unfinished projects.

- The CSI300 sits 1.2% better off at typing after reversing earlier losses of as much as 0.7%, with the real estate (+2.8%) and financials (+1.9%) sub-gauges contributing the most to gains.

- The ASX200 deals 0.8% firmer, just shy of session highs at writing. Tech stocks lead gains, with the S&P/ASX All Technology Index adding 1.9%, while commodity-related equities tracked a rally in commodity prices higher (BCOM: +0.8%), with the materials and energy sub-indices sitting 1.7% and 2.0% better off respectively.

- E-minis trade 0.3% to 0.7% higher, operating around session highs at typing.

OIL: Back From Lows; Supply Outlook Remains Tight After Biden’s Visit To Saudi Arabia

WTI is ~$0.60 and Brent is ~+$0.90 at typing, operating around session highs and building on Friday’s gains after reversing earlier losses.

- To recap, both benchmarks closed ~$2 firmer apiece on Friday as U.S. Pres Biden landed in Saudi Arabia, with a lack of concrete, near-term measures re: crude output increases observed. State Dept advisor Hochstein has since stated that producers will take "more steps in the coming weeks" (without naming specific countries/targets), while Saudi officials have re-iterated that supply decisions would be made in consultation with OPEC+.

- The prompt Brent spread remains elevated, operating around ~$3.95 at typing, pointing to persistent tightness in the outlook for crude supplies.

- Libya’s new state oil company chairman has stated that production will be fully restored within a week, potentially returning >500K bpd in output to global supplies.

- Elsewhere, worry surrounding lower energy demand in China remains elevated as fresh daily COVID cases for Sun were reported at 510, after Sat’s 580 cases (two-month high). Shanghai has also ordered mass testing in 9 of 16 districts, with authorities describing the situation as “severe”, while BBG reports have pointed to mass testing to be conducted in Tianjin (pop. ~13.8mn).

- BBG source reports have highlighted that Indian fuel demand in July so far has declined M/M (albeit as expected during the monsoon season), adding to wider worry re: cooling Asian energy demand.

GOLD: Higher In Asia; 11-Month Lows Eyed

Gold sits ~$6/oz firmer to print $1,714/oz, operating a little shy of Friday’s best levels at typing. The precious metal has caught a bid as China reported >500 fresh COVID cases for another day while the USD has weakened, with the DXY continuing to back away from recent cycle highs as participants in Asia react to previously-flagged Fedspeak (with focus re: possibility of a 100bp rate hike in Aug), as well as softening long-term inflation expectations from Friday’s UoM survey.

- To recap, gold closed little changed on Friday after repeated tests of the $1,700/oz handle, staying clear of Thursday’s 11-month lows ($1,697.7/oz). Bullion recorded a fifth straight week of losses (~$170/oz in all) amidst well-documented Dollar strength, with rate hike expectations for the Fed’s Aug FOMC ticking higher across the week (~74bp to ~80bp, referencing FOMC dated OIS).

- The European Commission has formally proposed a ban on Russian imports of gold (following the G7 announcement in June), with RTRS sources suggesting possible bans on imports through third countries. As mentioned previously, the measure is expected to have limited impact on the space, given prevailing EU sanctions since Mar ‘22.

- From a technical perspective, gold remains in a downtrend. Initial support is located at $1,690.6/oz (Aug 9 ‘21 low), while resistance is situated at $1,745.4/oz (Jul 13 high).

FOREX: Kiwi Draws Incremental Support From Inflation Data, Greenback Sags Lower

New Zealand's expectation-busting inflation print fanned hawkish RBNZ bets, providing a key data input ahead of the August Monetary Policy Statement. Headline inflation accelerated to +7.3% Y/Y (32-year high), surpassing BBG median estimate of +7.1% and the +7.0% forecast in the May MPS.

- The RBNZ's own gauge of core inflation reaffirmed the view that price pressures have intensified. Sectoral factor model inflation quickened to a record high of +4.8% Y/Y, with readings for the three preceding quarters revised higher.

- The market reacted by adding hawkish RBNZ tightening bets, with benchmark NZ 2-year swaps rising to a new monthly high & NZGB yield curve bear flattening.

- Several sell-side desks reconsidered their RBNZ calls. ANZ said they now forecast a terminal OCR level of 4.0% (prev. 3.5%) and warned that "a 75bp hike at the August MPS is a very real possibility," while ASB lifted their projection of OCR peak to 4.75% from 3.50%.

- The kiwi dollar caught a bid as StatsNZ published its CPI report, albeit reaction to sectoral factor model inflation was virtually non-existent. That said, the currency's strength gradually petered out, with AUD/NZD returning to neutral levels.

- The greenback remained the worst performer among major currencies throughout the Asia-Pac session, with regional players playing catch-up with U.S. data/Fedspeak from after local hours Friday.

- Traditional safe havens JPY and CHF struggled for any topside impetus as U.S. e-mini futures crept higher.

- Japanese financial markets were closed in observance of a public holiday, limiting liquidity in the timezone.

- The global data docket remains feather-light after Asia hours. BoE's Saunders is the only G10 central bank member due to speak.

FX OPTIONS: Expiries for Jul18 NY cut 1000ET (Source DTCC)

- EUR/USD: $0.9975(E689mln), $1.0000(E1.1bln), $1.0150-60(E1.1bln)

- USD/CNY: Cny6.7750($1.7bln)

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 18/07/2022 | - |  | UK | BOE Saunders at Resolution Foundation (Time TBA) | |

| 18/07/2022 | 1215/0815 | ** |  | CA | CMHC Housing Starts |

| 18/07/2022 | 1400/1000 | ** |  | US | NAHB Home Builder Index |

| 18/07/2022 | 1530/1130 | * | | US | US Treasury Auction Result for 13 Week Bill |

| 18/07/2022 | 1530/1130 | * | | US | US Treasury Auction Result for 26 Week Bill |

| 18/07/2022 | 2000/1600 | ** | | US | TICS |

| 19/07/2022 | 0600/0700 | *** | | UK | Labour Market Survey |

| 19/07/2022 | 0800/1000 |  | EU | ECB Bank Lending Survey | |

| 19/07/2022 | 0900/1100 | *** | | EU | HICP (f) |

| 19/07/2022 | 0900/1000 | ** | | UK | Gilt Outright Auction Result |

| 19/07/2022 | 0900/1100 | ** | | EU | Construction Production |

| 19/07/2022 | 1230/0830 | *** | | US | Housing Starts |

| 19/07/2022 | 1255/0855 | ** | | US | Redbook Retail Sales Index |

| 19/07/2022 | 1745/1845 | | UK | BOE Bailey at Mansion House Dinner |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.