Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- ITALY WILL NOT USE THE EU’S ESM BAILOUT FUND, MELONI SAYS (BBG)

- POLAND SUES EU OVER FINES FOR RULE-OF-LAW INFRINGEMENTS (BBG)

- CHINA'S SOARING COVID CASES PUSH ECONOMIC ACTIVITY OFF A CLIFF (BBG)

- BEIJING DRAWS DOCTORS AND STAFF FROM PROVINCES TO EASE OVERWHELMED HOSPITALS (SCMP)

- YUAN COULD RALLY TO 6.5 BUT VOLATILITY AHEAD (MNI)

- NOVAK: RUSSIA MAY CUT OIL OUTPUT IN RESPONSE TO PRICE CAPS (RTRS)

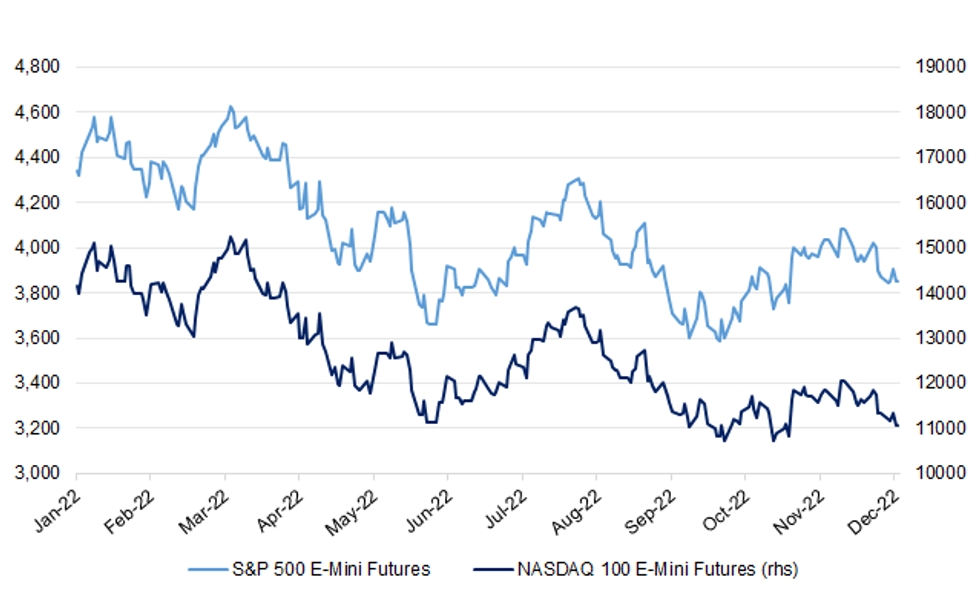

Fig. 1: S&P 500 & NASDAQ 100 E-Mini Futures

Source: MNI - Market News/Bloomberg

EUROPE

EU: Poland filed a complaint against the European Union’s executive to the bloc’s top court to stop the commission from levying a €1 million ($1.1 million) a day fine over the country’s contested mechanism for disciplining judges. (BBG)

ITALY: Italy will not use the European Stability Mechanism bailout fund, Premier Giorgia Meloni said in an interview on Rai national television show Porta a Porta. (BBG)

ITALY: Italy's government asked on Thursday for the lower house of parliament to hold a confidence vote on the 2023 budget to speed up its approval and ensure the package becomes law by the end of this year. (RTRS)

U.S.

ECONOMY/INFLATION: U.S. President Biden wrote the following in a Yahoo op-ed: “Americans have been through a tough few years, but I am optimistic about our country’s economic prospects. Americans’ resilience has helped us recover from the economic crisis created by the COVID-19 pandemic, families are finally getting more breathing room, and my economic plan is making the United States a powerhouse for innovation and manufacturing once again.” (MNI)

FISCAL: The Senate approved a $1.7 trillion government funding bill on Thursday, sending the legislation to the House, where it is expected to pass in time to beat a Friday night deadline to avert a partial federal government shutdown. (CNBC)

POLITICS: The House Jan. 6 committee late Thursday unveiled its formal eight-chapter report summarizing its investigation into the deadly attack on the Capitol. (NBC)

EQUITIES: Elon Musk said Thursday afternoon in a Twitter Spaces that he’s not selling any Tesla stock next year "under any circumstances." (Axios)

OTHER

GLOBAL TRADE: TSMC is in advanced talks with key suppliers about setting up its first potential European plant in the German city of Dresden, a move that would allow the world's largest chipmaker to capitalize on booming demand from the region's car industry. (Nikkei)

U.S./CHINA: US Indo-Pacific Command says it is closely tracking China military activities in the South China Sea, Philippine Sea, and ongoing Russia-China exercise in the East China Sea, according to a statement. (BBG)

U.S./CHINA: US Secretary of State Antony Blinken spoke with China Foreign Minister Wang Yi in a call today, according to an readout from the State Department. Blinken discussed the need to maintain open lines of communication and responsibly manage the US-China relationship. (BBG) Discussed the current Covid-19 situation and raised concerns about Russia-Ukraine war. (BBG)

The United States must stop suppressing China's development and should not continue the "old routine of unilateral bullying", Chinese Foreign Minister Wang Yi told U.S. Secretary of State Antony Blinken, according to a press statement. (RTRS)

U.S./CHINA: It is important for all countries, including China, to share information with the world about what they're experiencing with COVID-19, U.S. Secretary of State Antony Blinken said on Thursday, as some health experts have questioned whether China might be hiding information on the extent of its outbreak. (RTRS)

JAPAN: Japanese Prime Minister Fumio Kishida is considering reshuffling his cabinet early next year in the hopes of buoying his public support, Sankei reports, citing unidentified government and ruling party officials. (BBG)

BOK: South Korea's central bank said on Friday its interest rate policy next year would continue to target containing inflation, which it said is expected to slow though a huge amount of uncertainty lies ahead. (CNA)

SOUTH KOREA: Prime Minister Han Duck-soo said Friday the government will decide when to lift the indoor mask mandate, the country's last remaining COVID-19 restriction, if two of four criteria are met, such as a fall in severe cases and deaths. (Yonhap)

NORTH KOREA/RUSSIA: North Korea's foreign ministry denied reports it offered munitions to Russia, calling it "groundless," and denounced the United States for providing lethal weapons to Ukraine, the North's official KCNA news agency reported on Friday. (RTRS)

MEXICO: Mexico’s Finance Ministry plans to renew in February its inflation pact with big businesses that aims to contain the cost of basic goods by removing import barriers and red tape, according to people familiar with the matter. (BBG)

BRAZIL: Brazil's incoming finance minister Fernando Haddad on Thursday said Rogerio Ceron will be the country's treasury secretary. In a press conference, Haddad also picked Marcos Barbosa Pinto as the ministry's secretary for economic reforms. (RTRS)

RUSSIA: President Vladimir Putin said on Thursday that Russia wants an end to the war in Ukraine and that this would inevitably involve a diplomatic solution. (RTRS)

ARGENTINA: The International Monetary Fund’s executive board approved the third review of Argentina’s $44 billion program Thursday, clearing a key hurdle for the government to receive more money as the economy shows signs of slowdown. (BBG)

ENERGY: Russia's natural gas output will fall by up to a fifth this year to 671 billion cubic metres , the Interfax news agency cited Deputy Prime Minister Alexander Novak as saying on Friday, as exports to Europe have plunged. Russia's oil output is seen rising 2% this year to 535 million tonnes, Intefax cited Novak as telling state television. (RTRS)

ENERGY: Russian President Vladimir Putin signed a decree on application of special economic measures in the sphere of natural gas supplies due to unfriendly actions of the US and countries and organizations joining such actions. (TASS)

OIL: The U.S. Treasury Department said late on Wednesday that shipments facing the G7’s upcoming price cap on oil products such as diesel and gasoline from Russia will have a grace period to arrive at their destination. (RTRS)

CHINA

CORONAVIRUS: China has sent hundreds of healthcare workers, some specialising in critical care, to the capital Beijing to ease the burden at heavily strained hospitals amid a tsunami of infections. (SCMP)

ECONOMY: China’s GDP predicted to expand by more than 5% next year, Securities Daily reported, citing five economists. (BBG)

ECONOMY: China’s economy will rebound next year, but the strength of recovery is uncertain said experts at the 4th Bund Finance Summit, co-hosted by the China Finance 40 Forum (CF40). (MNI)

ECONOMY: China’s soaring Covid infections are keeping people home and causing a slump in travel and economic activity, according to the latest high-frequency data. (BBG)

YUAN: The Chinese yuan could rally to 6.5 against the U.S. dollar in the second half of 2023 on capital inflows and a weaker U.S. dollar, though two-way volatility is likely early in the year as an economic recovery navigates rising Covid cases, a senior policy adviser told MNI. (MNI)

PROPERTY/CREDIT: Debt-laden developer Evergrande said disagreements are narrowing in its offshore debt restructuring plan, though it also admitted great uncertainty on repayment given the company’s massive debts and challenging business situation, Caixin reported. (MNI)

PROPERTY: Upper tier-2 cities in China have taken steps to increase demand for property purchases, according to Yicai.com. (MNI)

CHINA MARKETS

PBOC NET INJECTS CNY164 BILLION VIA OMOS FRIDAY

The People's Bank of China (PBOC) on Friday injected CNY2 billion via 7-day reverse repos, and CNY203 billion via 14-day reverse repos with the rates unchanged at 2.00% and 2.15%, respectively. The operation has led to a net injection of CNY164 billion after offsetting the maturity of CNY41 billion reverse repos today, according to Wind Information.

- The operations aim to keep year-end liquidity stable, the PBOC said on its website.

- The 7-day weighted average interbank repo rate for depository institutions (DR007) rose to 2.0000% at 9:26 am local time from the close of 1.5345% on Thursday.

- The CFETS-NEX money-market sentiment index closed at 44 on Thursday vs 45 on Wednesday.

PBOC SETS YUAN CENTRAL PARITY AT 6.9810 FRI VS 6.9713 THURS

The People's Bank of China (PBOC) set the dollar-yuan central parity rate higher at 6.9810 on Friday, compared with 6.9713 set on Thursday.

OVERNIGHT DATA

JAPAN NOV CPI +3.8% Y/Y; MEDIAN +3.9%; OCT +3.7%

JAPAN NOV CPI EX-FRESH FOOD +3.7% Y/Y; MEDIAN +3.7%; OCT +3.6%

JAPAN NOV CPI EX-FRESH FOOD & ENERGY +2.8% Y/Y; MEDIAN +2.8%; OCT +2.5%

AUSTRALIA NOV PRIVATE SECTOR CREDIT +0.5% M/M; MEDIAN +0.5%; OCT +0.5%

AUSTRALIA NOV PRIVATE SECTOR CREDIT +8.9% Y/Y ; MEDIAN +9.0%; OCT +9.0%

MARKETS

SNAPSHOT: No Last-Ditch Santa Rally In Asia

Below gives key levels of markets in the second half of the Asia-Pac session:

- Nikkei 225 down 257.86 points at 26250.01

- ASX 200 down 44.801 points at 7107.7

- Shanghai Comp. down 8.088 points at 3046.343

- JGB 10-Yr future down 11 ticks at 146.14, yield down 0.5bp at 0.395%

- Aussie 10-Yr future down 3.0 ticks at 96.155, yield up 3.3bp at 3.828%

- U.S. 10-Yr future down -0-06 at 113-11+, yield up 0.92bp at 3.6878%

- WTI crude up $0.78 at $78.27, Gold up $2.54 at $1795.06

- USD/JPY up 34 pips at Y132.69

- ITALY WILL NOT USE THE EU’S ESM BAILOUT FUND, MELONI SAYS (BBG)

- POLAND SUES EU OVER FINES FOR RULE-OF-LAW INFRINGEMENTS (BBG)

- CHINA'S SOARING COVID CASES PUSH ECONOMIC ACTIVITY OFF A CLIFF (BBG)

- BEIJING DRAWS DOCTORS AND STAFF FROM PROVINCES TO EASE OVERWHELMED HOSPITALS (SCMP)

- YUAN COULD RALLY TO 6.5 BUT VOLATILITY AHEAD (MNI)

- NOVAK: RUSSIA MAY CUT OIL OUTPUT IN RESPONSE TO PRICE CAPS (RTRS)

US TSYS: Marginally Cheaper In Asia, PCE Due Before Christmas

Tsys were biased lower overnight on the Asia-Pac reaction to Thursday’s cheapening in wider core global FI markets, leaving TYH3 -0-06+ at 113-11 into London hours, 0-01 off the base of its narrow 0-05+ range, on modest volume of ~46K. Cash Tsys sit 0.5-1.5bp cheaper across the curve, with marginal bear steepening in play.

- Tsys ticked lower alongside an uptick in the USD & weakness in e-minis during the early rounds of Asia-Pac dealing, with cross-asset flows at the fore, before stabilising as e-minis pared losses and the broader DXY moved back to neutral levels.

- Macro headline flow was fairly limited, with an as expected uptick in Japanese inflation, comments from President Biden stressing that inflation will take some time to normalise and the usual rounds of critique out of China re: U.S. views/actions towards the country all noted.

- Looking ahead PCE readings provide the focal point of Friday’s NY session, although this will of course come against a thinner liquidity backdrop owing to the time of the year, which will limit risk taking capabilities/desire.

- Tsys will be subjected to curtailed trading hours ahead of the Christmas weekend (see earlier bullet for more details).

JGBS: Futures Hold Cheaper, Curve Twist Flattens

JGB futures consolidated around overnight closing levels after a two-way start to Tokyo trade. That leaves the contract -15 into the bell, with 7s providing the weakest point on the curve on the weakness in futures (~2bp cheaper on the day), while wider JGBs observe some twist flattening.

- 10-Year yields continue to hover around the ~40bp mark, 10bp shy of the BoJ’s new YCC cap.

- Local headline flow saw the 3 major Y/Y CPI readings print broadly in line with expectations, once again ticking higher in November, while reports did the rounds re: a potential January cabinet reshuffle from PM Kishida.

- Looking ahead, PPI services data headlines the local docket on Monday, with the labour market report and retail sales prints due on Tuesday. Tuesday will also bring the latest round of 2-Year JGB supply.

AUSSIE BONDS: Cheapening Into Christmas

Aussie bonds nudged away from worst levels into the pre-Christmas close, after the impact of Thursday’s cheapening in core global FI markets applied some weight to the space in Sydney hours.

- Both YM & XM printed through their overnight lows, settling -5.0 & -3.0, respectively, while wider cash ACGB trade saw a similar degree of bear flattening. The AU/U.S. 10-Year yield spread continues to hover around multi-month highs, in the ~+15bp zone.

- Bills were 2-7bp cheaper through the reds, while RBA dated OIS pricing was little changed to a touch higher, looking for 18-19 of tightening at the Feb ’23 meeting, alongside a terminal cash rate of ~3.85%.

- Broader news flow was limited, with domestic private sector credit data printing in line with wider expectations.

- The domestic docket is empty between Christmas and NY.

NZGBS: Marginally Cheaper Come The Close, Early Cheapening Holds

There was little in the way of net movement for NZGBs after the early modest cheapening that came in the wake of Thursday’s light cheapening in core global FI markets. That left the major NZGB benchmarks ~3bp cheaper across the curve at the close, while swap rates were ~2bp higher across the term structure. RBNZ dated OIS is little changed on the day, with Feb ’23 meeting pricing indicating just over 70bp of tightening, alongside a terminal OCR of ~5.55%.

- We didn’t receive any notable domestic news flow, with macro headlines also on the light side.

- There isn’t anything in the way of meaningful domestic points of note slated between Christmas and the turn of the year.

GOLD: Unchanged For The Week, But Technicals Still Appear Positive

Gold has been range bound so far today, currently close to $1793.5, slightly higher for the session. This comes after yesterday's -1.2% drop. At this stage, gold is tracking close to unchanged for the past week.

- Better US data, coupled with a rebound in yields, has crimped the precious metals move above $1800, at least for now. Recent highs remain capped just above $1820.

- On the downside, the 20-day EMA at $1784.74 looks to be a support point and is trending higher, which is a positive from a technical standpoint. The simple 200-day is also near by at $1783.8.

OIL: Tracking Higher For The Week, Russia May Cut Production By 5-7% In Early 2023

Despite Thursday's dip, Brent crude is tracking +3.36% higher for the week, a similar gain to last week. We last tracked near $81.65/bbl, close to the 20-day EMA at $82.06/bbl, beyond that is recent highs between $83/$84/bbl. WTI is close to $78.50/bbl, and on track for a stronger gain this week, +5.72% at this stage.

- Headlines crossed a short while ago that Russia may cut oil output by 5-7% in early 2023 in response to the price caps introduced at the start of the month. This is between 500-700k barrels per day per Bloomberg reports.

- Supply side issues are likely to be the main focus point as we progress in the first part of 2023.

- The drop in US oil inventories, reported earlier in the week, has been supportive, while the market remains wary of the impact of US winter storms and the potential for further supply disruptions in the near term.

FOREX: Safe Havens Edge Down, NZD Claws Back Some Underperformance

Earlier trends have mostly stayed on track as we progress into the Asian afternoon session. Safe havens in terms of JPY and CHF remain underperformers, while higher beta plays have seen modest outperformance against these plays and the USD.

- This largely owes to the slightly better tone from equities, although market participants are unlikely to be putting on much fresh risk ahead of the Christmas holiday period.

- USD/JPY currently tracks close to 132.65, down slightly from session highs near 132.80. US cash Tsy yields are off intra-day highs as well.

- NZD/USD has rebounded by nearly 0.50%, the pick of the high beta plays. We were last around 0.6275, but this unwinds only a small proportion of the past week's underperformance.

- AUD/USD is back above 0.6680, +0.20% for the session. The AUD/NZD cross has corrected lower though, back sub 1.0650, versus yesterday's highs near 1.0720.

- Coming up, the main focus is likely to be on US data due, with the PCE deflator, durable good orders, U. of Mich. consumer sentiment and new home sales all set to print.

FX OPTIONS: Expiries for Dec23 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0300(E754mln), $1.0400-15(E900mln), $1.0500(E1.4bln), $1.0550(E969mln), $1.0800(E1.6bln)

- USD/JPY: Y130.00-10($981mln), Y132.00($548mln), Y134.00($690mln), Y135.00($1.8bln)

- GBP/USD: $1.2000(Gbp860mln), $1.2100(Gbp511mln)

- AUD/USD: $0.6650-55(A$607mln), $0.6710-25(A$852mln)

- USD/CAD: C$1.3570-75($611mln), C$1.3665-75($933mln)

- USD/CNY: Cny6.8580($1.1bln), Cny6.9000($965mln), Cny7.0460($1.5bln)

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 23/12/2022 | 0745/0845 | ** |  | FR | PPI |

| 23/12/2022 | 0800/0900 | ** |  | ES | PPI |

| 23/12/2022 | 0800/0900 | *** | | ES | GDP (f) |

| 23/12/2022 | 0900/1000 | ** |  | IT | ISTAT Business Confidence |

| 23/12/2022 | 0900/1000 | ** | | IT | ISTAT Consumer Confidence |

| 23/12/2022 | 1330/0830 | *** |  | CA | Gross Domestic Product by Industry |

| 23/12/2022 | 1330/0830 | ** |  | US | durable goods new orders |

| 23/12/2022 | 1330/0830 | ** | | US | Personal Income and Consumption |

| 23/12/2022 | 1400/1500 | ** |  | BE | BNB Business Sentiment |

| 23/12/2022 | 1500/1000 | *** | | US | New Home Sales |

| 23/12/2022 | 1500/1000 | *** | | US | Final Michigan Sentiment Index |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.