Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

KRW

Spot USD/KRW has remained fairly elevated, last at 1436. Dips sub 1430 have been supported in recent sessions, while moves above 1440/45 could draw selling interest. The equity impulse is firmer, following firm tech gains overnight (+2.44% for the session) and above 2208 in index terms. A stronger USD against the majors, coupled with North Korean tensions, are offsetting to a degree.

- The PMI for September eased further to 47.3, from 47.6. This likely hasn't helped sentiment either. The detail was generally softer (output down to 43.1, from 44.6), although new orders rose from August.

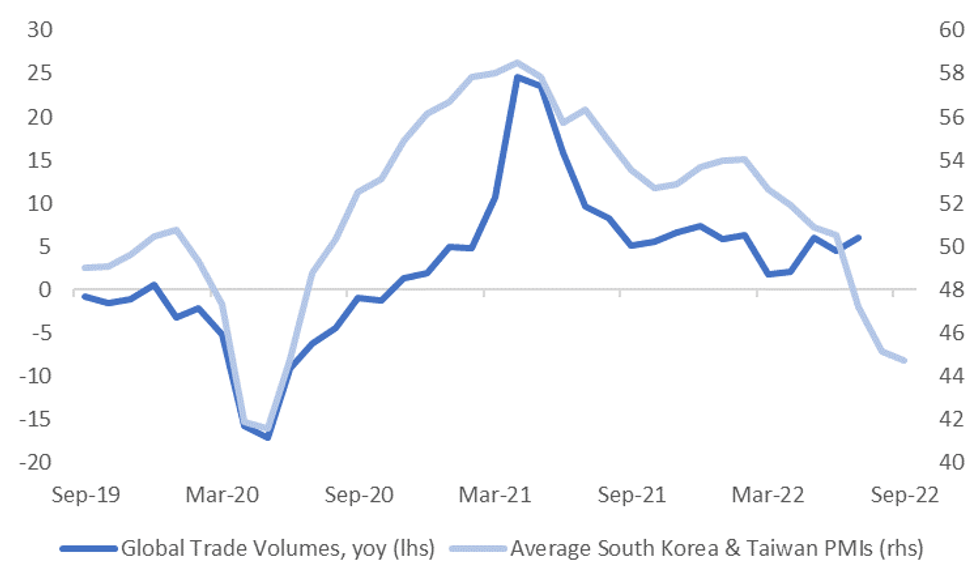

- The chart below plots the average PMI readings for South Korea and Taiwan (which printed yesterday at 42.2) against global trade volumes. The trade metric has been resilient, although note this print is only up to date for July.

- Elsewhere, South Korea is considering raising sanctions on North Korea following this morning's missile test.

- The Finance Minister stated that lowering inflation is the top policy priority. The upcoming BoK decision is next Wednesday (the 12th of October).

- The authorities are also looking at incentives for local residents to repatriate funds back into the won (see this link for more details).

Fig 1: South Korea & Taiwan PMIs Versus Global Trade Volumes

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok