Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

SOUTH AFRICA

MNI (London)

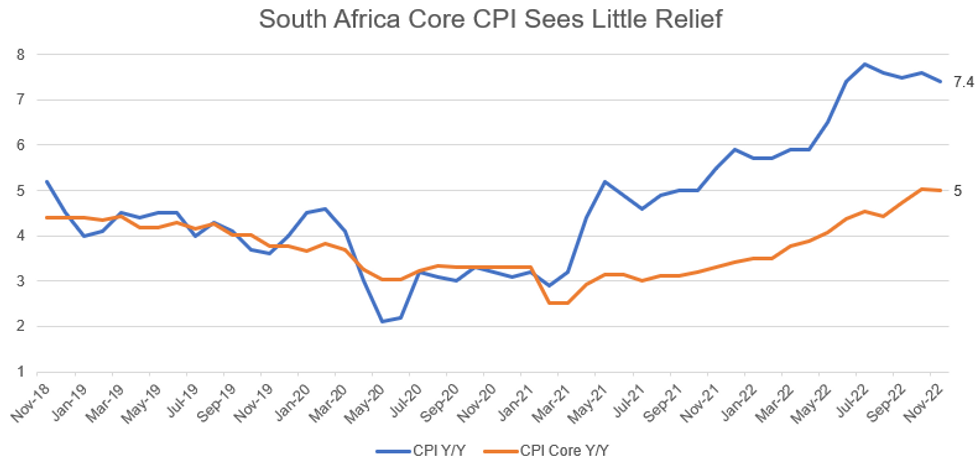

SOUTH AFRICA NOV CPI +0.3% M/M (FCST +0.3%); OCT +0.4% M/M

SOUTH AFRICA NOV CPI +7.4% Y/Y (FCST +7.5%); OCT +7.6% Y/Y

SOUTH AFRICA NOV CORE CPI +5.0% Y/Y (FCST +5.1%); OCT +5.0% Y/Y

- South African CPI moderated by 0.2pp to +7.4% y/y in November, one-tenth lower than expectations. Prices slowed marginally to +0.3% m/m (vs +0.4% in Oct).

- Food inflation accelerated for the seventh consecutive month, up 0.5pp at +12.5% y/y on the back of continued bread/cereal price growth. Hotel and restaurant prices also accelerated, to +7.9% y/y.

- Whilst transport inflation eased for the fourth month, slowing by 1.8pp to +15.3% y/y on the back of falling fuel costs.

- The next SARB interest rate decision is due at the end of January. As such, today's CPI print will likely be largely overshadowed by December data, yet November's core CPI holding steady implies the tightening cycle is not yet over.

- The November 75bp hike was likely the largest of this magnitude, leaving the Bank likely to downshift to 25-50bp in January.

Source: MNI / Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok