Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US

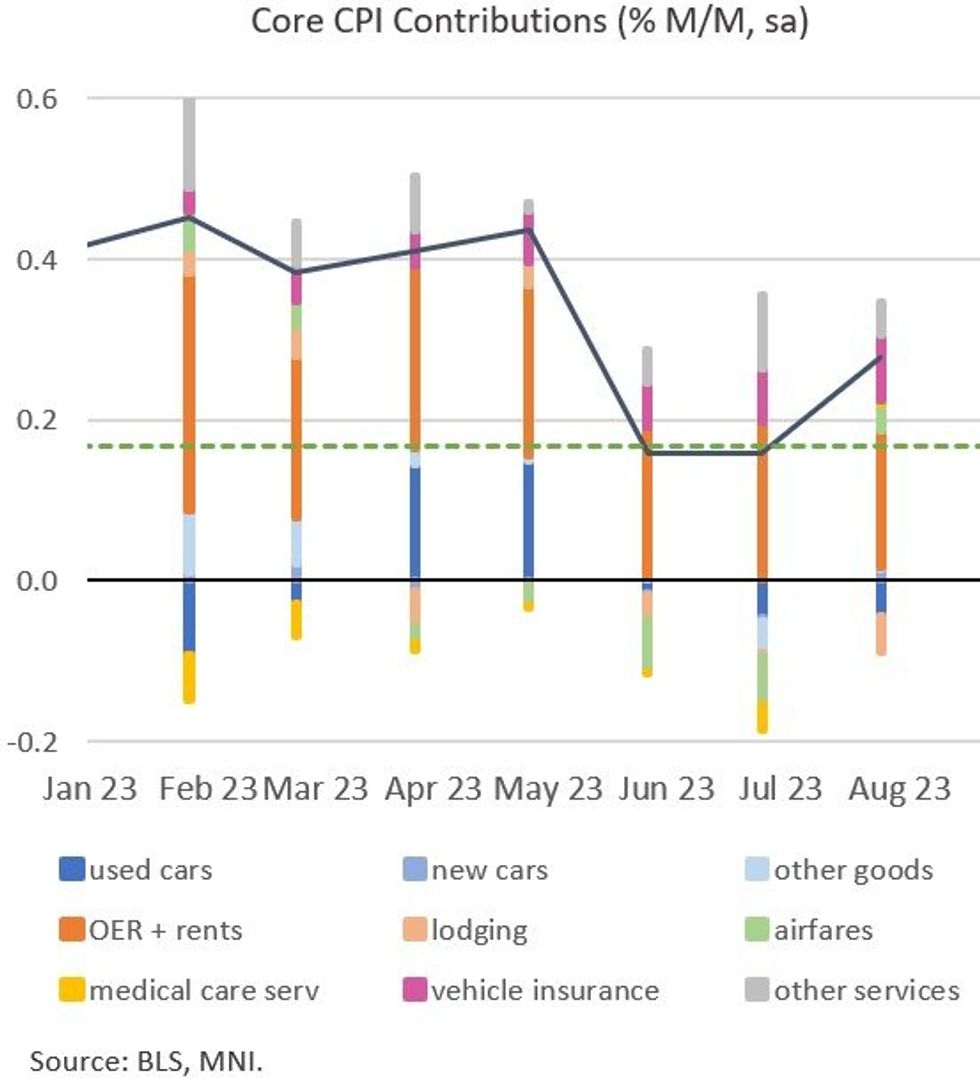

Ex-food and energy (core) CPI is expected to print 0.3% M/M in September for the 2nd month in a row in today's release (0830ET/1330UK). Headline CPI is also expected to print 0.3% M/M, a deceleration from the energy-led jump up to 0.6% in August. (Our full CPI preview is here.)

- In the event of an out-of consensus reading on core, we'll be watching for a few things in particular:

- CORE GOODS: Expected to come in slightly deflationary territory M/M (-0.2%), led by a sharp decline in used car prices (median/mean -1.5%). However used cars are arguably the biggest wild card in the overall print as there's a wide range of analyst expectations - from -3.6% to +1.3% - which has the ability to swing the overall core number significantly.

- CORE SERVICES: Expected to remain steady-to-higher vs August's 0.39% (0.4% median/mean), with OER picking up slightly from 0.38% and rents decelerating a bit from 0.48%. Major swings are seen in lodging (from -3.0% in Aug to +1-to-2%) offset by a deceleration in airfares (from 4.9% in Aug).

- Note that if airfares are particularly strong, they are likely to be discounted in an upside core surprise scenario. We already have the PPI airline passenger services reading (which is used in the Fed's PCE measure) which came in at around -2% for the 2nd month in a row.

- "Supercore" (core services ex-OER/rents) services inflation is seen between 0.3-0.5% M/M, after August's 0.37%.

- HEADLINE: Energy inflation is set to decelerate significantly from Aug's 14-month high 5.6% M/M (expectations are around 1-1.5%), driving the slowdown in headline CPI M/M. Food inflation is seen relatively steady by comparison, at 0.2-0.3% M/M, vs 0.2% in both Jul and Aug.

(Dotted line represents pace consistent with 2% annualized)

(Dotted line represents pace consistent with 2% annualized)

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok