Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

BONDS

NZGBs weakened through Thursday's session, closing at cheaps, as the market comes to terms with the hawkish messaging from yesterday’s RBNZ policy decision and the bank’s subsequent communique. The overhang of potential supply resulting from the Government’s post-cyclone response also appears to have weighed on NZGBs with bonds underperforming swaps on the day.

- NZGBs close 13-14bp weaker across the curve versus a +5-9bp move in swaps.

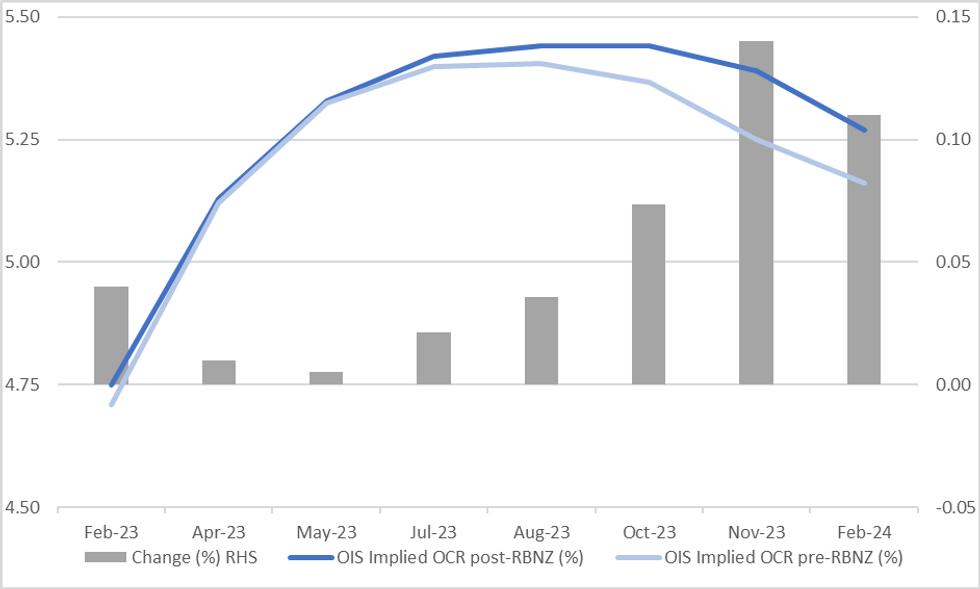

- RBNZ-dated OIS's reaction to yesterday’s policy decision has centered on pricing for the late-23 meetings. With the RBNZ deciding to keep its peak OCR projection at 5.50% (albeit reached slightly later), highlighting the inflationary impact of Cyclone Gabrielle, alongside the chance of higher for longer rates (per comments from Governor Orr in a BBG interview). The market has lifted terminal OCR pricing to 5.45%, while scaling back easing expectations for later in the year. Pricing for the October and November meetings firmed 7bp and 13bp, respectively versus pre-RBNZ levels with the latter now only pricing in ~5bp of easing from 23bp a week ago and ~40bp at the start of February.

- With little on the local calendar until next week’s Q4 Retail Sales release, the market will have to find its direction from abroad, RBNZ communications and/or government announcements on its natural disaster recovery strategies.

Fig. 1: Pre- Vs. Post- RBNZ Meeting RBNZ-Dated OIS (%)

Source: MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok