Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

JPY

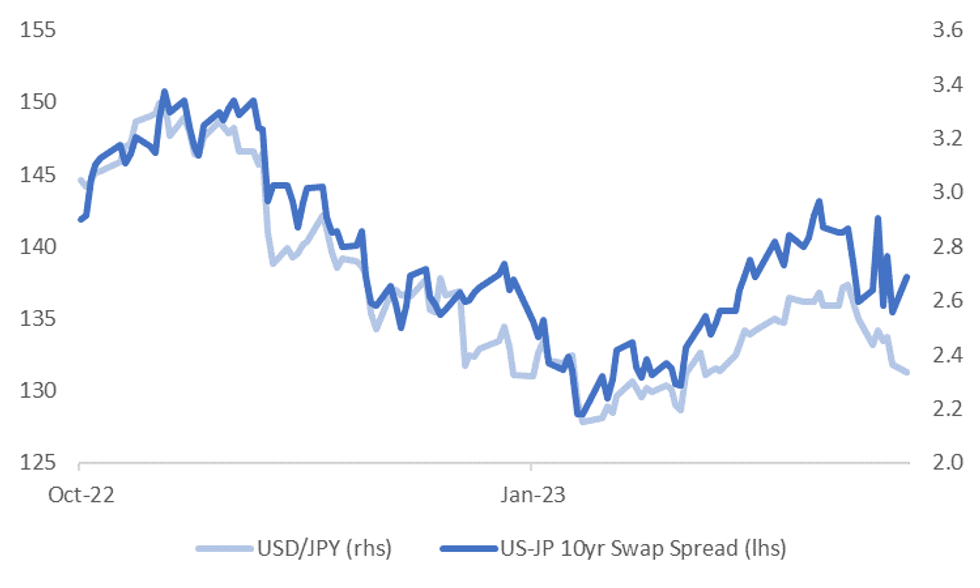

A modest wedge has emerged between USD/JPY and the US-JP 10yr swap differential, see the chart below. The yen looks too firm relative to the recent moves in spreads. As we noted in the earlier yen bullet, the currency outperformed the rebound in US yields through Monday's NY session.

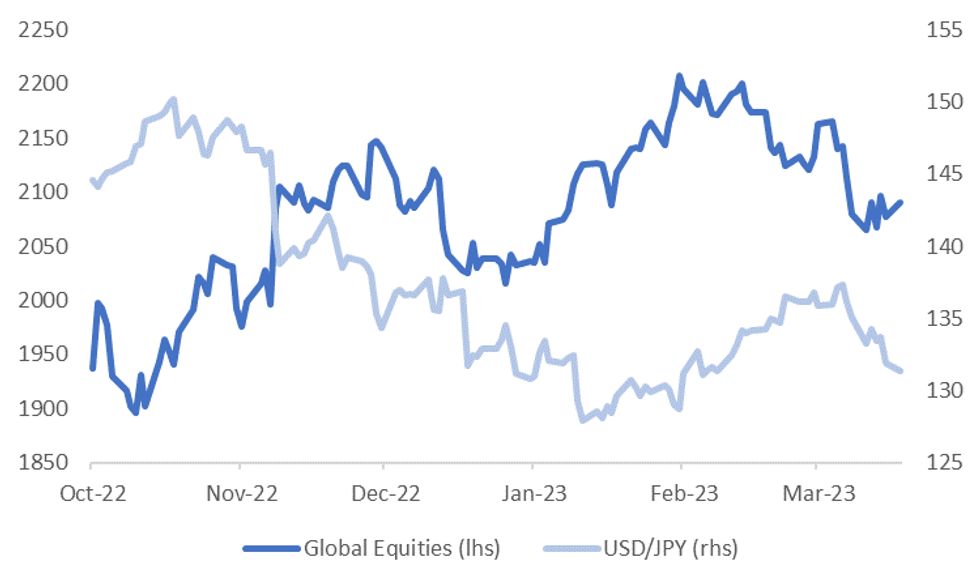

- One factor that has helped drive the wedge has been the recent correction lower in global equities, see the second chart below.

- USD/JPY is no doubt seen as a good downside hedge in the event of a deeper correction in equities, particularly in the event of a global recession scenario. The second chart below plots USD/JPY versus global equities.

- Correlations have fallen with relative swap spreads, back to 70%, versus around 97% in early March on a rolling monthly basis (in levels terms). The correlation with global equities has rebounded over the same time period, back to +60%, after being negative earlier in the month.

- Again though, USD/JPY looks a little low versus the recent stability in global equities. USD/JPY downside could still be viewed as an attractive hedge given the current global climate. The currency tends to perform well during global recessionary periods and at current levels is still viewed as cheap on some metrics (REER very low relative to long term averages).

- The other focus point for the market will be risks of a BoJ policy shift (in some form) during 2023.

- The USD/JPY risk reversal remains close to recent lows, last under -2.10, which is still indicative of downside USD/JPY demand. Note today is Japan holiday, which will be impacting liquidity to a degree.

Fig 1: USD/JPY Versus US-JP 10yr Swap Spread

Source: MNI - Market News/Bloomberg

Fig 2: USD/JPY Versus Global Equities

Source: MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok