Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

AUD

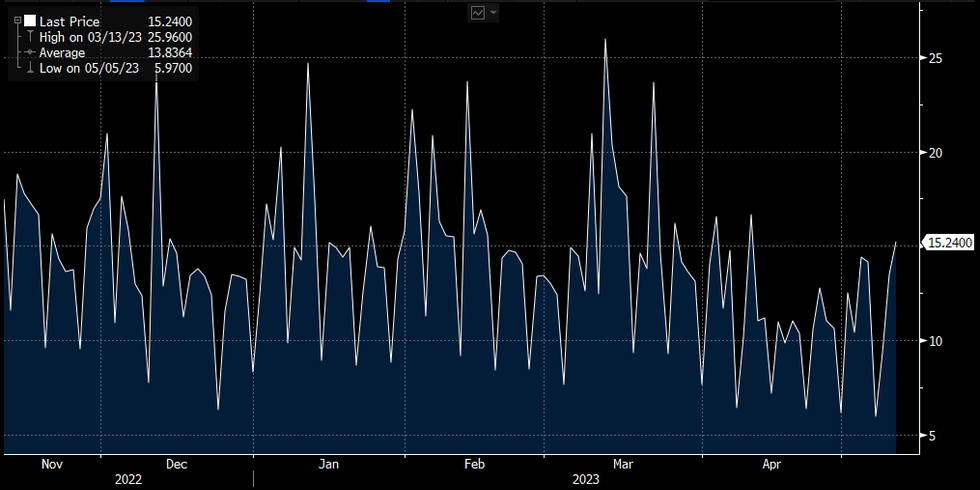

AUD/USD overnight implied volatility sits at 15.24% as option markets price in a $0.6702-$0.6832 range in the aftermath of today's US CPI print.

- Overnight implied volatility sits well below levels seen in the aftermath of the SVB crisis (~25%) in March. We also sit below levels seen around April's RBA meeting, when the bank paused its hiking cycle, (~17%) and within the 2023 range.

- Overnight risk reversals are skewed to the downside, however we sit well above levels seen pre-SVB crisis and within the yearly range.

- Bulls look to target $0.6806 high from Apr 14 and key resistance. Support comes in at $0.6711 the 50-Day EMA.

- The MNI preview of the US CPI print is here.

Fig 1: AUD/USD Overnight Implied Volatility

Source: MNI/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok