Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

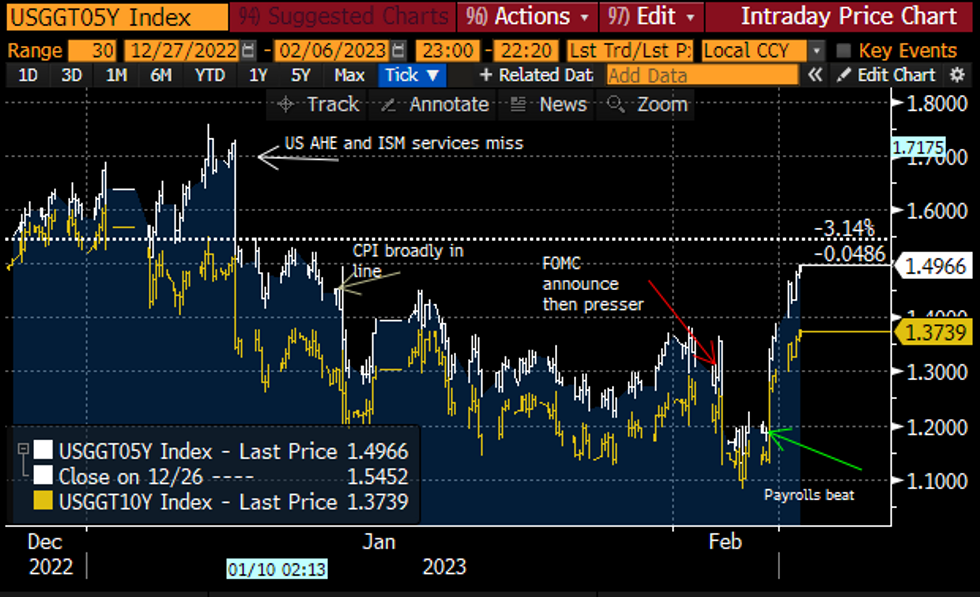

US TSYS

- Today’s large cheapening in Treasuries following Friday’s beats for payrolls and ISM services comes with real yields climbing further (5YY +12bps, 10YY +8bps).

- In doing so, 10Y real yields have increased from a low of 1.09% in the gap between the FOMC presser’s dovish reaction and Friday’s payrolls, to 1.37% currently.

- However, it’s still only back to level immediately after last month’s surprise weakness in AHE (about half of which was subsequently revised away in Friday’s January print) and ISM services (which has been fully unwound after the sharpest monthly increase since the pandemic). Prior to these misses, 10Y real yields were ~1.5%.

US 5Y real yields (white) and 10Y real yields (yellow)Source: Bloomberg

US 5Y real yields (white) and 10Y real yields (yellow)Source: Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok