Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US DATA

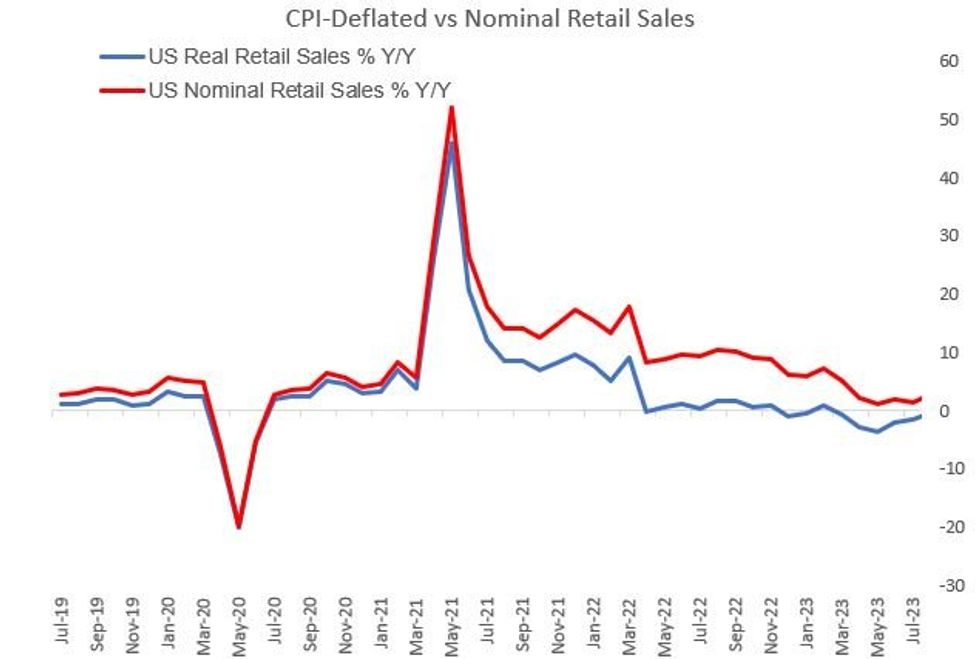

October's advance retail sales were stronger than expected, particularly when taking into account upward revisions to September's data.

- Overall retail sales declined -0.1% M/M (vs -0.3% expected, +0.9% prior revised from +0.7%), with ex-auto +0.1% (vs -0.2% expected, +0.8% prior revised from 0.6%) and ex-auto/gas +0.1% (vs +0.2% expected, +0.8% prior revised from 0.6%). And the key control group, an input into GDP, was in line at +0.2% M/M but saw prior revised up to 0.7% from 0.6%.

- As expected, motor vehicle retailers (-1.0% M/M after +1.1%) and gasoline stations (-0.3% M/M after +1.0%) dragged on overall sales, though the gas sales decline may have been a little less than expected given the sharp drop in prices.

- Elsewhere the story was mixed. Multiple categories saw improvement vs September: electronics (+0.6% vs +0.4% prior), food/beverage (+0.6% after +0.2%), health/personal stores (+1.1% after +0.5%), and clothing (flat after -0.8%)

- However several saw flat/lower growth. Building materials saw a second consecutive -0.3% M/M reading, with sporting goods contracting -0.8% after +0.1%, furniture -2.0% after -0.6%, general merchandise -0.2% after +0.4%, miscellaneous retailers -1.7% after +4.8%, nonstore retailers +0.2% after +1.4%, and food services +0.3% from +1.6%.

- In real terms, the 0.0% CPI figure for October implies a modestly negative "real" figure. On a Y/Y basis, CPI-adjusted retail sales were slightly negative (-0.7%) for the 11th month in 12, and remains below late-2021 levels.

- While the underlying details were very mixed, the overall pullback was less than expected, and with the control group reading in-line, this report shows a moderation from a very strong Q3 but hardly a collapse of consumption as we head into the holiday shopping season.

Source: BLS, Census Bureau, BBG, MNI

Source: BLS, Census Bureau, BBG, MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok