Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EUROZONE DATA

MNI (London)

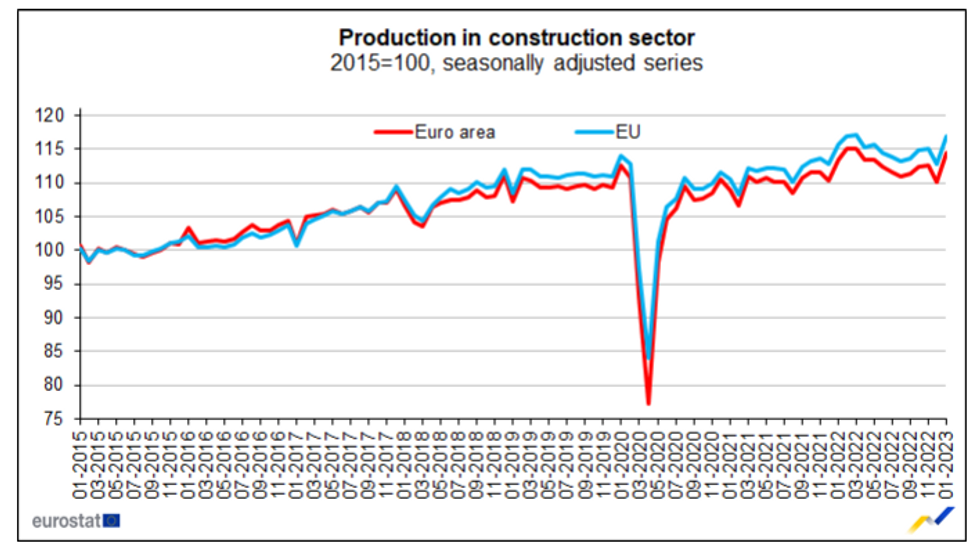

EUROZONE JAN CONSTRUCTION OUTPUT +3.9% M/M; DEC -2.3%r M/M

EUROZONE JAN CONSTRUCTION OUTPUT +0.9% Y/Y; DEC --0.6%r Y/Y

- January construction output rebounded in the eurozone by +3.9% m/m and +0.9% y/y following a contractionary end to 2023. This was largely due to the +12.6% m/m boost from Germán construction (largely a rebound from the December fall).

- Looking forward, February construction PMI data improved to the softest contraction since May '22.

- Further easing of supply shortages and decreasing building material costs are underpinning improvements in the sector. Yet the high interest rate environment means that demand appetite will likely remain lacklustre for now.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok