Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US

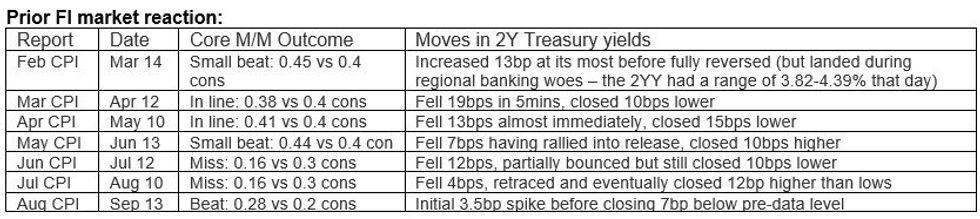

Overall, today's CPI reading is shaping up to be largely about the details. There's room for a decently large surprise to the 0.26% (average) M/M consensus in either direction on the core (used cars for goods, airfares for services) that spurs a knee-jerk reaction, but one will have to pick it apart to get whatever signal lies within. We are reminded of last month's reading where the initial upside surprise was ultimately faded as the upside came from increases in categories that weren't seen being repeated in the Fed's preferred PCE metric. See table below.

- While thecore CPI reading is unlikely to show much more progress if at all toward a 2.0% run rate in September, if the individual categories are in line then it will not dissuade the FOMC from believing that it is on track to meet its inflation objective over the medium-term.

- Developments since the September FOMC – including geopolitical turmoil and rising long-end yields reflecting soaring Tsy issuance and “higher-for-longer” rate pricing - have pared expectations of further hikes in this cycle, with just 7bp of further tightening priced. Even a much stronger-than-expected September employment report didn’t have a lasting effect on perceived tightening.

- Yesterday's stronger-than-expected PPI reading probably nudged up the bar to what represents an upside surprise in the CPI reading. Even so, in the event of an upside core CPI shock, the implications for November Fed pricing are likely to be limited, with December perhaps nudged up a couple of basis points (in conjunction with the strong payrolls report calling the Fed’s expectations into question).

- A significant miss would probably all but price out further tightening and could even bring forward easing expectations depending on whether it's largely confirmed by the details of the report.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok