Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

INR

Spot USD/INR is drifting higher in early trade today (after onshore markets were shut yesterday). We remain well within recent ranges at 81.60/65, but the rupee is not enjoying the benefits of a weaker USD seen elsewhere in the region. Coming up soon is the services (last 57.2) and composite (58.2) PMI readings for September.

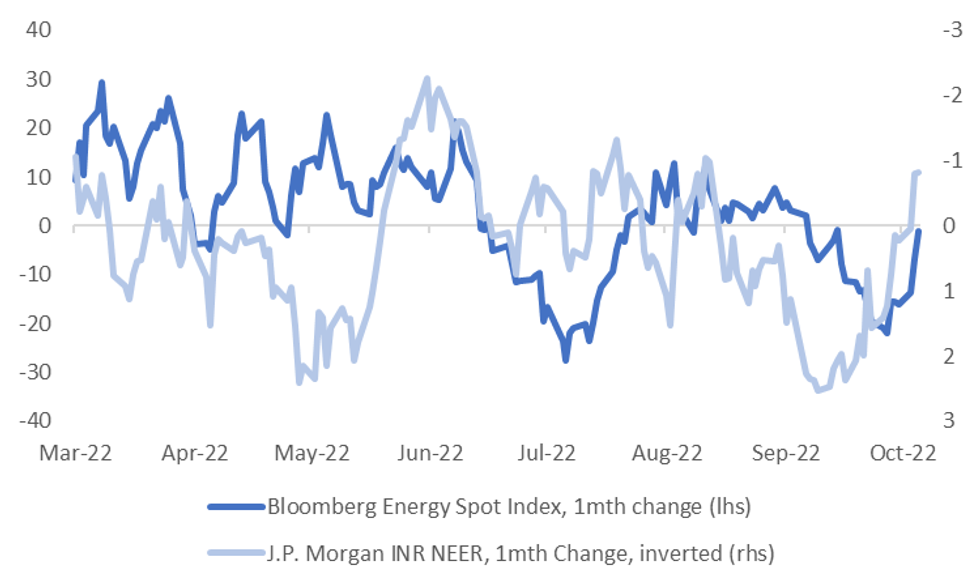

- The recovery in crude prices is likely weighing on INR sentiment, at least on a relative value basis. The chart below plots the 1 month change in the J.P. Morgan INR NEER, which is inverted on the chart, against the 1 month change in the Bloomberg spot energy commodity price index.

- INR is the only EM Asia FX currency not to gain against the USD so far in October. In September it was the best performer, albeit still dropping 2.2% against the USD.

- Elsewhere, onshore yields are up, the 10yr pushing back to 7.46%, +10bps, as potential index inclusion has been put off to 2023. Local equities are higher though, +0.60% at this stage.

Fig 1: Energy Commodity Prices & J.P. Morgan NEER

Source: J.P. Morgan/MNI - Market News/Bloomberg

Source: J.P. Morgan/MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok