Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

SWEDEN

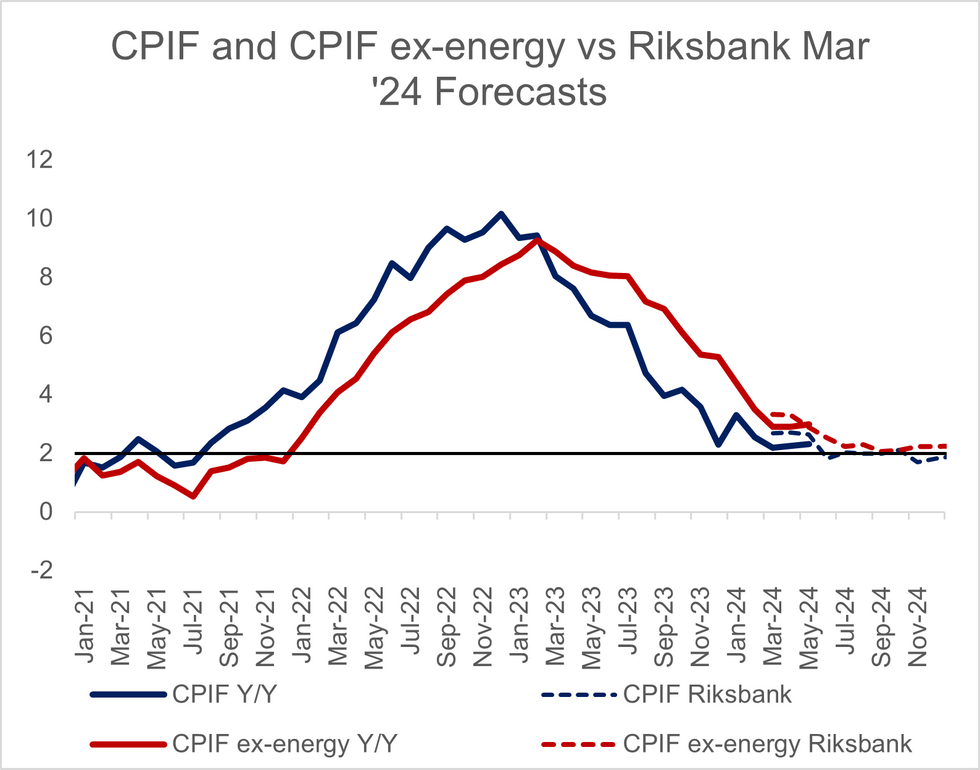

Swedish May inflation was higher-than-expected, with CPIF ex-energy at 3.0% Y/Y (vs 2.6% cons, 2.9% prior). This actually means that CPIF ex-energy prints 0.1pp above the Riksbank’s March MPR forecast of 2.9%. In the previous two months, the forecast error was -0.4pp.

- The probability of a June rate cut was already very small, but this data all but confirms an on-hold decision at the May 27 meeting. Main interest now is whether the Riksbank’s guidance for 2 cuts in H2 2024 will change – we don’t think there is enough evidence for that just yet.

- SEK has strengthened a touch versus the EUR and NOK, but remains comfortably within yesterday’s ranges on both crosses.

- The “one-off leisure effects” related to the Eurovision song contest and Taylor Swift concerts in Sweden appear to have had a larger impact on services inflation than expected. These effects should reverse next month.

- In May, restaurant and hotel prices rose 2.6% M/M (versus an average May increase of 1.1% M/M since 2010). On an annual basis, this component still moderated to 4.9% Y/Y (vs 5.6% prior).

- International flights also rose 17.2% M/M in May, versus an average May decrease of -7.1% M/M since 2010.

- Food prices rose 1.5% Y/Y (vs 0.7% prior) and 0.4% M/M, which also pushed underlying inflation higher.

- Headline inflation was 2.3% Y/Y (vs 2.1% cons, 2.3% prior and 2.6% in the Riksbank March MPR). As expected, electricity base effects dragged headline lower, at -10.9% Y/Y (vs -8.7% prior) and -13.3% M/M.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok