Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

GERMAN DATA

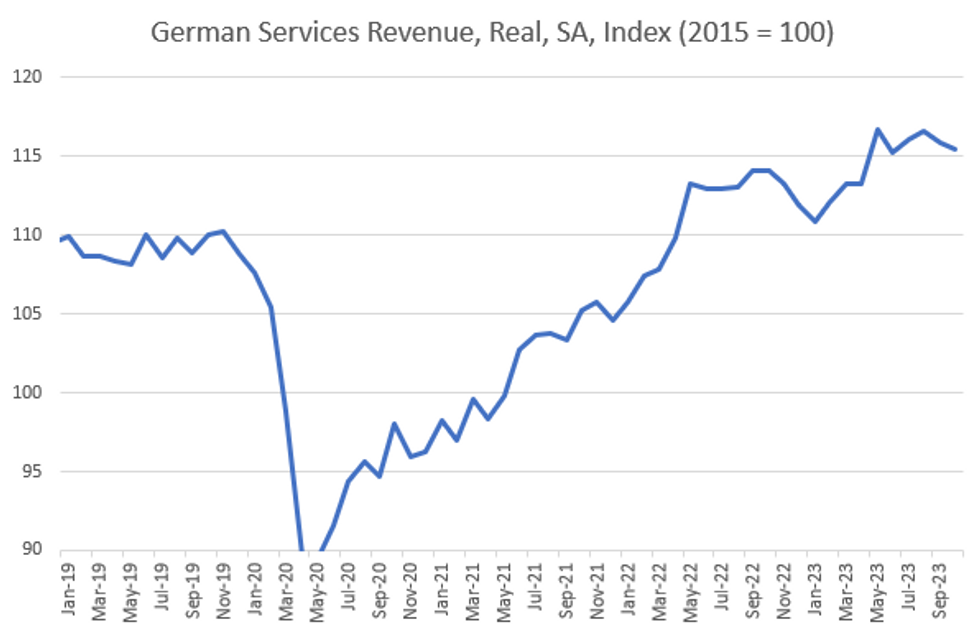

Turnover in German services sectors (excl. finance and insurance) weakened in October, coming in at -0.3% M/M (vs -0.6% prior) and +1.2% Y/Y (vs +1.6% prior) in data released Friday morning.

- Those figures, which are reported by Destatis in real (inflation adjusted) and seasonally adjusted terms, represented the second monthly decline in a row. The 3M/3M measure came in flat at 0.0% (vs +1.0% prior) after 6 months of positive prints.

- The strongest gains on a monthly basis could be seen in freelance, scientific and technical services at +1.2% M/M (-2.1% prior), and real estate and housing services at +1.0% M/M (vs +0.5% prior), the highest value since three months.

- Negative impulses could be seen in the other economic services sector (e.g. rental of movable property and placement of labour) at -2.4% M/M (vs +1.0% prior), the lowest value since 4 months. Revenues in the transport and warehousing sector also drove the total lower, falling at -0.5% M/M (vs -1.1% prior).

- Services have been relatively resilient compared to the manufacturing sector in Germany, but some weakness is starting to emerge.

- The German Services PMI ticked up slightly after October (48.2 Oct, 49.6 Nov, 49.3 Dec), but the December print noted a muted growth outlook for the next 12 months and participants seeing activity being dragged down by “tightened financial conditions and weakness in the broader economy”.

- The IFO survey's services sector expectations balances have been in contractionary territory since March 2022, but on a considerably less severe level than their manufacturing equivalents. This seems to be the general theme.

Source: Destatis, MNI

Source: Destatis, MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok