Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

ITALY DATA

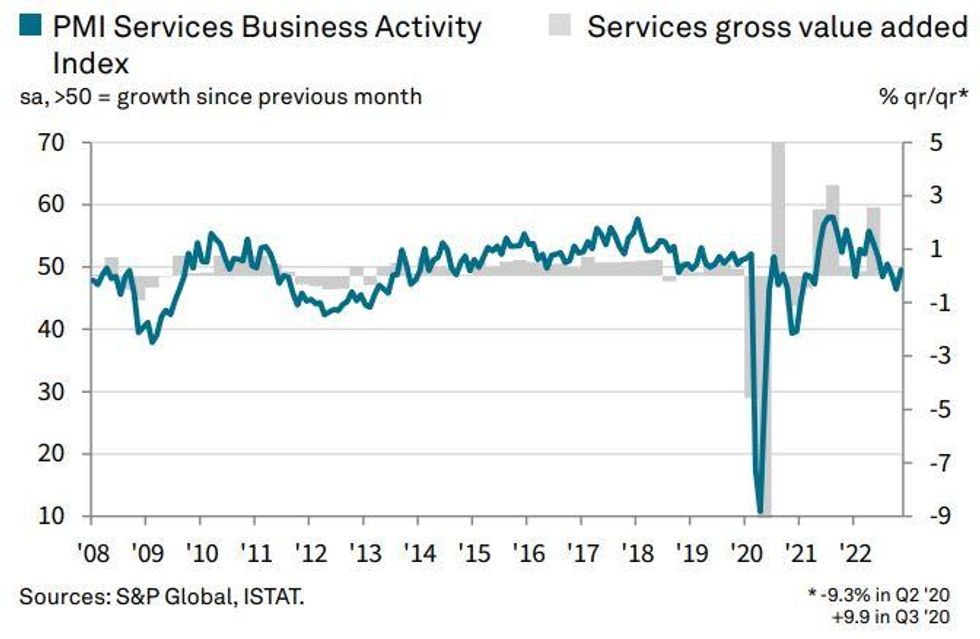

A solid Italy PMI report for November, with a Services reading of 49.5 (47.5 expected, 46.4 prior) and Composite of 48.9 (46.5 expected, 45.8 prior).

- The negative news first: Services activity and new orders continued to fall, with weaker demand attributed to the Russia-Ukraine war and price pressures. Foreign demand was especially weak. And input inflation rose further for Services firm. Input costs have risen in each month since June 2020. This was passed through, marking the 14th consecutive month in prices charged to customers.

- But there were significant constructive developments as well, with Services business activity and new orders seing slower rates of contraction, alongside accelerating jobs growth and the highest business confidence since June (up from October's 23-month low).

- One theme here is spare capacity: outstanding business fell as there was a combination of reduced demand for new work and higher employment (Services saw the fastest rate of job gains since July).

- Overall, although Italian services sector activity is stagnant at best, it adds to other pieces of recent evidence (eg other eurozone PMIs, German IFO) to suggest that the Eurozone downturn may not be quite as bad as feared.

Source: S&P Global

Source: S&P Global

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok