Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

GLOBAL

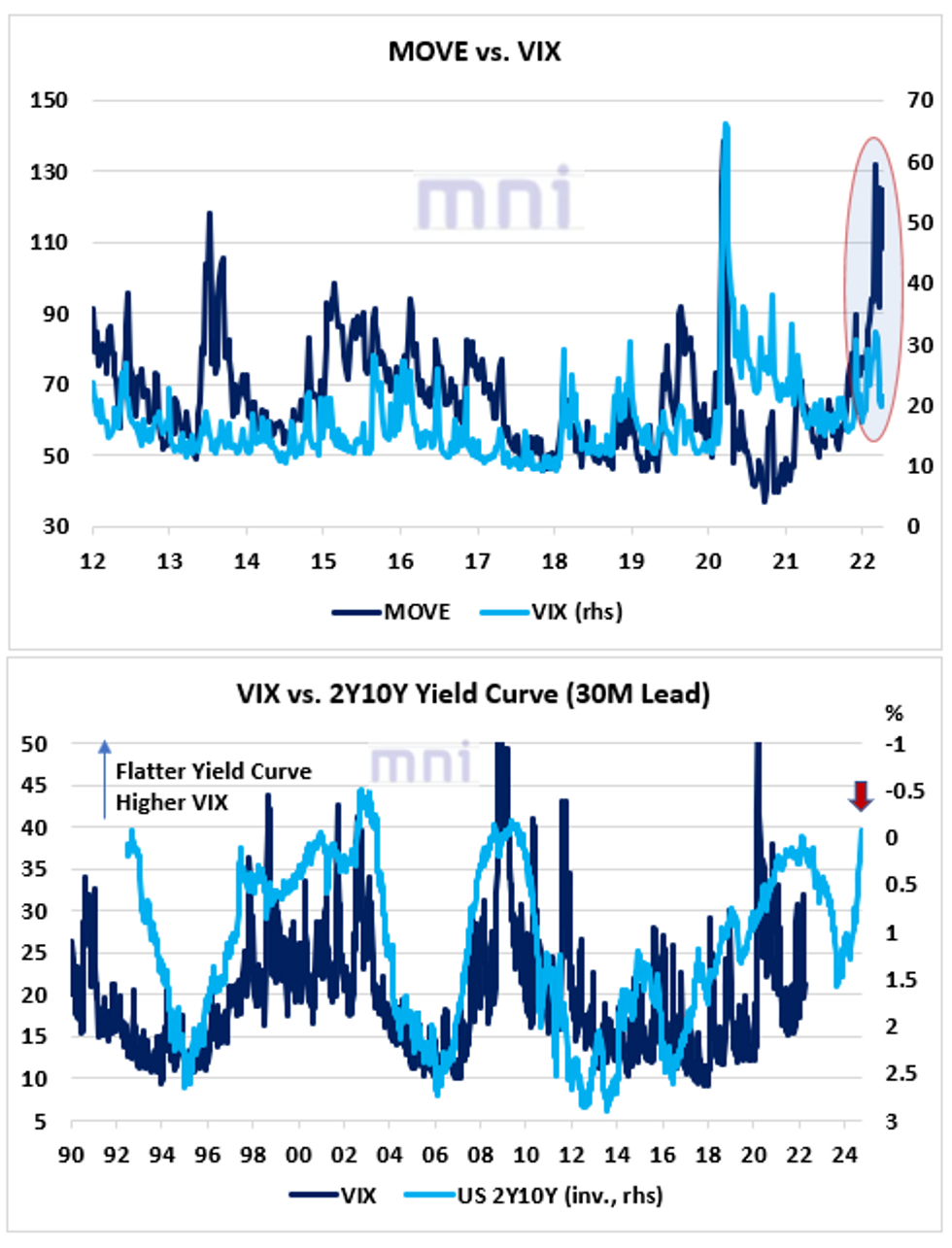

- Divergence has been widening sharply in recent weeks between the MOVE index, which measures bond market volatility, and the VIX as rising inflationary pressures have led to a sharp retracement in LT bond yields (top chart).

- While investors tend to ‘rush’ to buy the dip when equities correct, the dynamics in the bond market have been slightly different, particularly when inflation is rising.

- US 10Y yield surged to a local high of 2.8320% on Tuesday (Dec 2018 highs) before starting to consolidating lower in the past two days.

- However, price volatility in the equity market is expected to remain elevated in 2022 as equities perform poorly in stagflationary regimes (high inflation, falling economic activity).

- In addition, the bottom chart shows that the sharp flattening of the yield curve has generally preceded high-volatility regimes in the past 30 years.

- The bottom chart shows that the 2Y10Y yield curve has historically strongly led the VIX by 30 months.

Source: Bloomberg/MNI.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok