Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

STIR

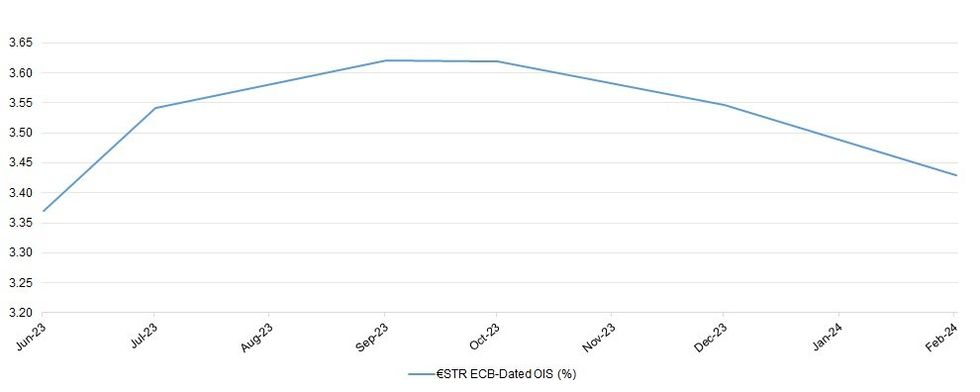

ECB-dated OIS pricing is incrementally higher today, although participants are still reluctant to fully price in a 2 further 25bp hikes from current levels. ~47.5bp of cumulative tightening is currently priced into the ECB-dated OIS strip, with ~19bp of cuts from current terminal rate pricing showing by the end of the ECB’s February meeting.

- The previously alluded to Fedspeak and uptick in equities has seemingly been the driver of pricing today.

- Elsewhere, Bundesbank chief Nagel generally reiterated comments he made yesterday, maintaining debate re: the need for tightening beyond the summer break.

- Late yesterday saw ECB Vice President de Guindos suggest that there “could” be further rate hikes (much less forceful than the general ECB tone at first glance), although he did highlight a data- and credit-dependent stance along with some worry re: service inflation, as well as a high level of consensus within the ECB re: the previous monetary policy decision, which countered the initial tone.

| ECB Meeting | €STR ECB-Dated OIS (%) | Difference Vs. Current Effective €STR Rate (bp) |

| Jun-23 | 3.370 | +22.5 |

| Jul-23 | 3.542 | +39.7 |

| Sep-23 | 3.620 | +47.5 |

| Oct-23 | 3.619 | +47.4 |

| Dec-23 | 3.546 | +40.1 |

| Feb-24 | 3.430 | +28.5 |

source: MNI - Market News/Bloomberg

source: MNI - Market News/Bloomberg

MNI London Bureau | +44 0203-865-3809 | anthony.barton@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok