Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

CONSUMER STAPLES

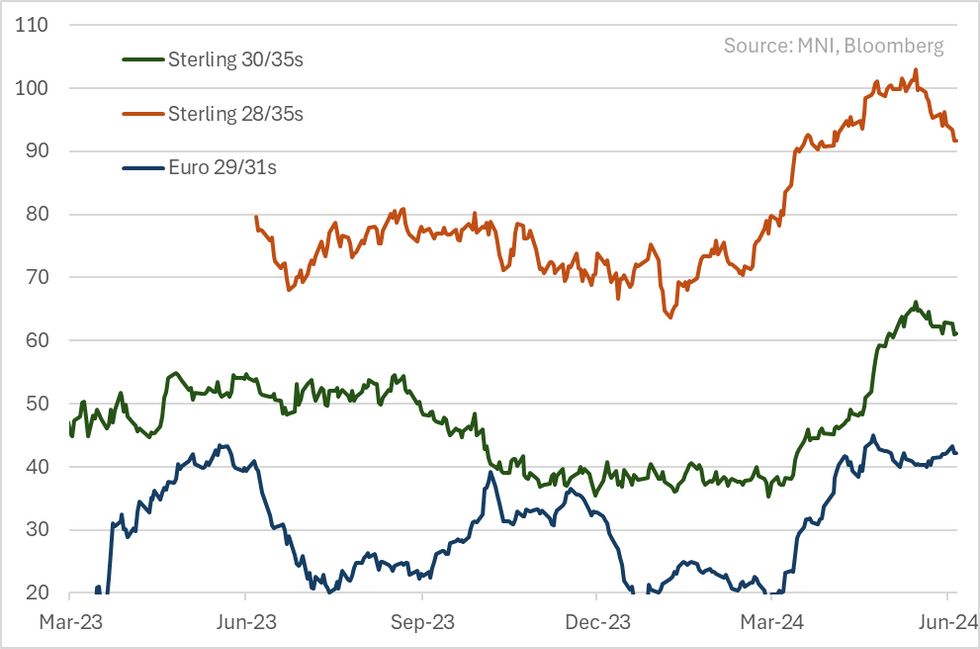

- We had a cheap view in primary on the the £10Y - not on the 7bp NIC it came with but on the steep secondary (mirrors BBB tobacco). Curve has flattened but its been driven by weak short-end and left our new 34s +9 wider at Z+161.

- We also had a cheap view on the €31s on similar reasoning - again shorter 29s have moved out but 31s moving with it.

- We don't see the Tesco bank sale triggering an event of default & have heard that may have drove low cash px shorter lines in - unclear if that's driven the reversal wider in €29s & £28/30s.

- We keep both views unch further out. Implied roll-down is attractive to us as is excess carry among sector comps - in €'s the 31s gives +40bps over Ahold (Baa1/BBB+) & +20 over Carrefour (Baa1/BBB).

- Tesco should give a Q1 trading update (3m ending May) soon. FY guidance was for adj. operating profit of £2.8b (c£2.95b) & retail FCF of £1.4-1.8b (c£1.6b). Latter excludes the £1b in bank sale proceeds on close later this year -it will be entirely directed to equity holders through buybacks.

- Leverage at bottom of target, unclear if the ~€400m £ deal last month was to refi the €473m (outstanding) July line rolling off soon...we wouldn't rule out local supply.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok