Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

SWITZERLAND DATA

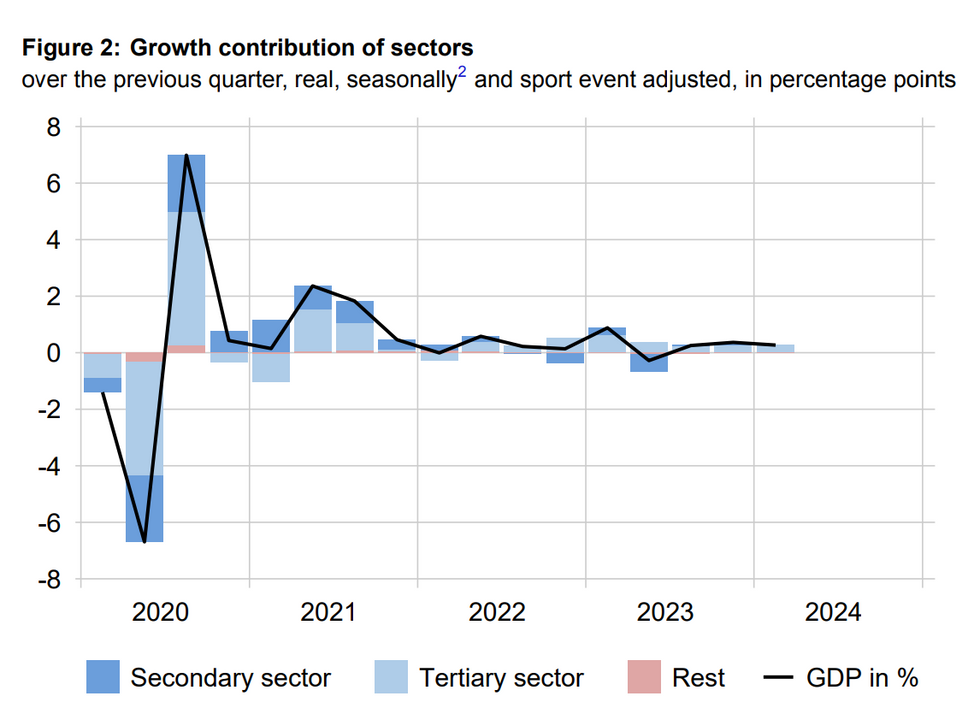

Swiss Q1 real GDP came in higher than expected on the sequential reading, at 0.5% Q/Q (vs 0.3% cons and prior) on a non sports event-adjusted basis, but lower than expected on a yearly comparison (+0.6% Y/Y vs +0.7% cons; 0.5% prior, revised from 0.6%). The Bloomberg median consensus was not consistent amid noticably more estimates being submitted for the Q/Q reading.

- When adjusting for sports events, growth was not as strong at +0.3% Q/Q vs 0.3% prior). The main takeaway here being that the report suggests that the moderate pace of growth in the Swiss economy continued in Q1.

- On a production split, "trade" and "hospitality" saw the most positive developments, both at +1.3% Q/Q (vs -0.5% and +2.2% prior, respectively).

- "Manufacturing" and "business services" meanwhile printed weaker than in Q4, at -0.2% Q/Q and -0.3%, respectively (+0.1% and +0.2% priors).

- On an expenditure basis, goods exports were lower on a sequential comparison (-3.3% Q/Q vs +3.8% prior). Elsewhere, developments were solid but not overly strong, with private consumption, government consumption, and equipment and software investment all contributing positively (+0.4% Q/Q, +0.2%, and +0.8%).

- Contrary to Switzerland's neighbor Germany, construction investment declined in Q1, however, at -0.2% Q/Q (vs -0.1% prior).

- Swiss real GDP growth is expected to pick up during remainder of 2024, with MNI's collation of sellside analysts standing at +1.1% Y/Y, +1.3%, and +1.4% for Q2-Q4. These estimates were not materially revised during the last three months. The SNB meanwhile expects around 1% growth for 2024 overall.

MNI, Seco

MNI, Seco

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok