US DATA

- Consumers' assessment of their current financial situation compared with the previous year dipped to an index level of 79, joint-lowest since December 2022, vs 91 in May and March's 2+ year high of 104

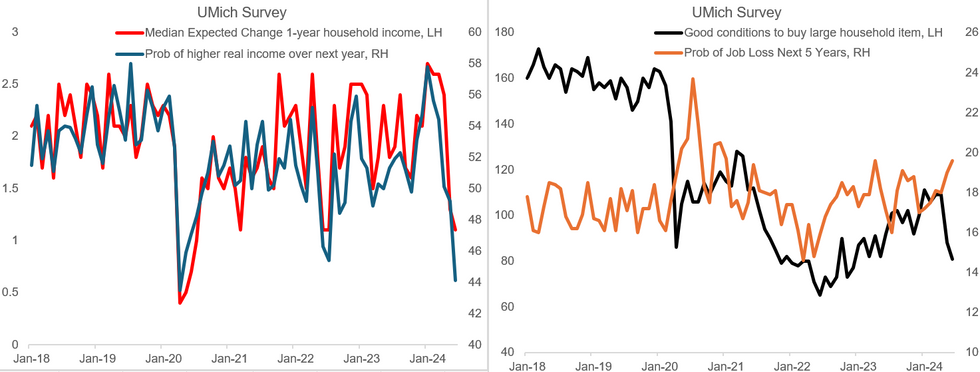

- The median expected change in household income over the coming 1-2 years dropped to 1.1%, joint-lowest since July 2020. As recently as April this was 2.4% Only 44.1% see expect higher real income over the next year, not far from the pandemic low of 43.5%.

- Job loss expectations over the next 5 years are up to 19.6%, joint-highest since January 2021.

- The "Good time to buy a major household Item" index was 81, lowest since Dec 2022.

The Michigan report acknowledges this deterioration, explaining it by a divergence across income levels.

- Higher-income consumers are not complaining as much as they have in the past about higher prices, but lower/middle-class consumers' complaints "have continued largely unabated", with middle-income consumers' views "resembl[ing] those of their lower-income counterparts, a departure from historical patterns in which their mentions are squarely in between those of higher- and lower-income consumers."

- Per UMich, overall sentiment for top one-third of income earners is up 56% since June 2022, vs 29% for the middle tercile and 11% for the bottom tercile.

Source: UMich, BBG, MNI

Source: UMich, BBG, MNI

399 words