Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

SWEDEN

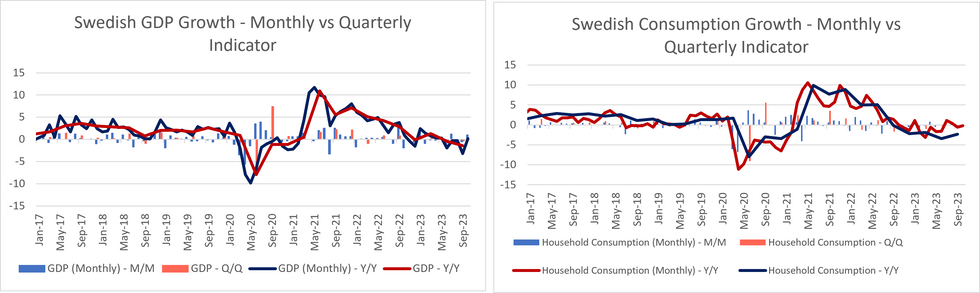

The Swedish monthly indicator grew significantly more than expected in October, printing at +1.0% M/M (vs +0.1% cons; -0.5% prior). In annual terms, the indicator also grew +0.2% Y/Y (vs a downwardly revised -3.2% prior). In its November forecast round, the Riksbank expected Q4 2023 GDP growth at -0.1% Q/Q and -1.4% Y/Y.

- We note that the monthly indicator is volatile, and October's weak print suggests the Q4 tracking is still just below zero in annual terms. Overall, this data does not change the narrative of a weak economic outlook in Sweden, and further justifies the Riksbank's decision to hold rates at its latest meeting.

- The press release notes that the uptick in GDP was largely due to strong net exports. The strengthening of the SEK in recent weeks may have contributed to an increase in the value of exports with foreign recipients not yet substituting away from Swedish goods.

- Household consumption rose +0.1% M/M (vs -0.5% prior) but fell -0.2% Y/Y (vs -0.6% prior). The consumption data still indicates weakness in the services sector, with restaurants, cafes, hotels and accommodation services falling -4.8% Y/Y. This is reflected in service sector production, which fell -2.4% Y/Y in October (vs an upwardly revised -0.2% Y/Y prior).

- The main upside driver for consumption came from transport and retail sales and service of motor vehicles, which rose +4.4% Y/Y.

- The rest of the production data also indicated a soft activity outlook, with falls in industrial production (-1.1% Y/Y, with September's figure revised down from +1.9% Y/Y to 0.0% Y/Y), construction sector production (-4.6% Y/Y) and industrial orders (-4.8% M/M vs +4.0% M/M prior).

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok