Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

CNH

USD/CNH fell below 6.7300 overnight, but we pushed back above 6.7400 and currently track around 6.7430. The currency remains an underperformer though during this recent bout of USD weakness.

- CNH/JPY is struggling to hold above its 100 day MA (19.746), with current spot at 19.755. EUR/CNH is also close to recent highs, sitting just under 6.955 presently.

- Domestic covid trends are presenting headwinds. Local case numbers are at a 3 month highs, (comfortably over 2k for daily case numbers), while Shanghai reported 7 local cases for yesterday.

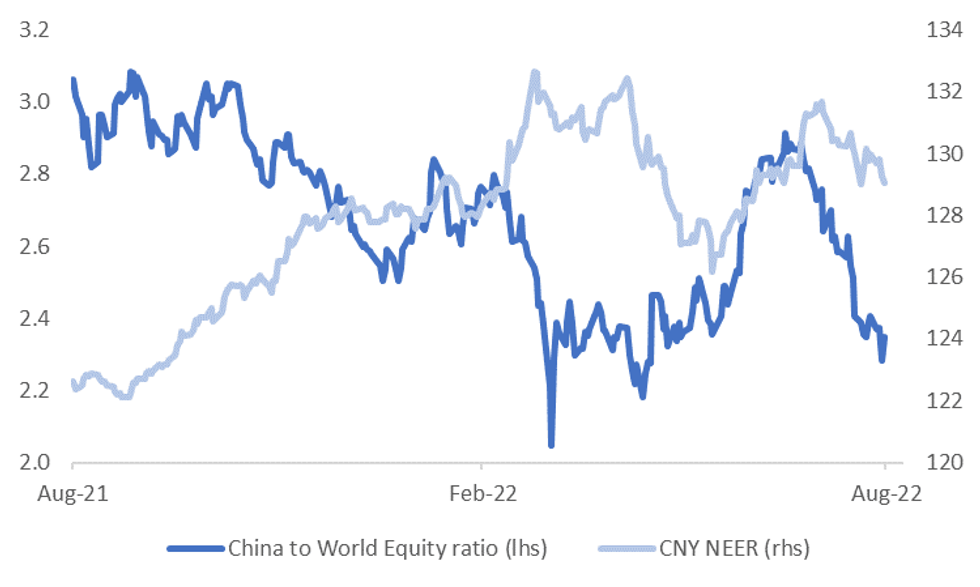

- China equities have had a better run in recent sessions, but on a relative basis, we aren't too far away from YTD lows compared to global equities, see the chart below. The other line on the chart is the CNY NEER (J.P. Morgan estimate), which is also drifting lower, in line with the trends outlined above.

- Onshore bond yields have edged higher, although more so at the front end. The US-CH 2yr bond yield differential is down from recent highs (+105bps versus +115bps in early August). This may help CNH sentiment at the margin, although USD/CNH spot still looks too low relative to current differential levels.

- We still await July aggregate finance figures, while Monday next week delivers the monthly data run of IP, retail sales, and fixed asset investment for July.

Fig 1: China Relative Equity Performance & CNY NEER

Source: J.P. Morgan, MNI/Market News/Bloomberg

Source: J.P. Morgan, MNI/Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok