Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

IDR

Like elsewhere in the region, USD/IDR is fairly range bound today. Spot is slightly higher in USD/IDR terms, last around 15120/25 (+0.15% for the session). Support is still evident around the 15100 levels, whilst both the 20 (15109.6) and 200-day (15129.65) EMAs are nearby.

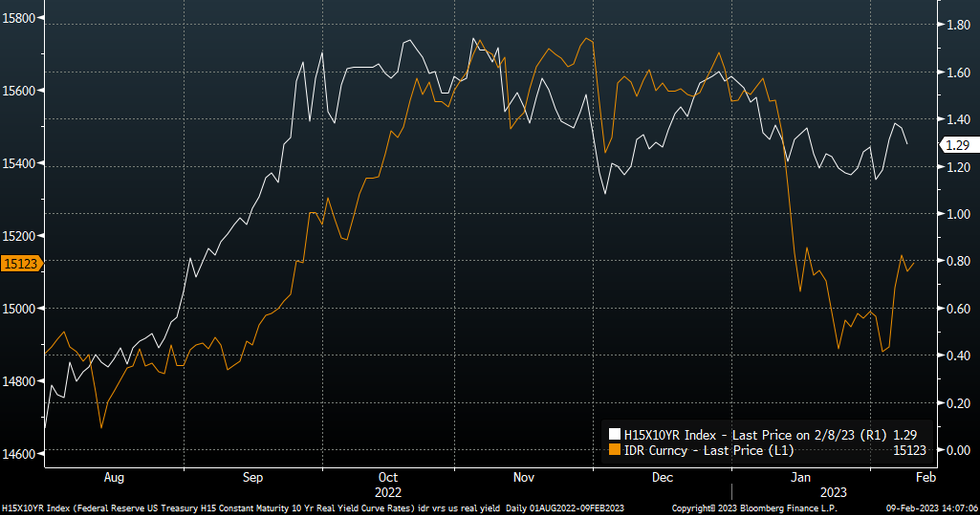

- We may stick to broad ranges ahead of next week's important US CPI release. IDR still has a reasonable correlation with US real yields, see the chart below.

- In terms of cross asset drivers, the Citi terms of trade proxy continues to trend lower, while the 5yr CDS is up off recent lows, post the US non-farm payrolls report.

- Encouragingly for IDR bulls, flows have continued into Indonesian government bonds post the payrolls report, with a further $245.1mn so far this week.

- On the data front, retail sales rose +0.7% y/y in Dec, with a +1.7% estimate for Jan, although this appears to reflect base effects, with the m/m estimate at -2.1% for Jan.

- The next major data release is trade figures out next Wed. So offshore drivers are likely to remain key for IDR sentiment.

Fig 1: USD/IDR v US Real 10yr Yield

Source: MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok