Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

ITALY DATA

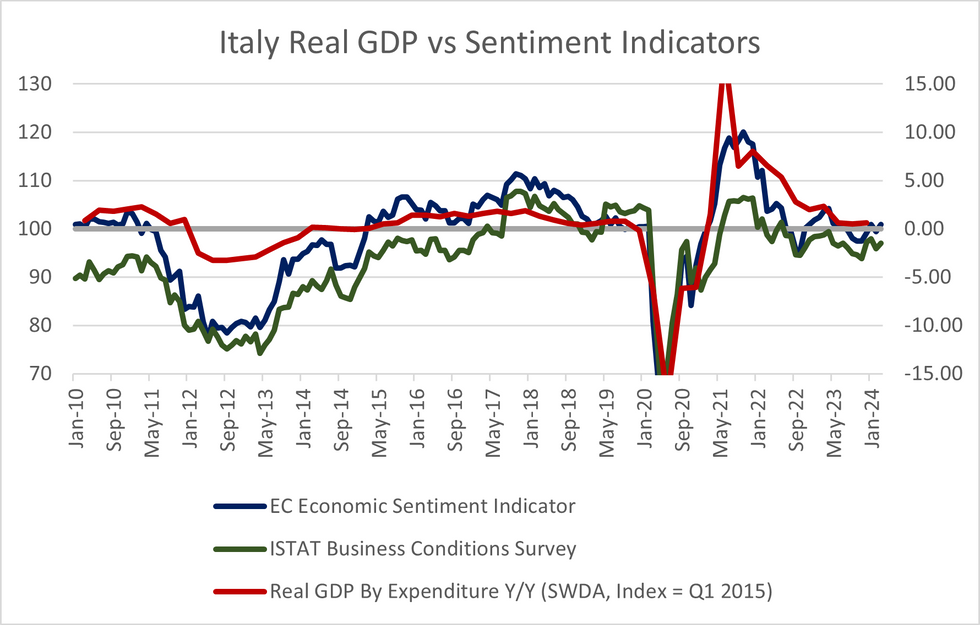

ISTAT's Economic Sentiment surveys saw the consumer confidence index at 96.5 in March (vs 97.6 cons, 97.0 prior) and business confidence at 97.0 (vs a 0.1pp upwardly revised 95.9 prior).

- The data generally aligns with yesterday's EC survey, where consumer confidence dipped slightly to -16.7 (vs -16.0 prior) and overall sentiment rose to 100.9 (vs 99.4 prior).

- On the consumer side, we note that the latest analyst consensus for Q1 '24 household consumption has been lowered to 0.2% Y/Y (from an initial 0.8% Y/Y). The ISTAT survey shows consumers' "future climate" expectations remaining in contractionary territory at 97.2 (vs 97.1 prior).

- Regarding the business survey, all industries saw an increase in confidence across both surveys in March, with the most notable increase in retail trade (ISTAT: 104.6 vs 100.8 prior; EC: 11.2 vs 7.5 prior). However, this comes following a surprising fall in February, and both retail trade indices remain below January's levels.

- The EC survey showed falling inflationary pressures amongst both services and retail respondents, suggestive of further services HICP disinflation ahead.

- Tomorrow's flash March release will provide more colour here, though calendar effects related to the early Easter will add an additional layer of uncertainty. Consensus sees March flash HICP rising due to energy base effects, at 1.5% Y/Y (vs 0.8% prior) and 1.4% M/M (vs 0.0% prior).

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok