Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

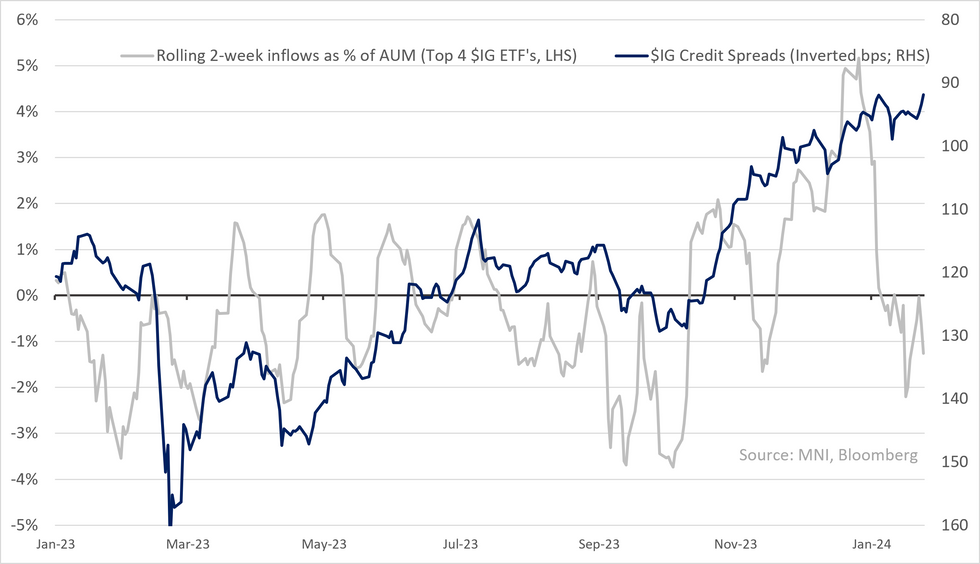

$ & € IG turned back to inflows for the week ending Wednesday, both more than reversing last weeks outflows. Little news given the primary metrics we've seen & stabilisation in $IG ETF outflows through the week. Flows have been met by still in-line supply - $IG at $37b (c$30b) but includes $13b into high-grade pharma from Bristol-Myers & for Euro & Sterling IG/HY €19b (c€21b) including €5b into Industrials from Siemens. There were fears February would see opportunistic issuance brought forward (from seasonally higher gross supply month of March) - little evidence of that yet - Jan NFP changing the rates backdrop might be helping.

€IG spreads have kept up with $ this week despite index yields reversing lower (while $ rose on rates) - a supportive sign re. local credit demand. Hard to point to fundamentals making up for rising yield differentials - €IG & $IG equity baskets have moved in tandem and there haven't been large forward earnings revisions in either region - SPW -0.1%, SXXP +2.5% on FY24 EPS est's since earnings began. We have seen higher US rates show up in $HY (lack of compression vs. €IG) - as we've mentioned ICR's look poor further down in index buckets like CCC's (across both regions) - still single B's remain the best performing locally YTD.

Outside of credit, equites inflows continued at pace - US equities reversing last week's outflows while Chinese equities continued to see inflows.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.