Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

CREDIT MACRO

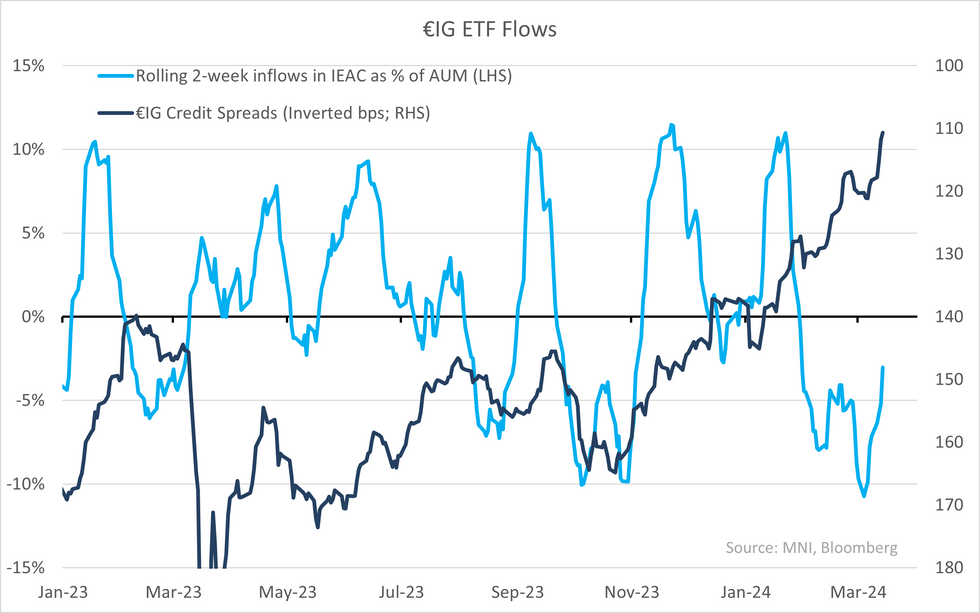

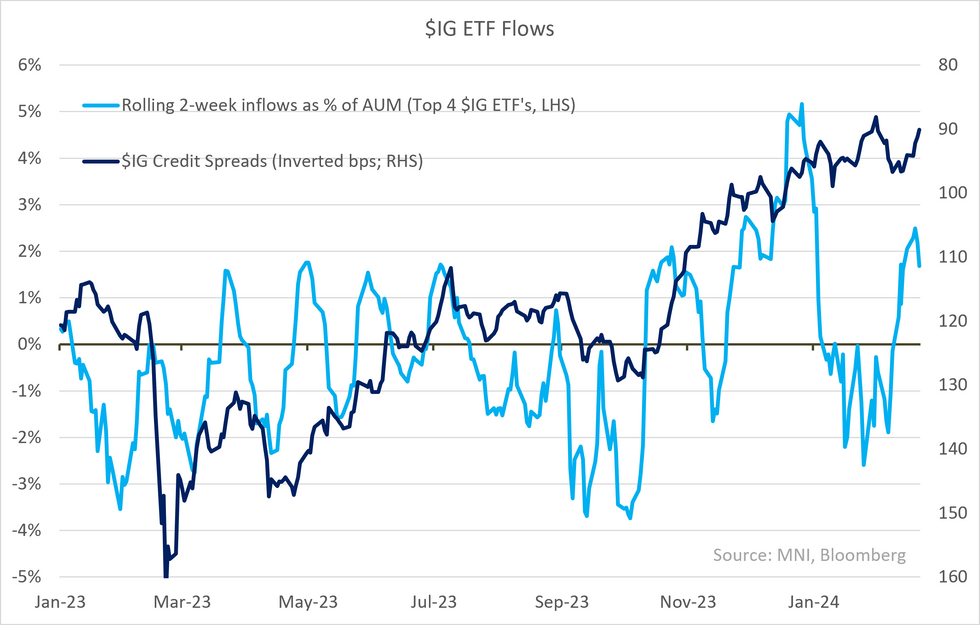

- Credit inflows continued in Euro & USD IG/HY - given muted inflows into ETFs we continue to see it driven by conventional/mutual funds. Regardless inflows have been enough this week to support within expectations supply of $37b in $IG (for a change) & above consensus €30m in Euro/Sterling IG/HY (with Friday deals to price as well).

- On £IG; it continued to see outflows for 3rd straight week - again its not evident in secondary spreads (IG/HY -6/-13bps WTD) but we saw signs of it in (certain) primary deals (like high-grade Nestle). £ supply still remains muted - £2.4b in IG is running slower than last 3 years and comes off a very slow February (£2b vs. £8b in Feb last yr).

- Outside of credit, $ govvies saw small outflows while € continued to receive inflows. US equities saw very strong inflows & is continuing recent strength (despite indices trading ~sideways this week) - muted equity flows outside of the US.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok