Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US

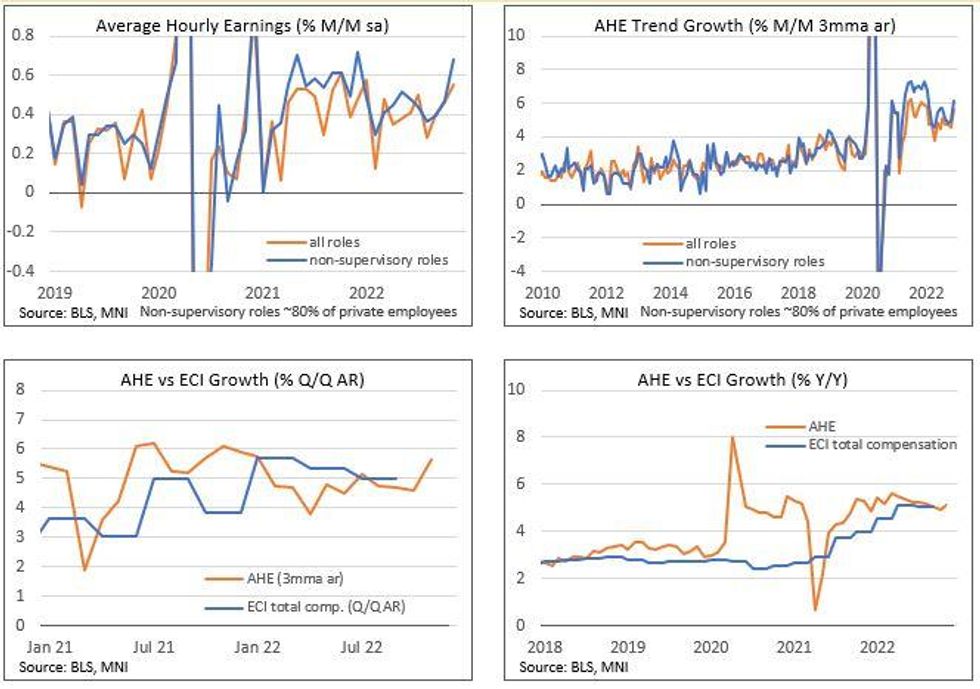

The November employment report's earnings component was probably the most concerning from a Fed "pivot" theory perspective.

- A 0.2-0.3% M/M increase would have seen Y/Y slip from 4.7% to 4.5-4.6%, but instead there was an acceleration, from an upwardly-revised 4.9% in Oct to 5.1% in Dec. 4.5% would be more consistent with mid-3s core PCE inflation; 5+% is 4%, roughly speaking.

- AHE is a volatile series to be sure, and there may be some issues at play in the past couple of months.

- Some theories presented to us include that it incorporates severance pay for laid off employees (particularly in transportation) and / or that higher-salaried employees are increasingly taking on well-paying non-supervisory service jobs.

- The better test will be in the metrics that compensate for compositional issues: namely the ones the Fed looks most closely at, the Employment Cost Index (the Q4 2022 edition is only due out Jan 31, the 1st day of the 2-day FOMC meeting), as well as the Atlanta Fed Wage Growth Tracker (usually comes out the 2nd Friday of the month, so next week).

- They will be watched unusually closely for any confirmation of wage acceleration.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok