Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

GOLD

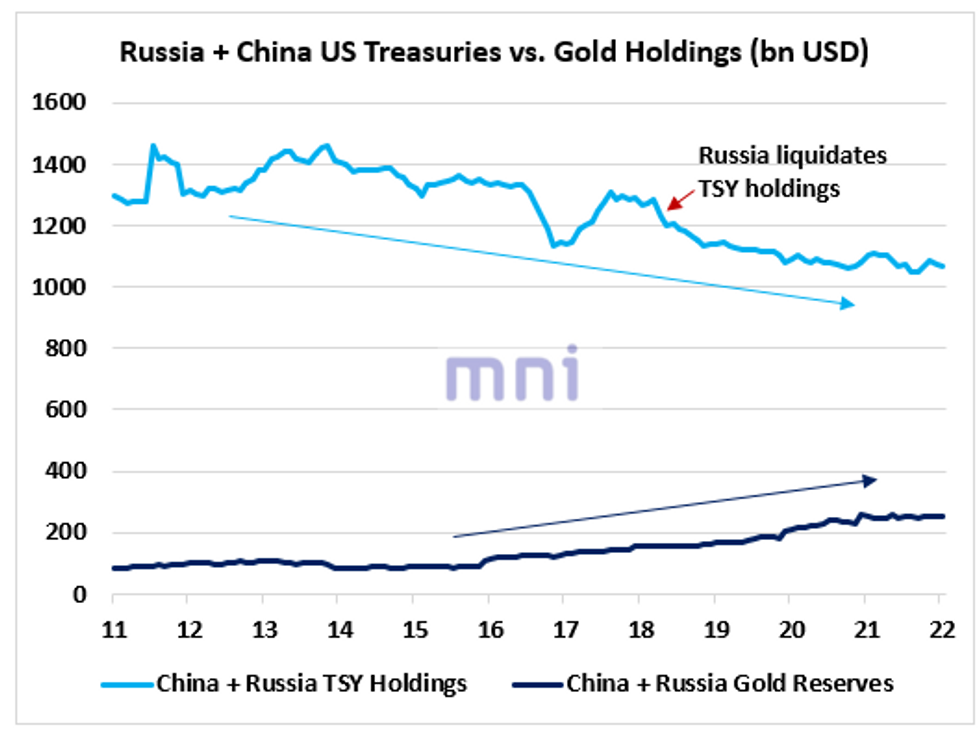

- One interesting topic that has been making the headlines in the past decades has been the ‘De-dollarization’ and the ‘Great Rotation’ from USD to non-USD FX reserves, particularly for China.

- China, which has historically been one of the top holders of US Treasuries (with Japan), has been gradually losing its interest in US ‘safe-haven’ securities in recent years.

- The chart below shows that the combined holdings of US Treasuries from China and Russia have declined from a 1,46tr USD in November 2013 to 1.06tr USD in January 2022 according to the TIC data.

- As a reminder, Russia liquidated nearly all of its TSY holdings between March and May 2018.

- Investors have been questioning if the recent sanctions imposed to Russia will accelerate the loss of China’s interest in US Treasuries.

- Russia’s accessibility to its FX reserves more than halved following the freeze of assets from Western economies as a response to the Ukraine invasion, erasing its last eight years’ effort of nearly doubling its reserves from 368bn USD to 630bn USD.

- Therefore, interests for gold could continue to surge in the medium term; the chart shows that Russia and China’s total gold holdings have increased by 170bn USD to 250bn USD in the past 6 years.

- Some analysts have argued that China’s reported measure of gold holdings (120bn USD, slightly below 2,000 tones) has been very questionable given that China has been the world’s biggest producer of gold since 2007, contributing to 12% of the annual production (380 tones).

- As gold export from the Chinese domestic market is prohibited by the PBoC, it is very likely that Chinese gold reserves are significantly higher than currently reported, implying that the Russia/China gold holdings dark blue line would also be much higher.

Source: Bloomberg/MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok