Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

STIR

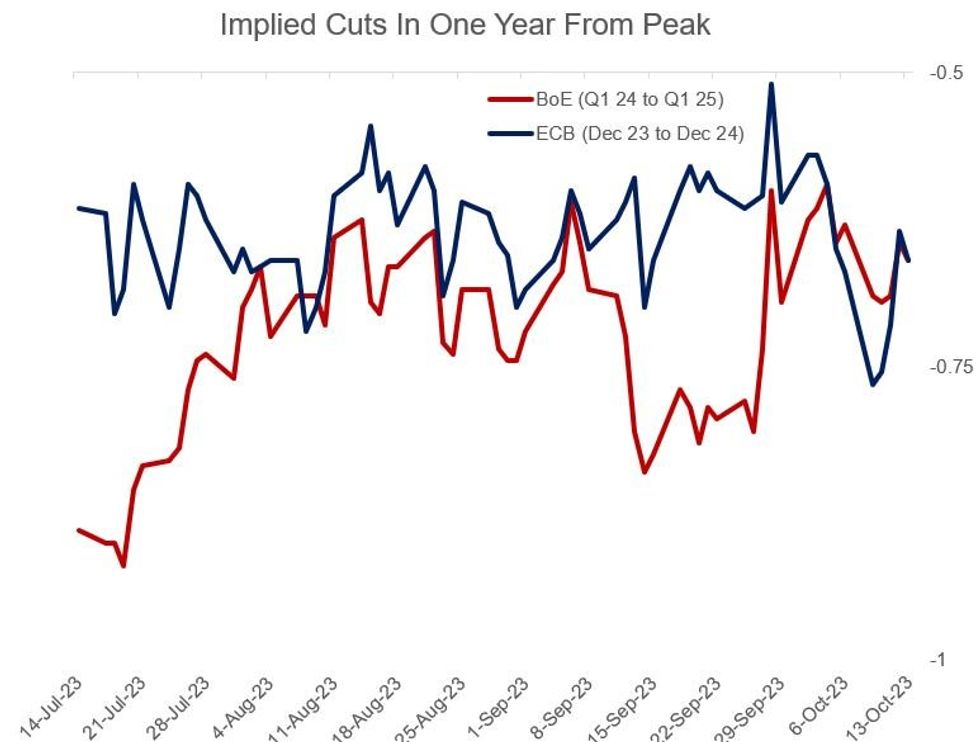

Market-implied ECB and BoE rate-cutting expectations were augmented slightly Friday amid risk-off trade.

- There's 66bp of reductions seen in the 12-months following peaks for both the ECB (Dec 2023 to end-2024) and BoE (Feb/Mar 2024-Mar-2024). That's around 2bp more cuts than was seen Thursday.

- As for hikes, there's been little change in implied pricing this week/month: around 1-2bp of further ECB hikes to Dec 2023 remain implied (despite Lagarde today reiterating that the central bank is ready to do more if necessary); peak UK pricing was flat, with 14-15bp of tightening priced through Feb 2024, marginally higher on the day.

- There's still just 8bp (around 1-in-3 chance of a 25bp hike) priced for the November 2 BoE MPC decision.

- With that in mind, attention turns primarily to the UK next week with the highlight being the CPI release next Wednesday; it's a quieter schedule for the Eurozone, with final September HICP and German ZEW on the docket.

- There's also another set of ECB/BoE speakers, but judging from this week they don't appear to be moving the needle much, with geopolitics and US macro developments seemingly carrying more weight.

Source: BBG, MNI

Source: BBG, MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok