Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

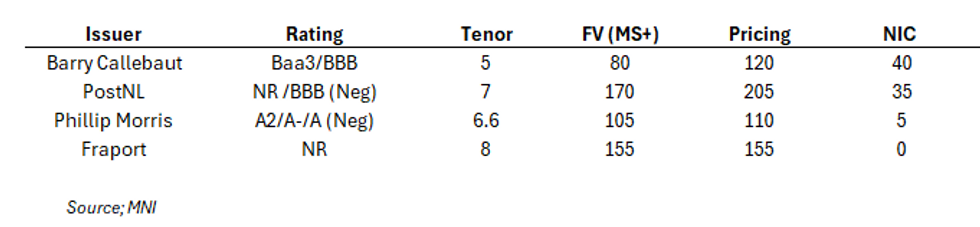

After Pandora's 15bp NIC & and Coty's 20 two weeks ago we added "a repeat of this week looks unlikely ahead of a seasonal summer lull particularly in July/August." We spoke to soon; PostNL handing out 35 and Barry Callebaut 40. They came while secondaries held firm - in PostNL's case we were eyeing IDSLN28s mids & for Barry a switch from anything broadly consumer related looked attractive yet nothing moved. If the new issues don't trade the NICs away, it leaves some tough questions to be answered on secondary levels; like why one would be parked in combustibles heavy Altria or Imperial over the largest cocoa processor for 5bps more carry.

"A high-grade airport not pricing through its curve" was another fascination we had two weeks ago with Avinor. Fraport has reminded us to not get too excited about airports with its unrated issuance and moves in secondary. As Ryanair's CEO O'Leary said last month when justifying his €3-4b net cash target, another downturn is only a matter of time. When/if that does happen the new Fraport 32s would be high up on our list of potential shorts.

In macro, Eurozone retail sales continued the April weakness we have already saw in US/UK prints, falling -0.5% MoM which left it flat yoy. We got early read-through on May card data (see below) which pointed to paring of April weakness including in Apparel. Other key notes from the week linked below.

- The Post-mortem on PostNL

- PVH29s cheap view back

- Tesco short-end coming out as expected but it's taking our cheap views with it

- LCC's May Traffic

- Early May US card data, VF still depressed on second measure

- VF and Flutter's equity vol has little read-through for us

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.