Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

USD

Since mid-January USD indices have largely tracked sideways. The Fed meeting later today shapes as key one in terms of short term USD sentiment.

- As our Fed preview noted, "The dovish risks to this meeting appear at least partly priced in, including some expectations of Statement language acknowledging decelerating inflation, or a clear signal that the end of the hiking cycle is near. However, there are many ways Powell could re-emphasize the FOMC’s view that the job is not nearly done yet."

- Arguably this raises the bar in terms of Fed dovishness needed to see a fresh wave of further USD selling.

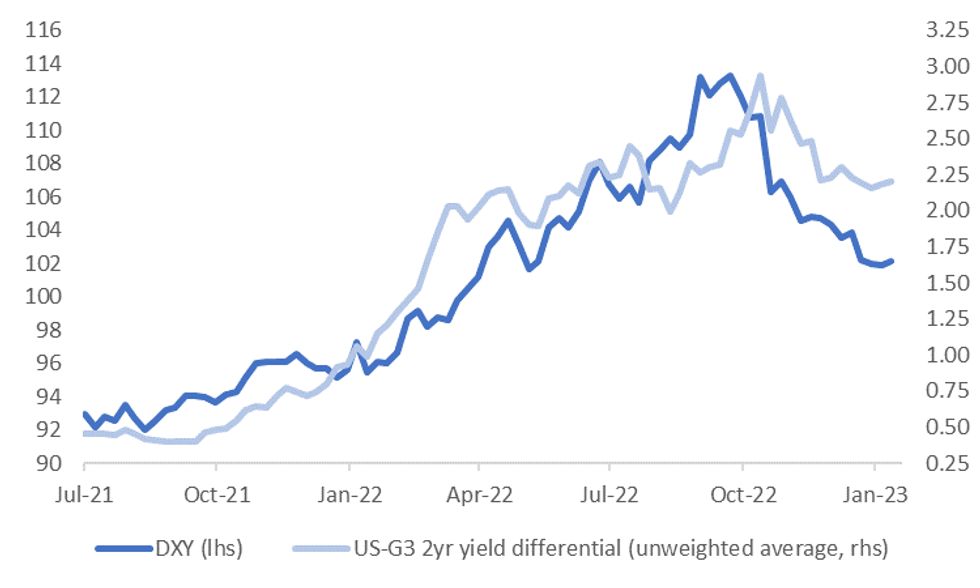

- The first chart below overlays the DXY index against the unweighted 2yr yield differential on a 2yr government bond yield basis. This differential has also stabilized in recent weeks, although more so against JP and UK yields rather than the EU.

Fig 1: DXY Versus US-G3 2yr Yield Differential

Source: MNI - Market News/Bloomberg

- Of course, the market may also pushback against any relative Fed hawkishness. Relative data surprises have also swung against the USD.

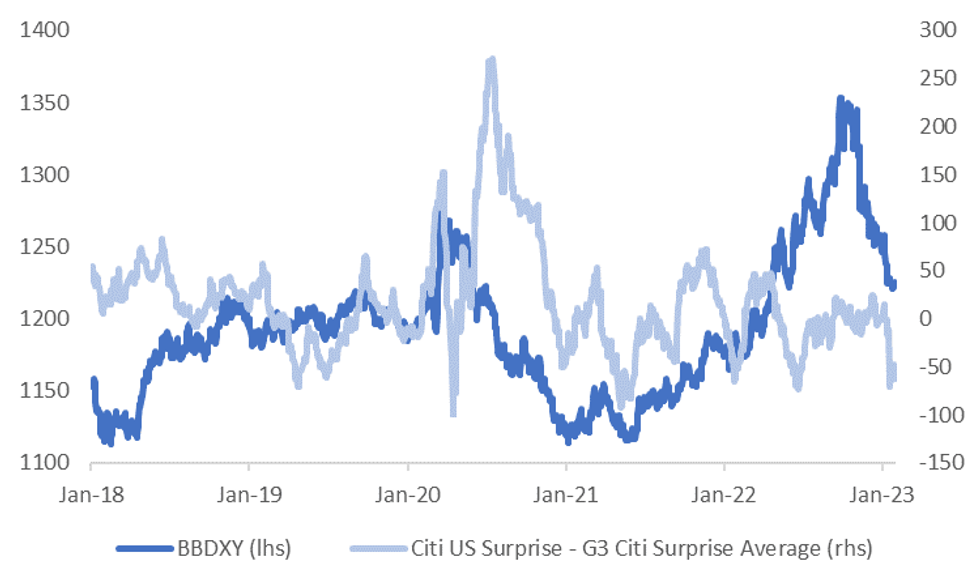

- The chart below plots the BBDXY index against the Citi US Surprise index differential with the EU, Japan and China Citi Surprise Indices.

- Interestingly though, we aren't too far away from recent trough points for this differential, at least using the last 5 years worth of history. If we see this differential start to stabilize it may take away one headwind for USD, all else equal. It's also hard not to argue some of this differential is also not priced in by the USD to some degree.

Fig 2: BBDXY Versus US Citi Surprise Index Differential With EU, Japan & China Average (Unweighted)

Source: Citi/MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok