Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

CHINA

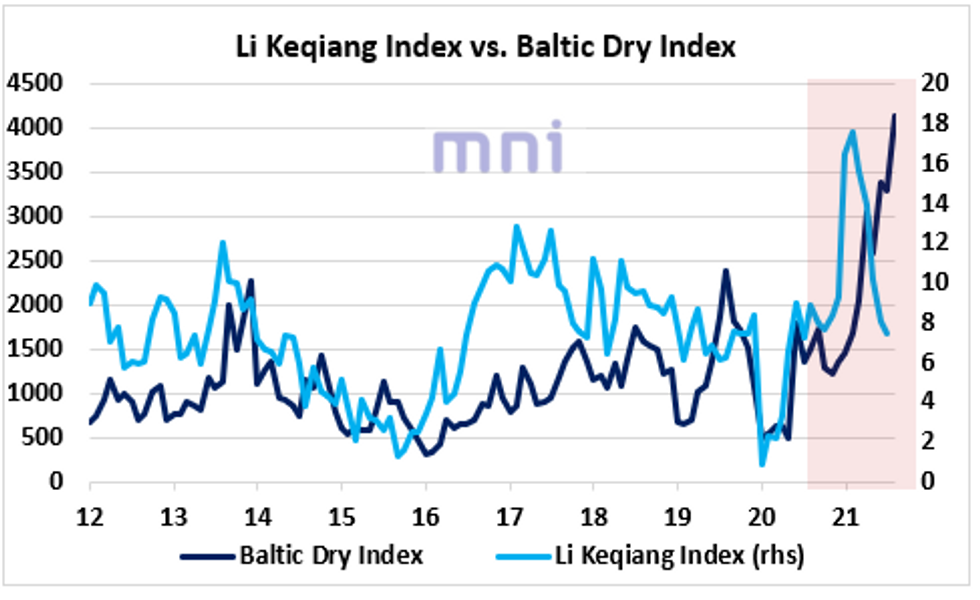

- Interestingly, the divergence persists between China Li Keqiang Index, which could be considered as a proxy of the Chinese real economic activity, and the Baltic Dry Index, which some investors view as a proxy for world trade and therefore for the global economy.

- China Li Keqiang Index, which is an economic measurement index that tracks China's economy using three indicators - railway cargo volume, electricity consumption and loans disbursed by banks, has been plunging since its peak reached in February, from a high of 17.61 to 7.44.

- The deceleration in the Chinese economy (and other Asian and SE Asian economies) amid rising uncertainty over the Delta variant has been concerning for global growth considering Chinese important contribution for global growth (and BRICS growth).

- We saw yesterday that China non-manufacturing PMI dipped below the 50-line threshold that separates growth from contraction for the first time since March 2020, falling to 47.50 in August, bringing down the composite PMI to 48.9.

- On the other hand, the Baltic Dry Index (BDI) keeps reaching new highs, currently standing at its highest level since November 2011, indicating strong demand for dry bulk commodities.

- Could the persistent rise in inflationary pressures combined with the strong demand across vessel segments be positive for global commodities, or will the deceleration in Chinese economy and the sharp liquidity contraction (China TSF) weigh on risky assets (commodities) in the near to medium term?

Source: Bloomberg/MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok