Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EUROZONE DATA

MNI (London)

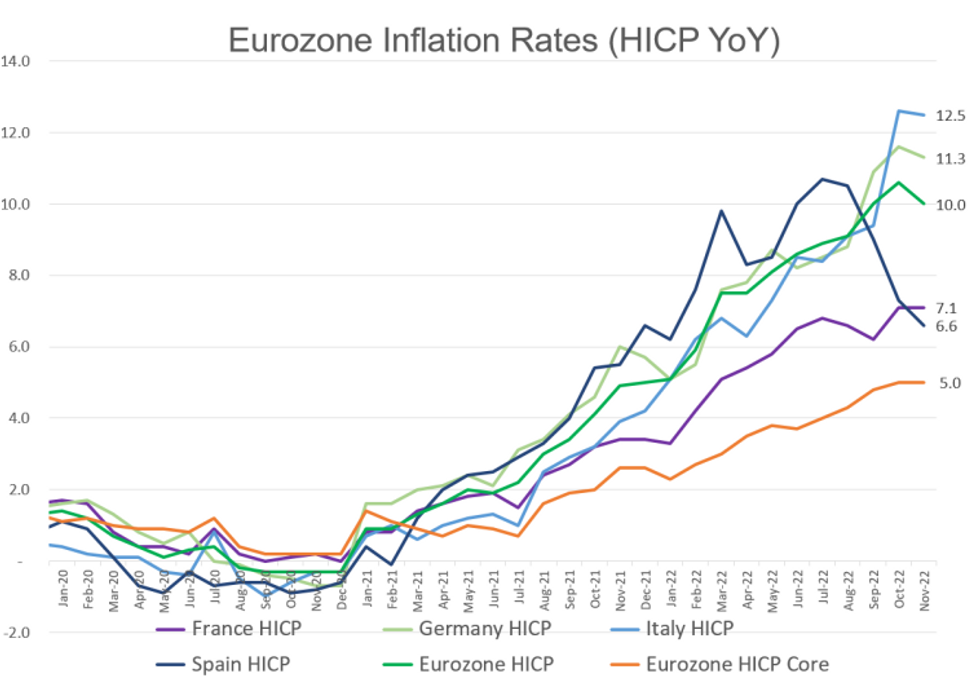

EUROZONE NOV FLASH CPI -0.1% M/M (FCST +0.2%); OCT +1.5% M/M

EUROZONE NOV FLASH CPI +10.0% Y/Y (FCST +10.4); OCT +10.6% Y/Y

EUROZONE NOV FLASH CORE CPI 0.0% M/M, +5.0% Y/Y (= FCST); OCT +5.0% Y/Y

- Eurozone inflation saw a downside surprise in the November flash, deflating by -0.1% m/m and cooling by 0.6pp to +10.0% y/y in the headline print. Only Slovenia, Slovakia and Finland recorded higher November year-on-year rates.

- Despite improvements in headline inflation, core CPI held steady at +5.0% y/y as anticipated. Prices stalled on the month at 0.0%.

- Inflation has as such come off its October record high, supported by the -1.9% m/m fall in energy prices. This left annualised energy inflation 6.6pp lower at +34.9% y/y.

- Food prices continued to accelerate, up +0.9% m/m (+13.6% y/y vs +13.1% in Oct), yet industrial goods held stable (+6.1%) and service prices fell by -0.3% m/m, easing by a marginal 0.1pp to +4.2% y/y.

- Markets have downgraded the ECB terminal rates to closer to 2.8-2.9% in mid-2023 and are currently pricing around 56bp for the November rate decision. Yet the lack of easing in core inflation likely implies the decision between 50bp and 75bp could be on a knife's edge.

Source: MNI / Eurostat

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok