Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US TSYS: Aug CPI Underscores Fed Chair Powell's Transitory Inflation Message

Weaker than anticipated August CPI 0.3% vs. 0.4% est (0.5% prior and core of 0.1% was the catalyst for long-end lead rally in rates and flatter curves Tuesday, while equities traded weaker -- technical support held (ESZ1 -31.0 at 4428.50). Tsy

30YY fell back to early August level of 1.8292% last seen Aug 5.

- Today's data underscores Fed Chairman Powell's "transitory inflation" message, but remember the Federal Reserve remains in media blackout until September 23.

- Trade surged, TYZ1 >1.4M twice that of Monday's post-close volumes, but dog days of summer malaise resumed in the second half.

- Option volumes proved muted, vol sellers emerging by midmorning while low delta put buyers noted in Oct 5- and 10Y options.

- No Treasury bill auctions, but corporate issuance remined robust with over $18B pricing on the day after $24.4B on Monday.

- The 2-Yr yield is down 0.6bps at 0.207%, 5-Yr is down 2.6bps at 0.779%, 10-Yr is down 5.1bps at 1.2752%, and 30-Yr is down 5.8bps at 1.8465%.

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements

- O/N -0.00150 at 0.07188% (+0.00025/wk)

- 1 Month +0.00088 to 0.08463% (+0.00075/wk)

- 3 Month +0.00200 to 0.11800% (+0.00225/wk) ** Record Low 0.11413% on 9/12/21

- 6 Month -0.00075 to 0.14788% (-0.00150/wk)

- 1 Year -0.00063 to 0.22250% (+0.00000/wk)

- Daily Effective Fed Funds Rate: 0.08% volume: $67B

- Daily Overnight Bank Funding Rate: 0.07% volume: $262B

- Secured Overnight Financing Rate (SOFR): 0.05%, $914B

- Broad General Collateral Rate (BGCR): 0.05%, $382B

- Tri-Party General Collateral Rate (TGCR): 0.05%, $354B

- (rate, volume levels reflect prior session)

- Operations resume Wednesday:

- Wed 9/15 1010-1030ET: Tsy 0Y-2.25Y, appr $12.425B

- Thu 9/16 1010-1030ET: Tsy 22.5Y-30Y, appr $2.025B

- Fri 9/17 1010-1030ET: TIPS 1Y-7.5Y, appr $2.025B

- Next week's buy-operations:

- Mon 9/20 1010-1030ET: Tsy 7Y-10Y, appr $3.225B

- Tue 9/21 1010-1030ET: TIPS 7.5Y-30Y, appr $1.225B

- Wed 9/22 No buy operation scheduled due to FOMC

- Thu 9/23 1010-1030ET: Tsy 10Y-22.5Y, appr $1.425B

- Fri 9/24 1010-1030ET: Tsy 4.5Y-7Y, appr $6.025B

FED: REVERSE REPO OPERATION, $20B Off Record High

NY Fed reverse repo usage climbs to 1,169.280B from 80 counter-parties vs. $1,087.108B Monday. Record high holds at $1,189.616B set Tuesday, Aug 31.

EURODOLLAR/TREASURY OPTIONS SUMMARY

Eurodollar Options:- +5,000 Green Dec 98.62/98.75/98.87 put flys, 1.25

- -6,000 short Dec 99.25/99.50 put spds, 2.0 vs. 99.58/0.10%

- -1,500 Green Nov 99.00 straddles, 20.5-20.0

- -1,000 Blue Mar 98.50/98.62 strangles, 38.0

- Overnight trade

- Block -3,742 Blue Dec 97.62/98.00 3x2 put spds, 2.0 w/another 17.5k on screen

- +11,000 short Dec 99.25/99.37/99.50 put flys, 2

- 5,000 short Dec 99.37 puts

- +20,000 short Mar 99.25 puts, 6.0

- Over 12,000 FVV 123.5 puts 9.5-10

- +15,000 TYV 131.5 puts, 1

- +5,000 TYX 131/132 2x1 put spds, 3

- -5,000 TYV 134 calls, 4

- 9,170 FVX 122.75/123.25 2x1 put spd

- Overnight trade

- +5,800 TYV 134 calls, 6

- +3,500 FVZ 121.5/122.5 put spds, 8

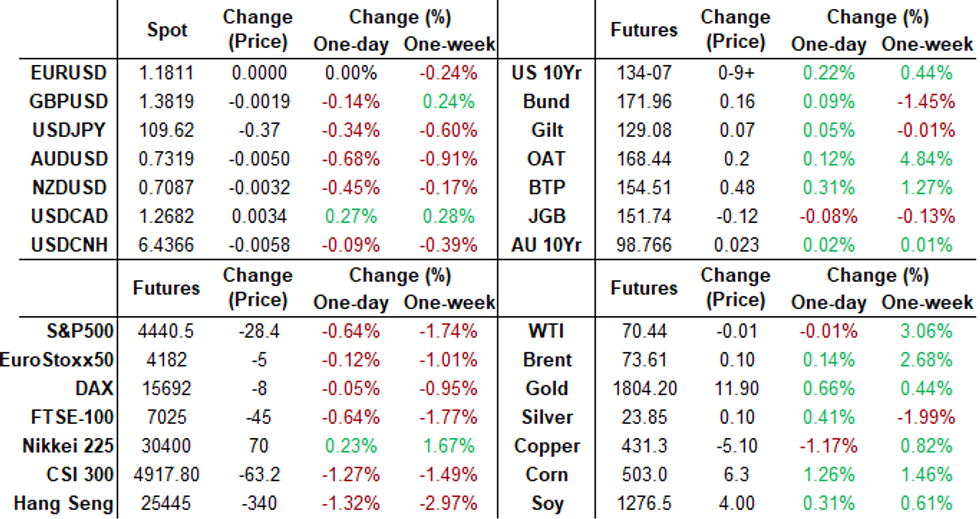

EGBs-GILTS CASH CLOSE: US CPI Lifts All Boats

A downside miss in the much-anticipated US CPI data release buoyed the European FI space Tuesday, with early supply-driven weakness reversing.

- The Bund and Gilt curves bull flattened slightly, while Italy outperformed - 10Y BTP spreads/Germany hit lowest level since Aug 13 (98.1bp).

- Supply this morning came from the UK (Gilt, GBP3bn), Germany (Schatz, E3.9bn allotted), Italy (BTPs, E9.0bn), plus E9bn EU NGEU 7Y syndication.

- UK employment data came in stronger than expected; Aug CPI data Weds morning enters focus.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is up 0.5bps at -0.7%, 5-Yr is down 0.3bps at -0.644%, 10-Yr is down 0.9bps at -0.34%, and 30-Yr is down 1.4bps at 0.152%.

- UK: The 2-Yr yield is up 0.3bps at 0.231%, 5-Yr is up 0.5bps at 0.419%, 10-Yr is down 0.7bps at 0.738%, and 30-Yr is down 1.3bps at 1.043%.

- Italian BTP spread down 3bps at 98.7bps / Spanish down 1.4bps at 64.6bps

EGB Options: A Couple Of Schatz Structures

Tuesday's European rates / bonds options flow included:

- DUZ1 112.3/112.4 call spd 1.75 over DUV1 112.3 calls paid 10k

- Buying DUZ1 112.30/112.40 call spread vs Selling 112.10 puts for net 0.5

- OEX1 135.75/136cs vs 135p, bought the cs for -3.5 (receives) in 2k

- RXV1 171.50p, sold 16k at 54.5/54 (ref 171.34), and 9k at 44 (ref 171.50)

- RXV1 171.5/170.5ps 1x1.33 was sold at 28 in 5k

- ERM3 100.62/100.50ps 1x2, bought for -5.5 (receives) in 4.5k

- 0LZ1 99.37/99.25ps 1x2, bought for 0.75 in 10k

FOREX: Cross-JPY Under Pressure As Risk Sours Post CPI

- Lower than expected headline CPI figures worked against the greenback at the outset with the dollar index shedding roughly 30 pips.

- Consistent pressure on equity indices following the data has kept risk-tied currencies under pressure and safe haven fx firmly bid with the Japanese Yen and Swiss Franc notable beneficiaries.

- With risk sentiment weighing, AUDJPY was the worst performing currency pair, down a little over 1% for Tuesday. Despite yesterday's minor uptick, this will be the sixth losing session in the past 7 trading days for the pair, giving up the majority of September's gains.

- USDJPY is currently testing the first support band of 109.59/41 Low Aug 31 and Sep 3 / Low Aug 24.

- Technically, a bearish risk is still present and key support lies at 108.72, Aug 4 low where a break would strengthen a bearish case and open 108.47, a Fibonacci retracement.

- Elsewhere EURUSD printed a fresh high for the week at 1.1846, however, the single currency has gradually reversed, turning negative as we approach Tuesday's close of play.

- GBPUSD also had a sharp turnaround off the highs at 1.3913 to trade a full big figure lower and hover above Monday's worst levels at 1.38.

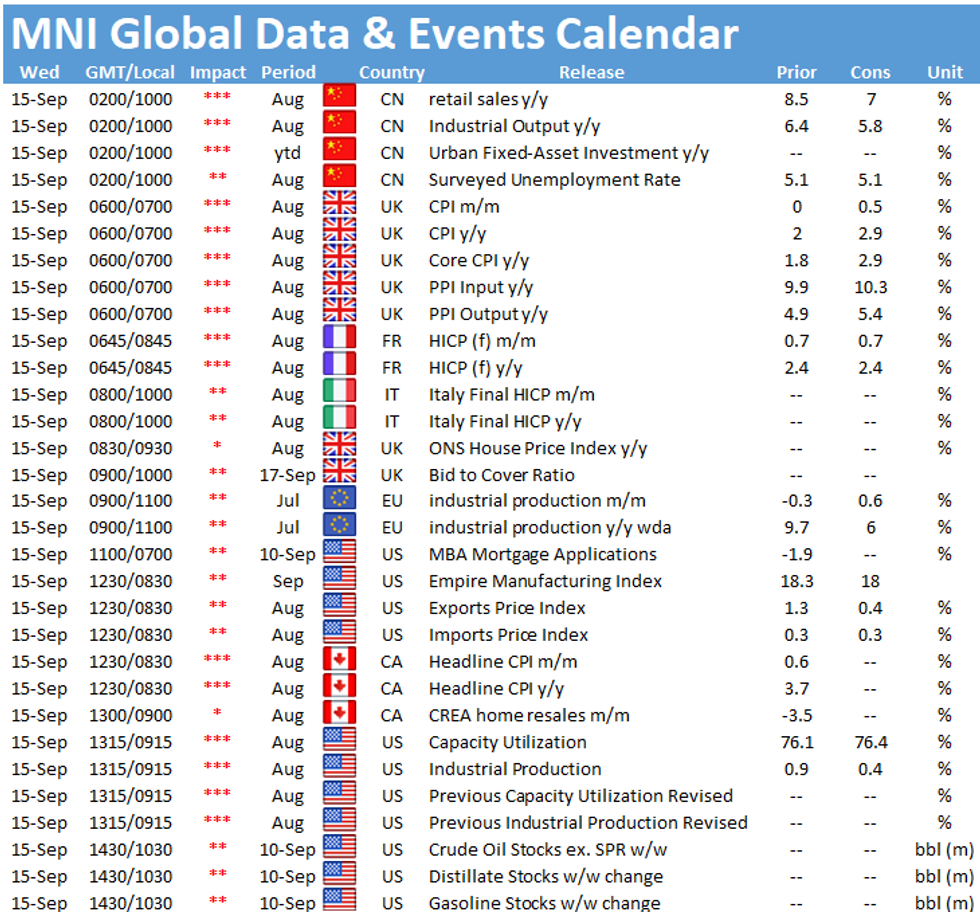

- Chinese retail sales are due overnight before markets will turn to UK and Canadian CPI data on Wednesday.

- US Empire State Manufacturing Index and Industrial production will headline the US docket.

FOREX: Expiries for Sep15 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1800(E647mln), $1.1820-30(E1.0bln), $1.2000(E1.1bln)

- USD/JPY: Y109.60-80($1.5bln), Y110.00($686mln)

- USD/CAD: C$1.2750($660mln), C$1.2795-00($988mln)

PIPELINE: Updated Guidance, Chile to Launch Soon

Date $MM Issuer (Priced *, Launch #)

- 09/14 $4.25B #Hungary $2.25B 10Y +100, $2B 30Y +150

- 09/14 $3B #Hyundai Central America $1.2B 3Y +63, $1B 5Y +88, $800M 7Y +105

- 09/14 $2B *Ontario Teachers Fnc Trust 5Y +10

- 09/14 $1.5B #BP Capital Mkts $1.25B +30Y +117, $250M 40Y +127

- 09/14 $1.5B *Sinochem $400M 3Y +65, $600M 5Y +80, $500M 10Y +110

- 09/14 $1B #Norichukin Bank $00M 5Y +50, $500M 10Y +80

- 09/14 $1B *Nordic Investment Bank 3Y -5

- 09/14 $1B Rep of Chile WNG 50Y +160a

- 09/14 $850M #Carlisle $300M 2NC1 +37, $550M 10.5Y +97

- 09/14 $Benchmark Bank of America 15NC10 +120

- 09/14 $2B Coinbase $1B 7NC3 3.375%, $1B 10NC5 3.625%

- Expected Wednesday:

- 09/15 $1B Council of Europe (COE) WNG 5Y -1a

- 09/15 $Benchmark IADB 3Y SOFR+15a

EQUITIES: Stocks Find Support as CPI Slows

- US equity markets traded in negative territory across both futures and cash space Tuesday, albeit indices recovered off the session lows as the pace of CPI inflation slowed across August. The figure came in below expectations, possibly adding to the pressure on the Fed that began with August's lower-than-expected payrolls.

- Indices continue to see support ahead of the key 50-dma. For the e-mini S&P, this level at 4423.84 has helped stem downside on numerous occasions this year, so will remain a market focus.

- The financials sector led markets lower, with the flattening of the US Treasury curve working against banking names. Energy and industrials similarly traded poorly.

COMMODITIES: Palladium Sinks, Death Cross Formed

- Oil markets remained supported throughout, with markets watching the formation of the Nicholas weather system, which could disrupt production further alongside the linger effects of Ida.

- Storm Nicholas has already struck Texas, with the high concentration of refining facilities in the area at risk of weather-forced shutdowns. Yesterday, the closing of the Port of Corpus Christi as well as the Houston Ship Channel were the first signs of disruption.

- Next resistance for WTI kicks in at the $73.52 Jul 30 high as well as the bear channel top drawn from the Jul 6 high at $71.37.

- Elsewhere in metals markets, palladium extended the recent slide to touch fresh 2021 lows and the lowest levels since mid-2020. The slip through $2,000/oz followed the formation of a death cross in DMA space, with the 50-dma falling through the 200-dma for the first time since June last year.

- Concerns over lagging auto production and the still-disrupted supply chain for chipmakers are weighing on demand, with the recent run-up in prices also prompting producers to switch to alternative raw materials. Support for Palladium undercuts at $1854, the 76.4% retracement for the recovery off the pandemic lows.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.