Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US TSYS: Ylds Climb After Mixed Data: Lower Claims/Weaker GDP, Weak 7Y Sale

Treasury futures hold weaker levels on heavy volumes by the close Thursday, just off second half lows of the day with curves mixed after more broad based flattening in first half (5s30s dropped to 73.349, Mar 2020 low).- Focus on data after ECB kept refi/deposit/lending rates unchanged. Tsys held weaker/inside overnight range after better than exp wkly/continuing claims (281k vs. 288k est; 2.243m vs. 2.420m est) while first look at 3Q GDP came out weaker than est: 2.0% vs. 2.6%.

- Robust volumes amid two-way in 2s-7s, carry-over buying in long end from bank and insurance portfolios. More steepener stop-outs for leveraged accts.

- Rates whipsawed midmorning: following Bund lead -- Tsys surged to session highs briefly only to extend session lows less than an hour later after ECB Lagarde press brief. Lagarde pushed somewhat back on market rate hike pricing, calling it inconsistent with ECB fwd guidance/infl forecasts, though "not for her to say" if markets had got ahead of themselves.

- Tsy futures back near lows after mediocre $62B 7Y note auction (91282CDF5) drew 1.461% high yield vs. 1.447% WI; 2.25x bid-to-cover in-line with Sep's 2.24x. Indirect take-up climbs to 63.89% (highest since Jan).

- Still no vote on bill, draft of Pres Biden's $1.75T social spending package leaked: Link: HR 5376

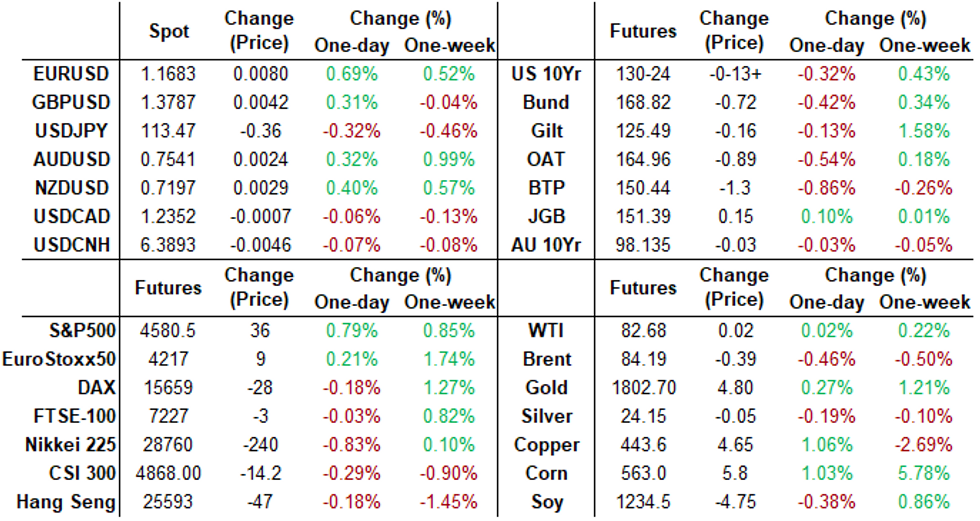

- The 2-Yr yield is down 0.6bps at 0.497%, 5-Yr is up 3.6bps at 1.1864%, 10-Yr is up 2.5bps at 1.5659%, and 30-Yr is up 1bps at 1.9603%.

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements

- O/N +0.00413 at 0.07363% (+0.00013/wk)

- 1 Month -0.00062 to 0.08638% (-0.00150/wk)

- 3 Month +0.00300 to 0.13163% (+0.00675/wk) ** Record Low 0.11413% on 9/12/21

- 6 Month +0.01400 to 0.19363% (+0.02163/wk)

- 1 Year +0.03838 to 0.37063% (+0.05375/wk)

- Daily Effective Fed Funds Rate: 0.08% volume: $78B

- Daily Overnight Bank Funding Rate: 0.07% volume: $267B

- Secured Overnight Financing Rate (SOFR): 0.05%, $865B

- Broad General Collateral Rate (BGCR): 0.05%, $356B

- Tri-Party General Collateral Rate (TGCR): 0.05%, $325B

- (rate, volume levels reflect prior session)

- Tsy 0Y-2.25Y, $12.401B accepted vs. $40.273B submission

- Next scheduled purchase

- Fri 10/29 1010-1030ET: Tsy 10Y-22.5Y, appr $1.425B

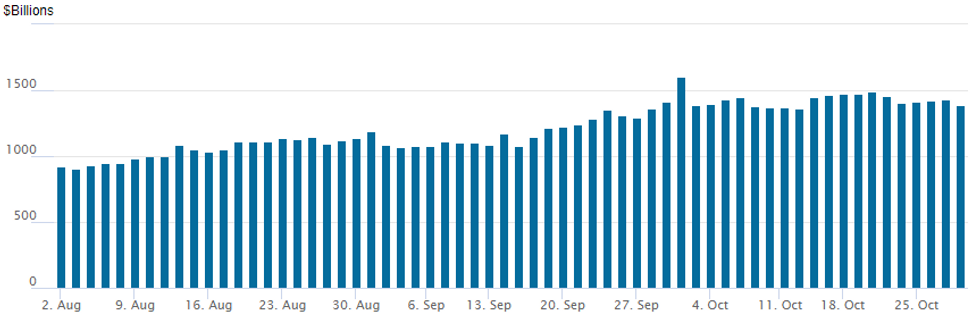

FED Reverse Repo Operation

NY Federal Reserve/MNI

NY Fed reverse repo usage recedes to $1,384.684B from 78 counterparties from $1,433.370B on Wednesday. Record high remains at $1,604.881B from Thursday, September 30.

EURODOLLAR/TREASURY OPTIONS SUMMARY

Eurodollar Options:- +60,000 Jun 99.81/99.87 call spds, 1.5

- +5,000 Green Dec 98.12/98.37 2x1 put spds, 2.0

- -2,500 short Mar 99.00/short Jun 98.87 straddle strips, 99.5 total

- +10,000 Blue Dec 99.12 calls, 0.5 vs. 98.355/0.05%

- Block, 17,000 short Dec 99.00/99.12 put spds, 4.5 vs. 99.13/0.14%

- Overnight trade

- Block, 6,600 Red Jun'23 98.75 puts, 42.0 vs. 98.74/0.48% at 0758:21ET

- +48,000 Dec 99.87 calls, cab (open interest pretty large on these upside calls at 382,584 coming into the session)

- 10,000 Gold Dec 97.62/97.87 put spds

- +2,000 TYZ 132 calls, 12

- +2,000 TYF 127.5/129.5 put spds, 33

- +5,500 TYZ 132.5 calls, 7 vs. 130-27.5/0.10%

- +5,000 TYZ 128 puts, 5

EGBs-GILTS CASH CLOSE: Volatile Session As ECB Debates Inflation

Thursday saw a very volatile session across the European FI space, highlighted by soaring Bund first futures volumes (1.2+mn, near March 2020 levels, eclipsed only by heavy Feb 2021 trading), and the 2nd highest daily BTP futures volume ever.

- But direction, while overall bearish, not entirely decisive. The morning saw a large short-end sell-off with global rate hikes brought forward, then the start of the ECB press conference saw Bunds sell off sharply, only to reverse higher and then lower again. BTPs underperformed.

- While the ECB (as expected) took no action and kept communications largely unchanged, Lagarde pushed somewhat back on market rate hike pricing, calling it inconsistent with ECB fwd guidance/infl forecasts, though "not for her to say" if markets had got ahead of themselves.

- BBG/Rtrs sources articles post-meeting highlighted an internal debate over the inflation outlook, with some on the GC sceptical of a fall below target in 2023.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is up 1.6bps at -0.624%, 5-Yr is up 2bps at -0.445%, 10-Yr is up 3.5bps at -0.143%, and 30-Yr is up 1.2bps at 0.167%.

- UK: The 2-Yr yield is up 8.6bps at 0.645%, 5-Yr is up 5.5bps at 0.763%, 10-Yr is up 1.7bps at 1.003%, and 30-Yr is down 2.7bps at 1.108%.

- Italian BTP spread up 6.4bps at 118.6bps / Spanish up 0.5bps at 65.4bps

EGB Options: Multiple Rate Condors

Thursday's rates / bond options flow included:

- RXZ1 168.5/167ps, 1x2, bought for 9 in 2.25k

- DUZ1 112.30/40 call spread vs 112.10/00 put spread bought for 5 in 8k (+ps). Closing

- L Z1 99.50/37/75/87c condor, bought was bought for 4 and 4.5 in 7k

- SFIH2 99.35/99.55/99.75c fly 1x3x2, bought for 1 in 5k

- SFIZ1 99.55/99.65/99.75/99.85c condor, bought for 2.75 in 8.5k

FOREX: Dollar Index Slides 0.5%, Weakness Extends Through October Lows

- The dollar has been under pressure throughout the latter half of Thursday's session and selling momentum in the dollar index has accelerated following the break of short-term support below the October lows.

- The DXY (-0.5%) has consolidated near the lows, having reached the first area of support for the index. The selling coincides with sell-side month-end models uniformly pointing to USD sales into the October fix, with some models noting the signal is strongest against the JPY.

- The main beneficiaries of the greenback weakness were the Euro and the Swiss Franc, both rising around 0.7%. EURUSD price activity picked up following during the ECB press conference where there was only a mild rates pushback, adding a marginal tailwind for the single currency.

- EURUSD had some clear levels of resistance to rip through, including multiple daily highs between 1.1665-69. The rally was capped at 1.1692, however, the move represents the largest daily range for EURUSD since mid-June of 110 pips. There is a key resistance at 1.1711, the top of a bear channel drawn from the Jun 1 high. Broader trend conditions remain bearish below this channel resistance.

- Gains in GBP, AUD and NZD were smaller in magnitude, although provide solid extensions of short-term bullish trends throughout October.

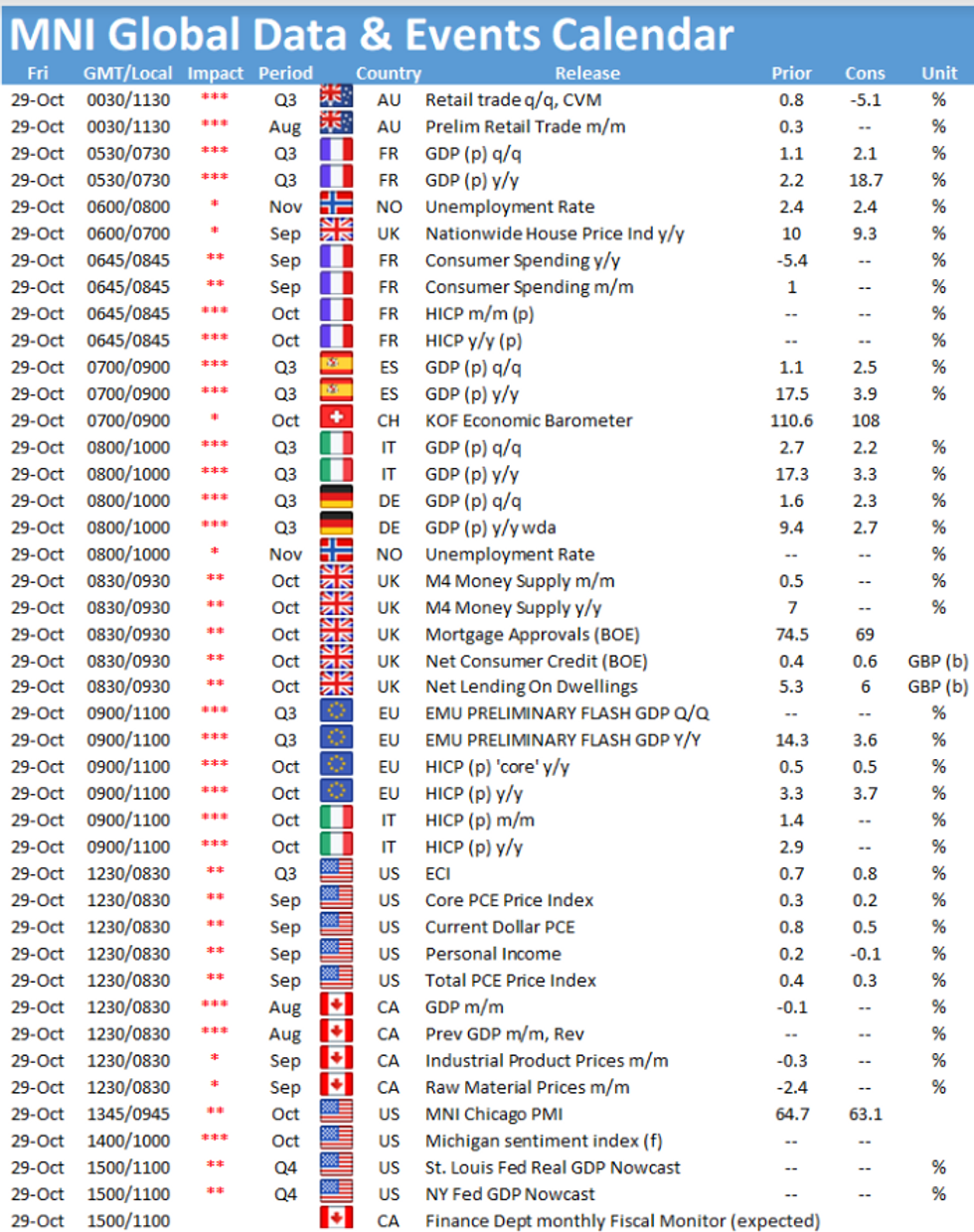

- European Flash GDP readings will precede Eurozone HICP Flash CPI Estimates. The US session will focus on Canadian GDP as well as US Core PCE Price Index. The week's calendar will conclude with the MNI Chicago PMI.

FX: Expiries for Oct29 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1480-00(E842mln), $1.1595-00(E1.3bln), $1.1645-55(E933mln)

- USD/JPY: Y113.00($674mln), Y113.75-90($1.3bln), Y114.60-75($1.4bln)

- NZD/USD: $0.7210(N$645mln)

- USD/CAD: C$1.2300($982mln), C$1.2345($610mln)

- USD/CNY: Cny6.4750($600mln)

PIPELINE: $4B Peru 3Pt Launched

- Date $MM Issuer (Priced *, Launch #)

- 10/28 $4B #Rep of Peru $2.25B 12Y +150, $750M 2051 Tap +150, $1B 50Y +180

- 10/28 $1.75B #Capital One $1.25B 6NC5 fix/FRN +70, $500M 11NC10 fix/FRN +105

- 10/28 $1.25B #Rio Tinto 30Y +85

- 10/28 $700M #Ares Capital 10Y +170

- 10/28 $600M #Kimberly-Clark WNG 10Y +48

- 10/28 $500M *Fifth Third 6NC5 +53

EQUITIES: Wall Street Outstrips Mixed European Stocks

- European markets closed more mixed, with the EuroStoxx50, CAC-40 and IBEX-35 finishing with gains of 0.3-0.8%. UK and German indices closed with minor losses. Markets looked through signalling at the ECB press conference that the bank would hold off on rate hikes for the foreseeable future, with short-end rates driving higher and tempering risk appetite.

- This failed to hold back Wall Street equities, however, which traded positively throughout the day as a solid earnings cycle continued to contribute to headline prices. The NASDAQ outperformed, trading higher by over 1% ahead of the close, with consumer discretionary, materials and real estate at the top of the pile. Energy names were the sole decliners, with a pullback in oil prices working against the sector.

- The e-mini S&P cleared the Wednesday high with little effort, but failed to plumb a fresh high at 4590, which remain intact from earlier in the week.

COMMODITIES: Crude Dips, Trades $5 Off Week's High

- WTI and Brent crude futures traded negatively Thursday, with WTI extending the pullback off the week's cycle highs at $85.41/bbl to over $5/bbl. Commodity weakness was notable, coming alongside both USD weakness as well as equity strength, underlining the importance of the build in inventories at yesterday's DoE release as well as the anticipation that Iranian crude could re-enter global energy markets in the coming months. Attention is on the 20-day EMA that intersects at $80.34. A clear breach of this average would signal scope for a deeper pullback and open $78.78, Oct 13 low.

- Gold and silver held their ground more effectively, with precious metals buoyed by the softening greenback and continued bullish focus for spot gold.

- The metal maintains a positive short-term tone despite Tuesday's pullback and remains above the 50-day EMA. Price recently cleared resistance at $1800.6, Oct 14 high and this highlights a short-term bullish theme.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok