Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US TSYS: Retail Sales Beat Estimates, Tsy Yields Climb Higher

Tsys extend session lows late after early see-saw trade. Post-Data Pressure:

Rates reversed early gains/extended lows after better than ests' Retail Sales gained +1.7% (+1.4% est), control group +1.6% M/M (+0.9%).- Major contributors to sales gains: electronics & appliances and building materials & garden, marrying up nicely with the stronger Home Depot /WMT earnings earlier today.

- After some initial two way, yield curves added to Monday's steepening as early long end support evaporated by late morning.

- Large Eurodollar Block: -30,000 EDZ2 99.070 (+0.010), sold through 99.075 post time bid at 111407ET, 99.055 last, sporadic offer picked-up as futures extended lows.

- Early heads up on the lead quarterly Dec'21 futures roll to March'22: rolling has begun with First Notice (when March'22 futures take lead) only two weeks away on November 30. That said, percentage of Dec'21 rolled remains in low single digits.

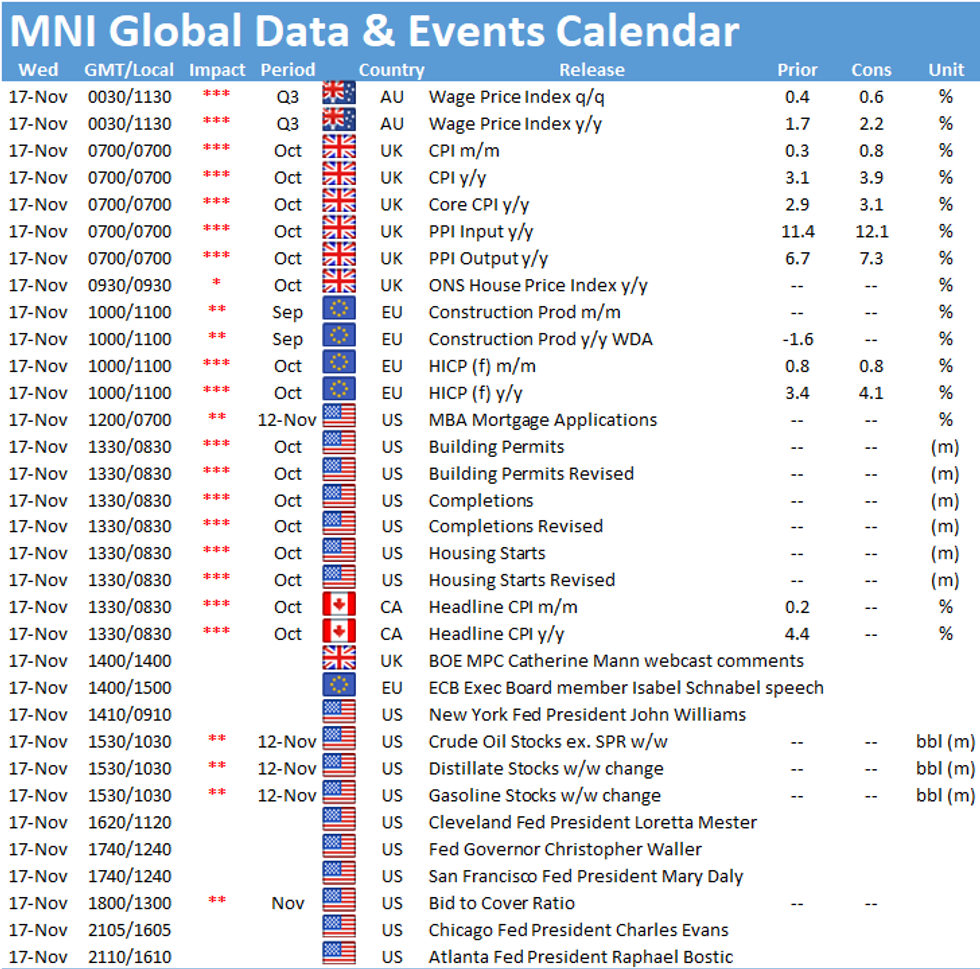

- On tap Wednesday: Building Permits (1.586M rev, 1.630M) and Housing Starts (1.555M, 1.580M). Multiple Fed Speakers and Tsy 20Y Bond Sale.

- Current 2-Yr yield is up 0.2bps at 0.5179%, 5-Yr is up 1.3bps at 1.2653%, 10-Yr is up 1.9bps at 1.6335%, and 30-Yr is up 2.5bps at 2.0207%.

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements

- O/N -0.00075 at 0.07425% (-0.00050/wk)

- 1 Month -0.00225 to 0.08888% (-0.00025/wk)

- 3 Month +0.00212 to 0.16000% (+0.00500/wk) ** Record Low 0.11413% on 9/12/21

- 6 Month +0.00237 to 0.22775% (+0.00175/wk)

- 1 Year +0.00488 to 0.39913% (+0.00062/wk)

- Daily Effective Fed Funds Rate: 0.08% volume: $77B

- Daily Overnight Bank Funding Rate: 0.07% volume: $283B

- Secured Overnight Financing Rate (SOFR): 0.05%, $9568B

- Broad General Collateral Rate (BGCR): 0.05%, $349B

- Tri-Party General Collateral Rate (TGCR): 0.05%, $333B

- (rate, volume levels reflect prior session)

- Tsy 10Y-22.5Y, $1.401B accepted vs. $4.010B submission

- Tsy 4.5Y-7Y, $5.251B accepted vs. $15.666B submission

- Next scheduled purchases

- Thu 11/18 1010-1030ET: Tsy 22.5Y-30Y, appr $1.600B

- Fri 11/19 1010-1030ET: TIPS 1Y-7.5Y, appr $1.775B

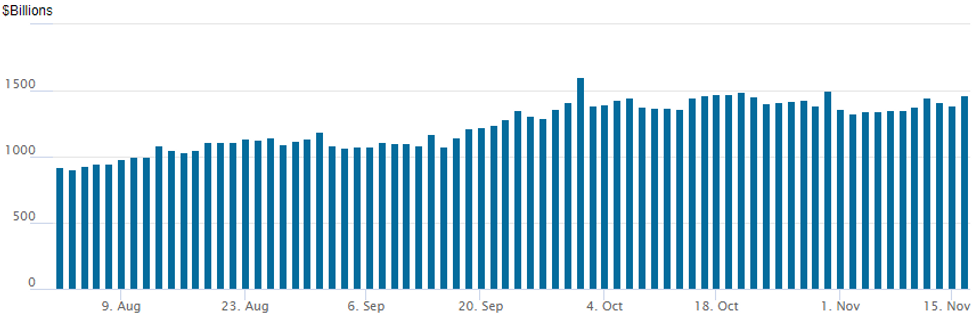

FED Reverse Repo Operation, November High

NY Federal Reserve

NY Fed reverse repo usage climbs to month high of $1,466.857B from 80 counterparties vs. $1,391.657B on Monday. Record high remains at $1,604.881B from Thursday, September 30.

EURODOLLAR/TREASURY OPTIONS SUMMARY

Eurodollar Options:- Update, total 8,000 Blue Dec 98.37 calls, 4.0-4.5

- 2,000 short Dec 99.18/99.31 call spds

- 4,000 Red Dec'22 99.12 puts

- +6,000 Green Dec 98.56/98.75 1x2 call spds, 1.0

- 3,000 Blue Jan 97.75/Blue Mar 97.87 put spds, 8.5

- 2,500 Blue Dec 98.37 calls, 4.5

- 10,000 TYF 132 calls, 6

- 12,400 TYZ 129.75 puts, 15

- 5,500 TYZ 130 puts, 15

- 5,100 FVF 120/121.25 put spds

- 2,000 TYF 127.5/131.5 strangles

- 1,500 TYZ 129.5/130/130.5 put flys

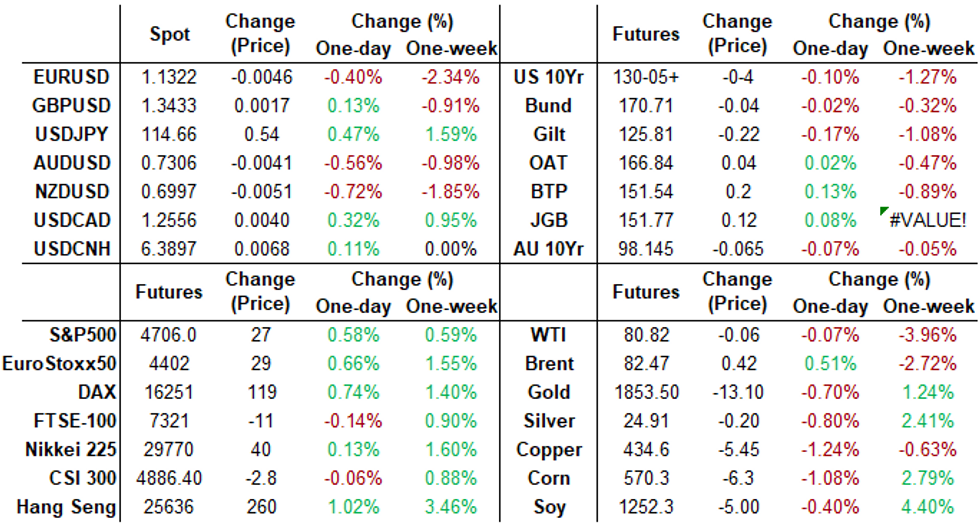

FOREX: Greenback Strength Extends Amid Strong US Data

- The US Dollar extended its strong recent form, emphasised by the dollar index printing a fresh year-to-date high for a fifth consecutive session. The index rose 0.5% during the trading session and the rally was aided by firm US retail sales and production data.

- EURUSD remains pinned to the lows and has weakened another 0.45% on Tuesday, narrowing the gap with touted support at the 1.1305 bear channel base drawn off the Jun 1st high.

- Additionally, supportive price action in USDJPY (+0.50%) has seen the pair creep up to significant horizontal resistance at 11470/73, threatening to break to the best levels since November 2017.

- The worst performers on Tuesday were NZD and AUD, losing 0.75 and 0.6% respectively.

- GBP, however, outperformed after some solid jobs data bolstered bets for a December rate hike, keeping the pound buoyant throughout European hours. This kept EURGBP firmly on the backfoot, and today's sell-off has resulted in a break of support at 0.8463, Nov 3 low. The move lower has exposed the key support at 0.8403, Oct 26 low, where a break would confirm a resumption of the broader downtrend.

- Plenty of action in emerging markets where USDTRY surged to new all-time highs at 10.4426, up well over 3% at one point. Despite a 1.3% reversal from this high print, price action continues to be very aggressive as we approach the CBRT decision on Thursday, with touted local demand exacerbating the price spike. USDZAR and USDCLP also rose over 1.5% amid the continued dollar strength.

- Wednesday's data focus will be on UK and Canadian October CPI data. Markets will also be alert for crude oil inventories and another slew of Fed speakers throughout the US session.

FX: Expiries for Nov17 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1390(E914mln), $1.1450-70(E735mln), $1.1490-05(E1.9bln)

- USD/JPY: Y115.00($558mln)

- EUR/GBP: Gbp0.8445(E839mln)

- AUD/USD: $0.7300(A$722mln)

- USD/CAD: C$1.2500($551mln), C$1.2540-50($905mln)

EQUITIES: Solid Retail Sales, Earnings Drives Indices Higher

- Wall Street traded uniformly higher Tuesday, with all three major indices notching up gains of 0.5% or more. The e-mini S&P traded just shy of Nov 8th's 4707, a break above which opens new alltime highs of 4711.75 printed a few weeks ago.

- Consumer discretionary and tech names led gains across Wall Street, with a solid contribution from Home Depot after their earnings, which showed comparable store sales coming in well ahead of expectations. Their shares traded with gains of as much as 6% ahead of the close.

- At the other end of the table, Walmart traded poorly as their report showed their gross profit rate took a hit of around 12bps - reflecting increased costs across supply chains, which had already received a boost from advertising.

- Across Europe, the picture was mixed-to-positive, with Germany's DAX making gains while the UK's FTSE-100 and Spain's IBEX-35 lagged.

COMMODITIES: Crude Recovers Off Lows While Gold Loses Shine

- WTI and Brent crude futures came under pressure in early NY hours, pressing prices back toward yesterday's lows before stabilising. This rejection of the break below $80/bbl in WTI futures keeps the focus pointed higher, with key resistance and the bull trigger is at $85.41, Oct 25 high. A break of this hurdle is required to confirm a resumption of the uptrend and resume the bullish price sequence of higher highs and higher lows. This would open $87.45, a Fibonacci projection.

- Gold traded poorly, reversing much of the early outperformance as the USD Index managed to print a fresh YTD high for a fifth consecutive session. $1845.29 - the Nov 12 low - marks first support, with a break below exposing $1822.4, the Nov 10 low.

- Focus Wednesday turns to the DoE crude inventories data, with markets expecting a build of just shy of 900k barrels for the headline.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok