Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US TSYS: Fall in Love W/ FI on Valentine's Day, Give the Gift of Risk Mitigation

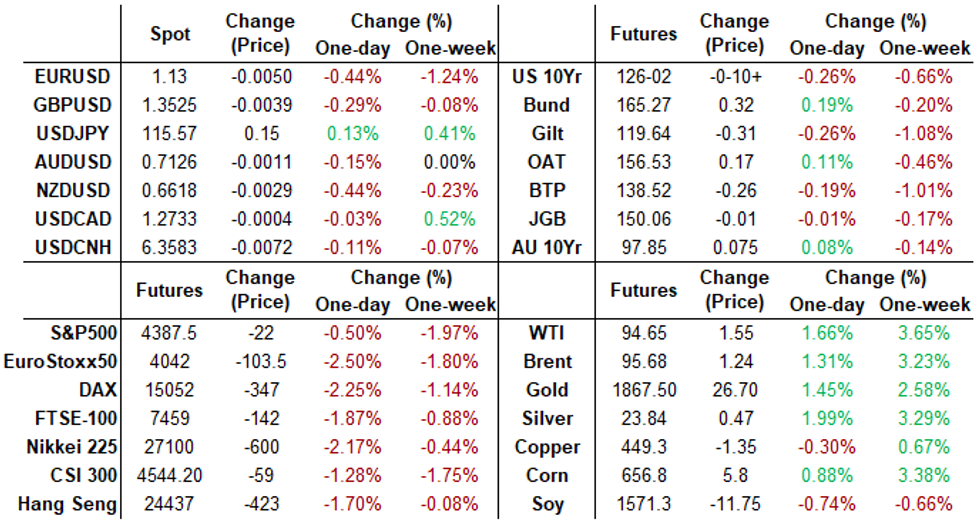

Rates finished weaker Monday, lower half of the range after making an attempt to reverse losses on late chatter concerning Russia/Ukraine tensions.- While markets reacted positively to early Russia official Lavrov comments over keeping negotiations open re: Russia/Ukraine tensions, late headlines purporting satellite images of Russia troop movements closer to Ukraine border and headline that Ukraine Pres Zelensky told Russia invasion would proceed Wed (apparently tied to mistranslated comments made in a speech hours prior) spurred risk-off moves.

- Markets remain skittish over Russia/Ukraine headlines -- more apt to spur a tail-event move than Fed speak after StL Fed Pres Bullard reprised his hawkish stance on CNBC Monday morning after green-lighting 50bps March lift-off and suggesting potential for off-meeting move.

- Tsy futures extending session lows as StL Fed Bullard reiterates stance on higher/faster rate hikes to address growing inflation, would like to see 100bp in hikes by July, Fed not moving fast enough. Bullard Wants balance sheet run-off in second quarter. On supply chain drag, Bullard said a feed-back loop may last into 2023.

- Active early trade, bearish option hedging as underlying rates react to StL Fed Bullard reiterating hardline stance on rising inflation and cooling geopol headlines re: Russia/Ukraine. Call skew firmed briefly on second half bounce in underlying.

- Late: 2-Yr yield is up 7.9bps at 1.5785%, 5-Yr is up 5.2bps at 1.9063%, 10-Yr is up 4.9bps at 1.9858%, and 30-Yr is up 5.2bps at 2.2905%.

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements:

- O/N -0.00172 at 0.07671% (+0.00143 total last wk)

- 1 Month -0.06543 to 0.12571% (+0.07585 total last wk)

- 3 Month -0.04786 to 0.45857% (+0.16743 total last wk) ** Record Low 0.11413% on 9/12/21

- 6 Month -0.04657 to 0.79386% (+0.28500 total last wk)

- 1 Year -0.07015 to 1.32214% (+0.39329 total last wk)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 0.08% volume: $67B

- Daily Overnight Bank Funding Rate: 0.07% volume: $251B

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 0.05%, $903B

- Broad General Collateral Rate (BGCR): 0.05%, $338B

- Tri-Party General Collateral Rate (TGCR): 0.05%, $329B

- (rate, volume levels reflect prior session)

NY Fed updated purchase schedule: The Desk plans to purchase approximately $20 billion over the monthly period from 2/14/22 to 3/11/22 -- in effect ending intermeeting move. Note: Eurodollar lead quarterly EDH2 +0.030 at 99.31 as 50bp hike odds fall below 50%.

- Tue 02/15 1010-1030ET: Tsy 4.5Y-7Y, appr $3.225B vs. $6.025B prior

- Thu 02/17 1010-1030ET: Tsy 10Y-22.5Y, appr $1.625B steady

- Tue 02/22 1010-1030ET: TIPS 1Y-7.5Y, appr $1.025B vs. $2.025B prior

- Thu 02/24 1010-1030ET: Tsy 0Y-22.5Y, appr $6.225B steady

- Tue 03/01 1100-1120ET: TIPS 7.5Y-30Y, appr $0.625B vs. $1.225B prior

- Thu 03/03 1100-1120ET: Tsy 7Y-10Y, appr $1.625B vs. $3.225 prior

- Tue 03/08 1010-1030ET: Tsy 22.5Y-30Y, appr $1.825B steady

- Thu 03/09 1010-1030ET: Tsy 2.25Y-4.5Y, appr $4.025B

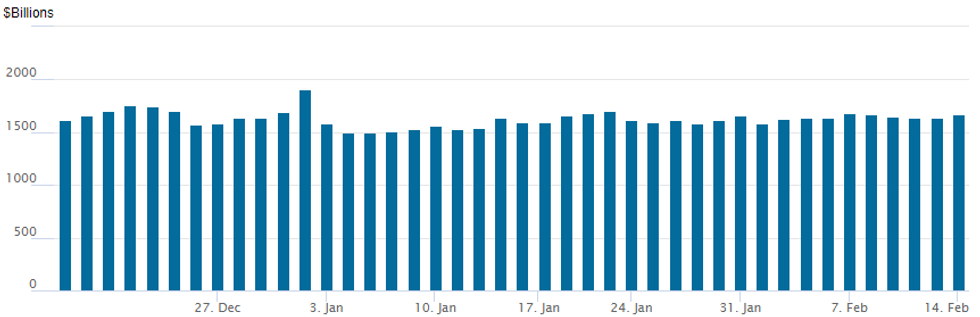

FED Reverse Repo Operation

NY Federal Reserve/MNI

NY Fed reverse repo usage climbs to $1,666.232B w/ 80 counterparties vs. $1,635.826B Friday -- remains well off all-time high of $1,904.582B on Friday, December 31.

EURODOLLAR/SOFR/TREASURY OPTIONS SUMMARY

Eurodollar Options:- -10,000 Sep 97.87/98.25 put spds, 10.5 ref: 98.315-.32

- +10,000 Jun 98.62/99.12 2x1 put spds from 5.5-7.0

- -10,000 Green Mar 98.00/98.12/98.18.7/98.37 broken call condors, 1.0

- 7,500 Green Jun 97.50/97.75 put spds

- 2,000 Green Apr 97.25/97.37/97.50/97.62 put condors

- More SOFR Straddles

- 10,000 SFRM3 98.00 straddles, 100.0 after 10k Blocked at 98.0 earlier (30k blocked Fr from 96-97)

- Overnight trade

- +5,000 Sep 98.25/98.50/98.75 put flys on 6x11x5 ratio, 3.0 net, ref 98.35

- -7,000 Blue Jun 97.25/97.75 put spds, 13.5 vs. 97.88/0.25%

- -5,000 May 98.62 calls vs. 10,000 Jun 99.12 calls, 11.0 net

- +3,000 Dec 97.75 puts, 33.0 vs. 98.02/0.40%

- 10,000 TYH 127 calls, 7 ref 125-26.5 pushes total volume near 70k

- Update +10,000 TYK 122/123/124 put flys, 5

- +20,000 TYJ 124.5 puts, 35 vs. 125-24

- +7,000 TYM 124 puts, 52

- 30,257 TYH/TYJ 127 call spds, 26

- +2,500 TYM 123/124 put spds, 23.0 vs. 126-05.5/0.12%

- 3,500 FVJ 118 calls, 24

- Overnight trade

- +3,000 TYH 124/125 put spds, 12

- +3,500 TYH 128.25 calls, 2

EGBs-GILTS CASH CLOSE: Geopolitical Reversals

Bunds outperformed Gilts Monday in a session dominated by geopolitical headlines.

- The open was met with risk-selling and core FI buying on Russia-Ukraine conflict fears, but this reversed almost completely in the afternoon as Russia indicated it saw a "way forward" on talks. Later, Interfax reported that Ukraine saw no full-scale Russian attack in the coming days, and yields finished near their highs.

- The standout move was at the UK short end, with 2Y yields at the highest since Feb 2011 - close attention on UK jobs data tomorrow, inflation Weds.

- Periphery spreads widened sharply on the open, and didn't come fully back despite the recovery in broader risk sentiment.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is down 3.7bps at -0.361%, 5-Yr is down 4bps at 0.044%, 10-Yr is down 1.4bps at 0.283%, and 30-Yr is down 0.2bps at 0.494%.

- UK: The 2-Yr yield is up 9.6bps at 1.51%, 5-Yr is up 6.7bps at 1.504%, 10-Yr is up 4.4bps at 1.589%, and 30-Yr is up 2.9bps at 1.646%.

- Italian BTP spread up 3.4bps at 169bps / Greek up 3bps at 237.5bps

EGB Options: Large Bearish Bund Trade (And Other Downside)

Monday's Europe rates / bond options flow included:

- RXH2 164.50p, sold at 20 in 6k

- RXH2 166/169.50cs 1x2, bought for 38 in 1.5k

- RXH2 164.5/164.0/163.0/162.5 put condor bought for 8 in 2k

- RXJ2 150p, bought for 5 in 15k

- RXJ2 166c, bought for 52.5 in 3.6k

- RXJ2 159/157ps, sold at 17.5 in 2.5k

- RXJ2 158/156ps, sold at 12 and 11 in 5.5k

- RXJ2 162/161ps, sold at 35 in 6k, and at 32 in 1.5k

- OEH2 129.75/129.25ps, bought for 11 in 10k

- DUH2 111.80c, sold at 3.25 in 5k

- DUH2 112.10/112/111.90, bought for half in 1.5k

- DUJ2 113.30/111.10ps, bought for 9 in 12k

- ERN2 100.12/100.25/100.37c ladder, bought for 3.5 in 10k

- 0RM2 99.50/99.37ps sold at 6.5 in 11.25k

FOREX: Greenback Firms Amid Shaky Sentiment, EURUSD Back Below 1.1300

- The US dollar remained well supported throughout Monday as risk sentiment deteriorated over mounting tensions regarding Ukraine. The dollar index edged slowly higher from the open, registering a 0.3% advance on Monday. Currencies, however, remained the sideshow to volatile trading in both equity and bond markets.

- Both EUR (-0.45%) and NZD (-0.45%) exhibited the most notable weakness, suffering from the dollar strength.

- EURUSD in particular continues to grind lower, spending the latter half of the session back below 1.13 and in close proximity to the ECB-day lows at 1.1268. A key short-term resistance has now been defined at Thursday’s high of 1.1495 and broader moving average signals still suggest the medium-term trend is down. Key short-term support has been breached through 1.1320, the top of the former channel.

- Despite the shaky risk backdrop, emerging market currencies seem to be trading resiliently with roughly half percent advances in RUB, ZAR and MXN.

- A busier data calendar on Tuesday with RBA minutes overnight and then UK unemployment data followed by German ZEW sentiment figures. US PPI and Empire State Manufacturing headlines the US schedule.

- Additionally, German Cahancellor Scholz is scheduled to visit Moscow on Tuesday, where he plans to hold talks with Russian President Vladimir Putin.

FX: Expiries for Feb15 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1295-00(E691mln), $1.1340-50(E981mln), $1.1395-00(E617mln)

- USD/JPY: Y114.85-00($900mln), Y115.45-50($650mln), Y115.70-75($800mln), Y115.90-00($1.3bln)

- USD/CAD: C$1.2695-00($2.3bln)

EQUITIES: US Sell-Off Abates as Bounce in Tech Steadies Indices

- Following the sharply negative Wall Street close on Friday, it was a particularly poor start for Asia-Pac and European indices. This was the same case for the cash open in the US, but sentiment appeared to find a floor and recovered after the London close. Tech and growth names led the bounce, with heavy hitters including Netflix, Amazon and Tesla all trading well in a reversal of recent weakness.

- The bottom in stocks coincided with a statement from Russian foreign minister Lavrov, who saw grounds for further discussions between Russia and the West - a proposal which Russian President Putin duly accepted. The signs of progress helped markets recover off bottom, with the threat of invasion in eastern Ukraine seen tapering off in the very near-term.

- The e-mini S&P failed to hold above the 50-day EMA - at 4555.49. This average still represents a firm resistance and a clear breach of it is required to suggest scope for a stronger rally that would open 4671.75 initially, Jan 18 high. The Jan 10 candle pattern is a bearish engulfing reversal, signalling a potential top and the recent move lower reinforces the pattern. A deeper pullback would expose 4212.75.

COMMODITIES: Russia-Ukraine Fears Stoke Oil, Gold

- An intensification of Russian aggression fears has pushed crude oil prices up circa 1.5% today.

- The latest move has been dialled back as markets take in the fact Zelensky might have been sarcastic on headlines that Russia could attack on Wed, but risk-off sentiment remains after the US earlier closed its Kyiv embassy.

- Earlier, EU Coordinator Borrell says the JCPOA deal is “in sight” re the Iranian nuclear deal, which could boost oil supply.

- WTI is +1.6% at $94.64 having earlier cleared the second resistance level of $95.7 (2.764 proj of Dec 2-9-20 price swing). Gains have been heavily loaded in front-end contracts.

- Brent is +1.2% at $95.60, resistance remains at $97.36 (2.618 proj of the same price swing) with support at $89.93 (Feb 8 low).

- Gold is up strongly, +0.8% at $1872.8. It touched a high of $1874.17, clearing two resistance levels of $1871.0 (Nov 18 high) and next opening key resistance of $1877.2 (Nov 16 high).

Tuesday Data Calendar

| Date | GMT/Local | Impact | Flag | Country | Event |

| 15/02/2022 | 2350/0850 | *** |  | JP | GDP (p) |

| 15/02/2022 | 0700/0700 | *** |  | UK | Labour Market Survey |

| 15/02/2022 | 0800/0900 | *** |  | ES | HICP (f) |

| 15/02/2022 | 1000/1000 | ** | | UK | Gilt Outright Auction Result |

| 15/02/2022 | 1000/1100 | *** |  | DE | ZEW Current Expectations Index |

| 15/02/2022 | 1000/1100 | * |  | EU | employment |

| 15/02/2022 | 1000/1100 | *** | | EU | GDP (p) |

| 15/02/2022 | 1000/1100 | * | | EU | trade balance |

| 15/02/2022 | 1000/1100 | *** | | DE | ZEW Current Conditions Index |

| 15/02/2022 | 1315/0815 | ** |  | CA | CMHC Housing Starts |

| 15/02/2022 | 1330/0830 | *** |  | US | PPI |

| 15/02/2022 | 1330/0830 | ** | | US | Empire State Manufacturing Survey |

| 15/02/2022 | 1355/0855 | ** | | US | Redbook Retail Sales Index |

| 15/02/2022 | 1400/0900 | * | | CA | Home Sales – CREA (Canadian real estate association) |

| 15/02/2022 | 1630/1130 | ** | | US | NY Fed Weekly Economic Index |

| 15/02/2022 | 1915/1415 | | US | Senate Banking Committee votes on Federal Reserve nominees | |

| 15/02/2022 | 2100/1600 | ** | | US | TICS |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.