Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US TSYS: Hawkish Hike Expectations Evaporate on Flat July Inflation

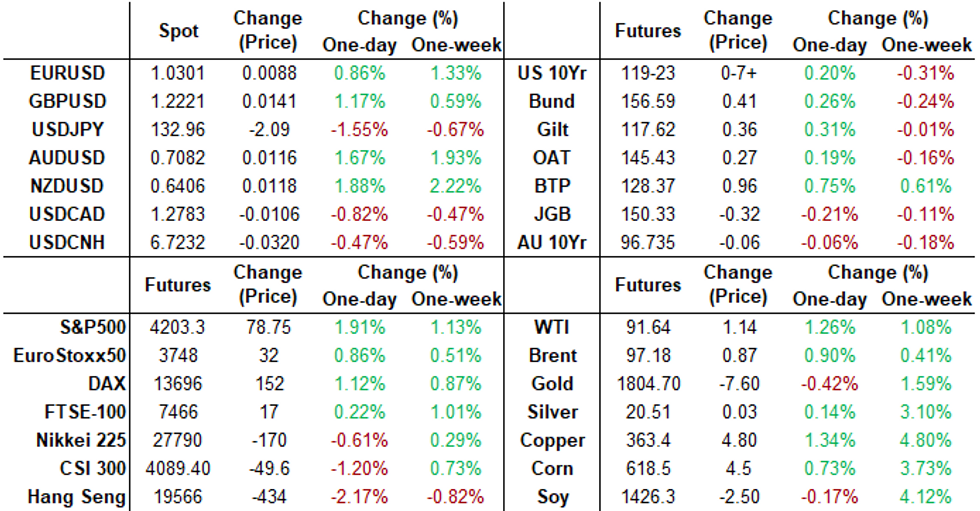

Tsy futures trading mixed after the bell, yield curves steeper but off highs on exceptionally wide range. Tsys initially surged across the board after flat July CPI read (0.2% est vs. 1.3% in June), Core 0.3%; Y/Y 8.5%, Core Y/Y 5.9%.

- Markets still have a lot of data to absorb between now and September 16, the next FOMC policy annc. Nevertheless, Bonds quickly pared gains after the release/traded weaker from midday on while short end continued to outperform as Sep rate hike expectations snapped from strong 75bp conviction to 50bp (off immediate high of 96.76, Sep Eurodollar futures trading 96.63 +0.075 after the bell).

- Appearing at Aspen Economic Strategy Group event, MN Fed Kashkari said the Fed needs to keep pressing ahead with rate hikes even after today's downside inflation surprise. "It doesn't change my path" laid out in June calling for a policy rate of 3.9% at the end of this year and 4.4% at the end of next year, he said. That remains true even with a recession being possible in the near term, he said.

- Meanwhile, Tsy futures gained slightly after strong $35B 10Y note auction (91282CFF3) stopped through: 2.755% high yield vs. 2.762% WI; 2.53x bid-to-cover vs. last month's 2.34x. Indirect take-up climbs to 74.52% vs. last month's 61.33% high; direct bidder take-up recedes to 15.56 from 17.97%, primary dealer take-up falls to 9.92% vs. 20.07%.

- Cross asset update: Stocks surged post-data (SPX eminis at 4205.0 +82.50); Spot Gold turned weaker at 1789.83 -4.46; Crude firmer (WTI +1.11 at 91.61).

- Data on tap for Thursday: PPI Final Demand MoM (0.3% est vs. 1.1% prior), weekly claims (265k est vs. 260k prior), continuing claims (1.45M vs. 1.416M prior).

- Currently, 2-Yr yield is down 4.9bps at 3.2203%, 5-Yr is down 3.6bps at 2.925%, 10-Yr is up 0.7bps at 2.7846%, and 30-Yr is up 4.5bps at 3.0343%.

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements

- O/N -0.00171 to 2.31629% (+0.00429/wk)

- 1M +0.02029 to 2.40043% (+0.03100/wk)

- 3M +0.00171 to 2.92271% (+0.05600/wk) * / **

- 6M -0.00386 to 3.54657% (+0.12100/wk)

- 12M +0.00728 to 3.99814% (+0.13828/wk)

- * Record Low 0.11413% on 9/12/21; ** New 24Y high: 2.91157% on 8/8/22

- Daily Effective Fed Funds Rate: 2.33% volume: $90B

- Daily Overnight Bank Funding Rate: 2.32% volume: $283B

- Secured Overnight Financing Rate (SOFR): 2.29%, $947B

- Broad General Collateral Rate (BGCR): 2.26%, $386B

- Tri-Party General Collateral Rate (TGCR): 2.26%, $377B

- (rate, volume levels reflect prior session)

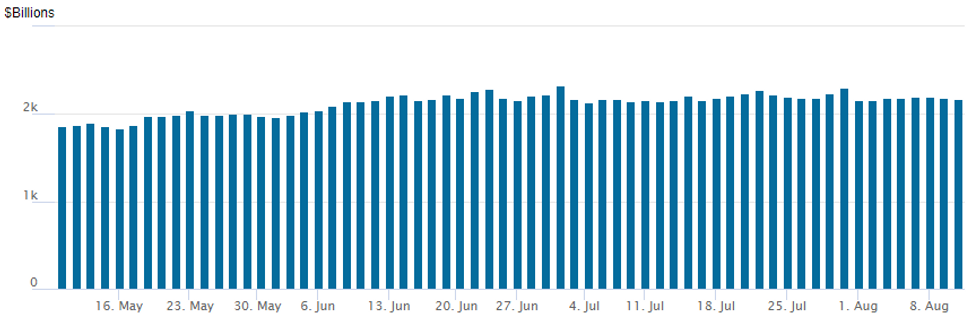

FED Reverse Repo Operation

NY Federal Reserve/MNI

NY Fed reverse repo usage recedes to $2,177.646B w/ 96 counterparties vs. $2,186.568B prior session. Record high still stands at $2,329.743B from Thursday June 30.

EURODOLLAR/SOFR/TREASURY OPTIONS SUMMARY

Option trades remained decidedly bearish despite the front-end lead, curve steepening rally in underlying rate futures after July CPI read of 0.0%, Core 0.3%; Y/Y 8.5%, Core Y/Y 5.9%. Initial relief rally across the board while yield curves bull steepen as Sep rate hike expectations snap from strong 75bp conviction to 50bp (off immediate high of 96.76, Sep Eurodollar futures continue to trade around 96.65-.655 +0.100).- Despite the softer inflation metric, considering the amount of time and data yet to come before the Sep 16 FOMC - put buyers faded the short end rally. Salient trade some up the day: buyer of 20,000 Sep SOFR 96.68/96.75 put spreads at 1.0 later in the second half vs. 96.885-.890/0.05% delta. Meanwhile, Eurodollar options included a buy of 20,000 Nov 95.50/95.75 put spds at 4.5. Treasury options proved more mixed: two-way in 10Y and 5Y puts.

- +20,000 SFRU2 96.68/96.75 put spds, 1.0 vs. 96.885-.89/0.05%

- Block, 4,000 SFRQ2 96.75/96.87 put spds, 1.0 ref 96.905

- 5,000 SFRH3 95.50/96.00 put spds 11.5

- 7,500 SFRM3 95.75/96.25 put spds, 15.0

- Block, 4,000 short Aug SOFR 97.25/98.00 call spds 14.0 over 95.75 puts

- Block, 5,000 SFRH3 95.75/96.12 put spds, 11.0

- -20,000 SFRZ2 97.00/97.25 call spds, 4.0-4.25

- +5,000 SFRU2 97.00/97..06/97.12 call flys 0.5, add to +40k late Tue

- 4,000 Sep 98.50/98.62 put spds

- +5,000 short Oct 96.00/96.12 put spds, 2

- +20,000 Nov 95.50/95.75 put spds, 4.5

- +5,000 TYU 120 calls, 54 vs. 120-07/0.54%

- update, -25,000 FVV 109/110 put spds, 4.5

- 2,000 TYU 120.25 calls, 51 ref 120-05.5

- 2,000 TYV 123/124 call spds, 8 ref 120-12.5

- 3,800 FVU 112.5 puts, 21 ref 112-29.25

- -15,000 TYU 119 puts, mostly 19-21

- over 27,000 FVV 111.25 puts right on data release 29.5-31.5

- 2,500 TYZ 123/124 call spds vs. 5,000 TYZ 114/116 put spds

EGBs-GILTS CASH CLOSE: Post-US CPI Rally Fades, But BTPs Outperform

The German curve bull steepened Wednesday with the UK twist flattening as a softer-than-expected US July inflation print pulled down global yields.

- Rates retraced somewhat from session lows immediately after the US CPI release.

- Overall though curves held their re-steepening (UK 2s10s finished above zero after inverting earlier in the session) and yields finished lower with the exception of the UK short-end.

- BTPs outperformed on the more dovish central bank tightening outlook and risk-on tone, but bucking the broader trend were GGBs whose spreads widened for another session.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany:

- Germany: The 2-Yr yield is down 5.9bps at 0.546%, 5-Yr is down 3.2bps at 0.656%, 10-Yr is down 3.3bps at 0.888%, and 30-Yr is down 2.7bps at 1.127%.

- UK: The 2-Yr yield is up 2bps at 1.947%, 5-Yr is down 2bps at 1.8%, 10-Yr is down 2bps at 1.951%, and 30-Yr is down 0.9bps at 2.336%.

- Italian BTP spread down 2.7bps at 211.3bps / Greek up 2.5bps at 230.8bps

EGB Options: A Few German Bond Spreads Bought And Euribor Fly Selling

Wednesday's Europe rates and bond options flow included:

- OEU2 128/129 call spread bought for 16.5 in 4k

- RXV2 143.0/140.5 1x1.5 put spread bought for flat in 4k

- ERZ2 99.37/99.12/99.00 broken p fly, 1x3x2, sold at 2.75 in 5k

FOREX: Greenback Plummets Following Lower July US CPI

- The USD index is seen 1.1% lower on Wednesday following the negative surprise for July US inflation data. The month-on-month headline unrounded was negative for the first time since May 2020 and the M/m core unrounded was the lowest since Sept 2021.

- The kneejerk reaction was a significantly lower greenback across the board, however, the main beneficiary in the immediate aftermath was the Japanese Yen. USDJPY crashed 230 pips to 132.69 shortly after the release and despite a sharp pullback to 133.30, pressure on the pair extended over the next few hours all the way down to 132.03, comfortably below the lows registered prior to Friday’s jobs numbers.

- In similar vein, EURUSD saw immediately strength and finally broke out of the 1.0100-1.0300 range it had been consolidating in for the past sixteen sessions. Key channel top resistance was briefly breached above 1.0352 coinciding with the horizontal breakdown area between 1.0341/50.

- Unyielding support for US equity benchmarks continued to underpin the likes of AUD and NZD who look set to register gains of close to 2% as we approach the APAC crossover.

- Worth noting there has been a decent bounce in the greenback in late trade as Fed rhetoric from both Evans and Kashkari hinted that today’s data should not alter their expected trajectories for rates. USDJPY relief rally was supported by US 10-yr yields rising back to pre-CPI announcement levels with the curve remaining steeper. The pair now roughly a full point off the day’s lows at 132.03.

- Similar EURUSD selling sees the pair trade back to the 1.0300 mark, however, with major equities remaining close to the highs, there has been less of a pullback in antipodean FX and CAD that remain closer to their best levels of the day against the greenback.

- Bank Holiday in Japan on Thursday with little data due throughout the APAC session. Less significant PPI and jobless claims highlight the US docket tomorrow.

FX: Expiries for Aug11 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0097-05(E1.8bln), $1.0125(E607mln), $1.0200(E700mln), $1.0235(E524mln), $1.0300(E581mln)

- USD/JPY: Y134.25($685mln), Y134.97-00($1.2bln), Y135.15-35($941mln)

- GBP/USD: $1.2000(Gbp552mln), $1.2150-65(Gbp1.1bln)

- EUR/GBP: Gbp0.8350(E780mln), Gbp0.8650(E716mln)

- AUD/USD: $0.6980-00(A$1.6bln)

- USD/CAD: C$1.3200($825mln)

- USD/CNY: Cny6.7000($1.2bln)

Late Equity Roundup: Holding Near Highs, Materials Sector Outperforms

Stocks remain stronger in late trade -- holding narrow range ever since gap bid following July CPI read - flat for the month, Core inflation climbed 0.3% MoM, 5.9% YoY. Currently, SPX eminis trades +78.5 (1.9%) at 4203.25; DJIA +470.82 (1.44%) at 33248.26; Nasdaq +326.1 (2.6%) at 12820.61.

- SPX leading/lagging sectors: Materials sector outperformed (+3.24%) lead by Albermarle (ALB) +5.81%, PPG +5.71%, Sherwin-Williams (SHW) +5.25%; Consumer Discretionary gained late (+2.79%) w/autos edging past consumer durables, Communication Services +2.75% lead by interactive media and services providers: Netflix (NFLX) +6.10%, Meta +5.74%, Dish +4.01%. Laggers: Utilities (+0.04%), Consumer Staples (+0.56%), after three consecutive session gains, Energy sector slows (+0.58%).

- Dow Industrials Leaders/Laggers: Goldman Sachs (GS) +12.77 at 349.39, Microsoft (MSFT) bounces +6.39 at 288.69, Home Depot (HD) +5.59 at 310.80. Laggers: Merck (MRK) -1.26 at 88.26, United Health (UNH) -1.01 at 536.25, JNJ -0.58 at 169.60.

E-MINI S&P (U2): Resumes Its Uptrend

- RES 4: 4400.00 Round number resistance

- RES 3: 4345.75 2.00 proj of the Jun 17 - 28 - Jul 14 price swing

- RES 2: 4306.50 High May 4

- RES 1: 4204.75 High May 31 and a key resistance

- PRICE: 4200.00 @ 1500ET Aug 10

- SUP 1: 4080.50 Low Aug 2

- SUP 2: 4008.43/3913.25 50-day EMA / Low Jul 26 and a key support

- SUP 3: 3820.25 Low Jul 18

- SUP 4: 3723.75 Low Jul 14

S&P E-Minis have traded higher today and delivered a fresh trend high print of 4201.50. This reinforces short-term bullish conditions. Continued gains would also maintain the positive price sequence of higher highs and higher lows. The focus is on 4204.75 next, May 31 high and the next key resistance. On the downside, initial trend support is at 4080.50, the Aug 2 low. The 50-day EMA intersects at 4008.43 - a key support.

COMMODITIES: Oil Whipsaws As US Gasoline Demand Wins Out

- Crude oil is currently up more than 1% on a day of whipsawing. Bearish price drivers included oil flows via Druzhba and Iraq production coming in just above its OPEC+ quota of 4.580mbpd in Jul at 4.584mbpd (+69k from June). That was before EIA data showed a much larger than expected drawdown in US gasoline stockpiles (-4.978M vs -1.152M) for the biggest weekly drop in 10 months, which seemed to carry more weight than an also large surprise build in crude inventories on a strong build in production and an unexpected fall in crude exports.

- Focus ahead on global supply and demand balances from OPEC and IEA.

- In Germany, low Rhine water levels threaten the ceasing of diesel and coal transport, with the marker at Kaub forecast to drop to the critical depth of 40cm early on Aug. 12, and set to continue dropping, to 37cm the following day.

- WTI is +1.44% at $91.79, pushing back against a doji candle pattern highlighting the possible end of the recent 3-day bounce. Resistance is eyed at $94.67 (20-day EMA) whilst support is seen at $87.01 (Aug 5 low).

- Brent is +1.07% at $97.34, moving closer to initial resistance eyed at $99.30 (20-day EMA).

- Gold is -0.25% at $1789.68, down from a post-CPI snap reaction of $1807.93, temporarily clearing trendline resistance at $1794.6 to leaving resistance at $1829.8 (38.2% retracement of Mar 8 – Jul 21 bear leg).

Thursday Data Calendar

| Date | GMT/Local | Impact | Flag | Country | Event |

| 11/08/2022 | 2301/0001 | * |  | UK | RICS House Prices |

| 11/08/2022 | 1230/0830 | ** |  | US | Jobless Claims |

| 11/08/2022 | 1230/0830 | *** | | US | PPI |

| 11/08/2022 | 1230/0830 | ** | | US | WASDE Weekly Import/Export |

| 11/08/2022 | 1430/1030 | ** | | US | Natural Gas Stocks |

| 11/08/2022 | 1530/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 11/08/2022 | 1530/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 11/08/2022 | 1700/1300 | *** | | US | US Treasury Auction Result for 30 Year Bond |

| 11/08/2022 | 1800/1400 | *** |  | MX | Mexico Interest Rate |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.