Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

HIGHLIGHTS

Atlanta Fed Fourth-Quarter GDP Growth Estimate Increases (3.6% from 2.6%)

ECB'S LAGARDE: THERE'S STILL A WAY TO GO ON RATES, Bbg

BOE RAISES KEY INTEREST RATE BY 75 BASIS POINTS TO 3%

Key links: MNI: BOE MPC Hikes 75bps, Says Market Rate Peak Was Too High / MNI BOE WATCH: Further Hikes Likely, Market Peak Overblown / MNI INTERVIEW: ECB Likely To Keep Hiking Beyond March – Kazaks / MNI Fed Review - Nov 2022: Destination Unknown

US TSYS: Focus On Friday's October Employment Data

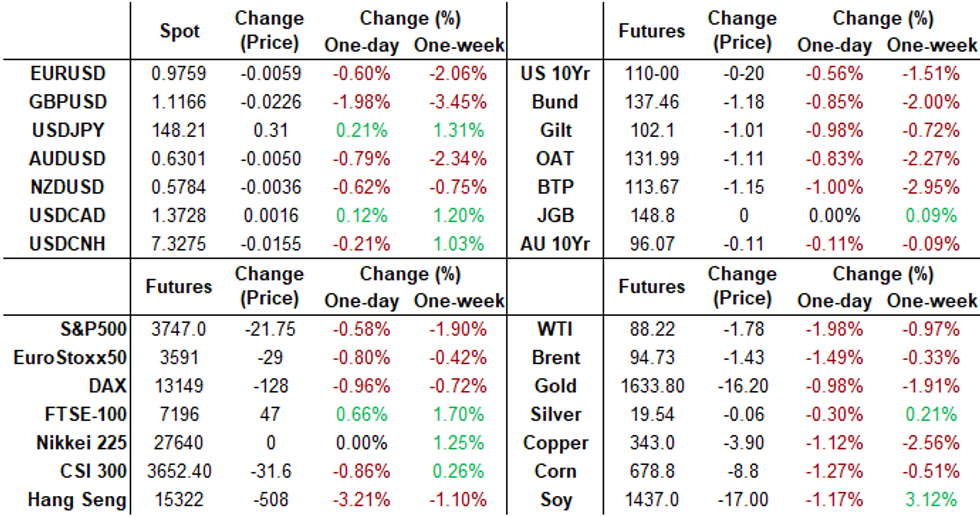

Tsy futures weaker after the bell but near late session highs, yield curves near inverted lows (2s10s currently -5.411 at -57.745). Generally quiet second half as markets await Friday's October employment data.

- Tsys opened weaker, adding to Wed's post-FOMC action after Chairman Powell's hawkish rebuttal to the expected 75bp rate hike while short end back to gradually pricing in an unprecedented fifth 75bp hike in December.

- Little react to expected BOE 75bp hike earlier while Tsys extended lows after small pick-up in continuing claims to 1.485M (1.450M est), weekly claims little softer at 218k vs. 220k est. Unit Labor Costs lower than exp: 3.5% vs. 4.0% est.

- Tsys bounced off midmorning lows (30YY tapped 4.2298%) after weaker than expected ISM Non-Manufacturing at 54.4 vs expected 55.3 (56.7 prior), ending for consecutive months of stronger data.

- Fed out of media blackout Friday: Boston Fed Pres Collins on economy/policy outlook at a Brookings conf (text and Q&A expected) at 1000ET, while CNBC expected to interview Richmond Fed Pres Barkin at same time.

- Currently, 2-Yr yield is up 7.5bps at 4.695%, 5-Yr is up 4.1bps at 4.35%, 10-Yr is up 2.1bps at 4.1217%, and 30-Yr is up 1.1bps at 4.1512%.

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements:

- O/N +0.75015 to 3.81329% (+0.74943/wk)

- 1M +0.01086 to 3.84657% (+0.07886/wk)

- 3M +0.02314 to 4.53157% (+0.09200/wk) * / **

- 6M +0.02658 to 4.99729% (+0.06643/wk)

- 12M +0.11757 to 5.65357% (+0.28457/wk)

- * Record Low 0.11413% on 9/12/21; ** New 14Y high: 4.53157% on 11/3/22

- Daily Effective Fed Funds Rate: 3.08% volume: $108B

- Daily Overnight Bank Funding Rate: 3.07% volume: $289B

- Secured Overnight Financing Rate (SOFR): 3.05%, $1.021T

- Broad General Collateral Rate (BGCR): 3.01%, $405B

- Tri-Party General Collateral Rate (TGCR): 3.00%, $391B

- (rate, volume levels reflect prior session)

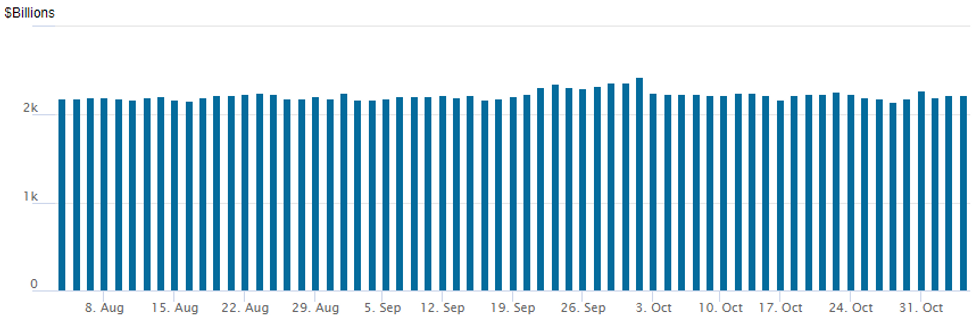

FED Reverse Repo Operation

NY Federal Reserve/MNI

NY Fed reverse repo usage recedes to $2,219.791B w/ 105 counterparties vs. $2,229.861B in the prior session. Prior record high stands at $2,425.910B on Friday, September 30.

EURODOLLAR/SOFR/TREASURY OPTIONS SUMMARY

Option volumes surged Thursday, better put flow on net as Tsys opened weaker, adding to Wed's post-FOMC action after Chairman Powell's hawkish rebuttal to the expected 75bp rate hike.

- Broad based downside positioning as short end rates resumed gradually pricing in an unprecedented fifth 75bp hike in December. One 12-leg strip had paper selling 5,000 SFRH3/SFRM3/SFRU3 94.87/95.25/95.50/95.87 put condors for a total of 25.0. Other longer plays rolled out (expiry) and down (in strike) such as buyer of 10Y option package: TYZ 109/TYH 107 put spds, 24 March over. Salient trade:

- SOFR Options:

- Block, -20,000 SFRM3 95.25/95.75 call spds, 9.5 ref 94.87-.875

- Block, 5,000 SFRG3 94.50/94.75 put spds, 7.0 ref 94.925 - add

- -5,000 SFRH3/SFRM3/SFRU3 94.87/95.25/95.50/95.87 put condor strips, 25.0

- Block, 10,000 SFRM3 94.50/94.75/95.00 put flys, 3.5-4.0 ref 94.86

- Block, 10,500 SFRM3 95.12/95.25/95.50 broken put flys, 10.0 ref 94.855-.86

- Block, 10,000 SFRG3 94.50/94.75 put spds, 8.0 vs. 94.88/0.15%

- Block, 2,500 SFRF3 94.50/94.75/95.00 6.0

- Block, 1,500 short Nov 95.50/95.62/95.75/95.87 call condors, 1.0

- Block, 5,000 SFRH3 95.00 calls, 16.5 total volume>20.9k

- 5,000 SFRX2 95.25/95.31 put spds

- 10,000 SFRH3 95.00/95.12 call spds vs. 20,000 SFRZ2 95.50/95.62 call spds

- Block, 4,000 SFRM 94.50/94.75/95.00 put flys, 3.5

- 5,000 SFRZ 95.37/95.50/95.62 call flys

- 4,100 short Nov 95.25/95.37/95.43/95.56 put condors

- Block, 2,000 SFRZ2 95.25/95.50/95.75 put flys, 10.5 ref 95.39

- 5,000 SFRM3 94.06/94.43 put spds

- Eurodollar Options:

- 25,000 Dec 99.12/99.25 put spds

- 4,000 short Dec 94.75 puts

- 6,000 Dec 94.62 puts, 3.0 ref 94.81

- 5,000 Jan 94.87/95.50 1x2 call spds - vs. short Jan SOFR 94.75/95.00 put spds

- 15,000 Dec 94.50/94.68 put spds

- Treasury Options:

- Block, 11,185 wk3 TY 110.5/112.5 2x3 call spds, 52 vs. 109-29

- Block, 25,000 TYZ2 112.5 calls, 9 ref 109-28

- +5,000 TYZ 109/TYH 107 put spds, 24 March over

- 12,000 FVZ 105.5/106 put spds

- 5,000 TYZ 108/109 put spds, 21

- 2,000 TYH3 112/116/120 call flys

- 8,000 TYZ2 108.5 puts, 35 ref 109-24

- 3,000 TUZ2 101.37 puts, 8

EGBs-GILTS CASH CLOSE: BoE Delivers 75bp Hike, Long End Gilts Weaken

European bonds continued to weaken Thursday following the lead of a hawkish Fed late Wednesday, with Bunds outperforming Gilts at the long end, and vice versa.

- Along with today's largely-expected 75bp hike (with a 7-2 vote), the BoE meeting communications also suggested that the recent market implied peak rate of 5.25% was too high.

- The UK long end underperformed in a bear steepening move, with BoE's Ramsden noting that the bank could start selling longer-end Gilts in the new year.

- The German curve saw very slight bear flattening. MNI interviewed ECB's Kazaks who said the bank would probably have to continue hiking past March, while calling for the ECB to start rolling off its APP holdings in Q1 next year.

- Attention Friday is on the US Employment Report.

CLOSING YIELDS / 10-YR PERIPHERY EGB SPREADS TO GERMANY:

- Germany: The 2-Yr yield is up 10.3bps at 2.085%, 5-Yr is up 10.5bps at 2.128%, 10-Yr is up 10.4bps at 2.245%, and 30-Yr is up 7.2bps at 2.169%.

- UK: The 2-Yr yield is up 3.7bps at 3.095%, 5-Yr is up 8bps at 3.443%, 10-Yr is up 12.2bps at 3.521%, and 30-Yr is up 14.8bps at 3.719%.

- Italian BTP spread up 1.8bps at 217.4bps / Spanish down 1.6bps at 107.3bps

EGB Options: OTM Bund Trades And Euribor Unwinds Feature

Thursday's Europe rates / bond options flow:

- RXZ2 144.5/147.5cs traded 8 in 2k

- RXF3 141/144cs, bought for 50 in 4k. Underlying March 2023 trades at 136.16

- OEZ2 119/118.25ps vs 120.50c, bought the ps for 6 in 3k vs 1.11k at 118.97 in Bobl

- ERZ2 97.87/97.75ps, sold at 7.25 in 5k (ref 97.735, -22 del)

- ERZ2 97.50/97.75/98.00 iron c fly, sold at 14.75 in 10k

- ERZ2 97.75/97.50/97.25p fly, sold at 5.75 in 8k (unwind)

- ERZ2 98.00/97.75/97.50 put fly sold at 10 in 11k (unwind)

- ERZ2 97.50/97.25/97.00 put fly sold at 1.75 in 10k (unwind)

FOREX: GBPUSD Sinks 2% In Fed/BoE Aftermath

- The US Dollar surged on Thursday as markets digested a hawkish FOMC press conference and the greenback extended the strong reversal higher from late Wednesday. The expectation of a higher terminal rate for the Fed continues to see pressure on front-end rates, underpinning a significant 1.45% advance for the USD index.

- The biggest victim to the dollars advance has been GBP. Cable had dropped roughly 150pips in advance of the Bank of England decision/statement and despite delivering a substantial 75bp hike, the lacklustre growth forecasts and rhetoric on rates dampened GBP sentiment further.

- The pair remains close to the lows at 1.1170 as of writing, down 2% on the session. Having now broken below support at 1.1272, the next target on the downside resides at 1.1061, the October 21 low, before 1.0924, low on Oct 12 and a key short-term support.

- In a relatively less pronounced move, EUR/USD (-0.62%) is now back below key support at 0.9812 today, which marked the top of the bear channel that was breached last week. A clear break of this support now undermines the recent bullish outlook and signals scope for a deeper pullback.

- Showing impressive resilience in the face of a firmer USD are both the Mexican peso and the Brazilian Real, with the latter continuing to benefit from the apparent smooth transition occurring following former President Lula’s victory in Sunday’s presidential election.

- Markets largely consolidated in the hours approaching the APAC crossover in anticipation of tomorrow’s release of October non-farm payrolls. Consensus looks for a payrolls report that would imply only a marginal easing in labor market tightness in October, with supply struggling to recover to pre-pandemic levels and an u/e rate near record lows.

FX: Expiries for Nov04 NY cut 1000ET (Source DTCC)

- EUR/USD: $0.9750(E615mln), $0.9790-00(E1.5bln), $0.9825(E650mln), $0.9900(E1.5bln), $1.0000(E2.3bln), $1.0100(E1.2bln)

- USD/JPY: Y146.00($607mln), Y147.00($973mln), Y148.00($580mln), Y149.00($553mln)

- GBP/USD: $1.1500(Gbp591mln)

- USD/CAD: C$1.3695-00($739mln), C$1.3800($689mln)

- USD/CNY: Cny7.2000($874mln), Cny7.3000($530mln)

Late Equity Roundup: Energy Sector Remains Strong

Stocks trade moderately weaker, but clinging near top end of the session range as Energy and Industrial shares backstop SPX eminis currently trading -18.75 (-0.5%) at 3750; DJIA -17.89 (0.06%) at 32166.44; Nasdaq -112.9 (-1.1%) at 10411.95.

- SPX leading/lagging sectors: Energy outperforming (+2.42%) as oil and gas shares trade strong (ConocoPhillips +6.85%; Marathon +5.31%; Diamondback Energy +2.51%), followed by Industrials (+1.90%) w/ construction and engineering shares stronger. Laggers: Information Technology (-2.11%) weighed by hardware makers underperforming software (Qualcomm -6.60%), Communication Services next up (-2.08%)

- Dow Industrials Leaders/Laggers: Boeing (BA) continues to outperform +10.06 at 157.47, Caterpillar (CAT) +6.10 at 220.64, Honeywell (HON) +4.96 at 205.43. Laggers: Home Depot (HD) -6.79 at 281.94, Visa (V) -4.98 at 195.97, Apple (AAPL) -4.98 at 140.05.

E-MINI S&P (Z2): Watching Support

- RES 4: 4100.00 Round number resistance

- RES 3: 4023.44 61.8% retracement of the Aug 16 - Oct 13 downleg

- RES 2: 3981.25 High Sep 14

- RES 1: 3928.00 High Nov 1

- PRICE: 3747.00 @ 1510ET Nov 3

- SUP 1: 3704.25/3641.50 Intraday low / Low Oct 21

- SUP 2: 3590.50/3502.00 Low Oct 17 / 13 and the bear trigger

- SUP 3: 3491.13 50.0% retracement of the 2020 - 2022 bull cycle

- SUP 4: 3453.78 1.618 proj of the Aug 16 - Sep 7 - 13 price swing

S&P E-Minis are lower today, extending the pullback from 3928.00, the Nov 1 high. Despite the latest retracement, a bull cycle remains in play following the recovery from 3502.00, Oct 13 low. A resumption of gains would refocus attention on 3928.00, where a break would confirm the bull theme and open 3981.25, Sep 14 high. Key short-term support has been defined at 3641.50, the Oct 21 low. A break would strengthen any developing bearish threat.

COMMODITIES

- WTI Crude Oil (front-month) down $1.75 (-1.94%) at $88.26

- Gold is down $3.51 (-0.21%) at $1631.71

Friday Data Calendar

| Date | GMT/Local | Impact | Flag | Country | Event |

| 04/11/2022 | 0030/1130 | *** |  | AU | RBA Statement on Monetary Policy |

| 04/11/2022 | 0030/1130 | *** | | AU | Retail trade quarterly |

| 04/11/2022 | 0030/0930 | ** |  | JP | IHS Markit Final Japan Services PMI |

| 04/11/2022 | 0700/0800 | ** |  | DE | Manufacturing Orders |

| 04/11/2022 | 0745/0845 | * |  | FR | Industrial Production |

| 04/11/2022 | 0800/0900 | ** |  | ES | Industrial Production |

| 04/11/2022 | 0815/0915 | ** | | ES | IHS Markit Services PMI (f) |

| 04/11/2022 | 0845/0945 | ** |  | IT | IHS Markit Services PMI (f) |

| 04/11/2022 | 0845/0945 |  | EU | ECB de Guindos Speech at Naturgy Foundation/IESE School | |

| 04/11/2022 | 0850/0950 | ** | | FR | IHS Markit Services PMI (f) |

| 04/11/2022 | 0855/0955 | ** | | DE | IHS Markit Services PMI (f) |

| 04/11/2022 | 0900/1000 | ** | | EU | IHS Markit Services PMI (f) |

| 04/11/2022 | 0930/0930 | ** |  | UK | IHS Markit/CIPS Construction PMI |

| 04/11/2022 | 0930/1030 | | EU | ECB Lagarde Open Lecture | |

| 04/11/2022 | 1000/1100 | ** | | EU | PPI |

| 04/11/2022 | - | | DE | G7 Foreign Ministers summit in Germany | |

| 04/11/2022 | 1215/1215 | | UK | BOE Pill & Shortall MonPol Report National Agency briefing | |

| 04/11/2022 | 1230/0830 | *** |  | CA | Labour Force Survey |

| 04/11/2022 | 1230/0830 | *** |  | US | Employment Report |

| 04/11/2022 | 1400/1000 | * | | CA | Ivey PMI |

| 04/11/2022 | 1400/1000 | | US | Boston Fed's Susan Collins | |

| 04/11/2022 | 2000/1600 | | US | Fed's Financial Stability Report |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.