Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- MNI US: Biden To Announce New Package Of Ukraine Aid Ahead Of Zelenskyy WH Meeting

- MNI MIDEAST: White House Closes In On Deal With Israel And Saudi Arabia

- US: Yellen: US Discussing Windfall Tax On Frozen Russia Assets w/EU, Bbg

- RUSSIA IMPOSES BAN ON GASOLINE, DIESEL EXPORT FROM SEPT 21, Bbg

- ECB'S KNOT: SATISFIED WITH WHERE WE ARE WITH MONETARY POLICY, Bbg

US TSYS Yields Climb to New Highs After BoE Follows Fed With Hawkish Hold

- Tsy futures bounced briefly but remained under pressure after the BoE left rate unchanged at 5.25%. Split five-to-four in deciding to leave the Bank Rate on hold. All the senior Bank insiders on the committee, with the exception of departing Deputy Governor Jon Cunliffe, backing no change.

- Rate futures extended lows (yields at new 16Y highs: 10YY marking 4.881%) after weekly claims came out lower than expected at 201k vs. 225k (small up-revision in prior to 221k from 220k), broad decline in Philadelphia Fed Business Outlook, however, -13.5 vs -1.0 est, 12.0 prior.

- Rates held near lows after Existing Home Sales came out a little softer than expected (4.04M vs 4.1M est), MoM (-0.7% vs 0.7% est), Leading Index (-0.4% vs. -0.5 est, prior up-revised to -0.3% from -0.4%).

- Thursday session low of 108-08 put focus on 108-00 and 107-23, the 1.236 projection of the Jul 18 - Aug 4 - Aug 10 price swing.

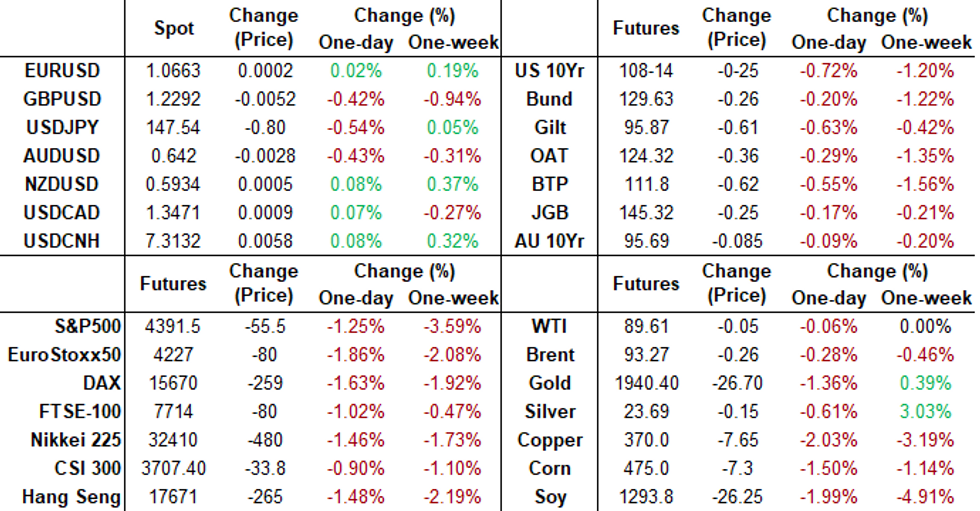

- Cross asset summary: Greenback near flat (DXY +.015 at 105.343), Gold weaker (-9.56 at 1920.74), crude weaker (WTI -.08 at 89.58) and stocks extending late lows: DJIA is down 218.24 points (-0.63%) at 34223.35, S&P E-Mini Futures down 55.5 points (-1.25%) at 4392, Nasdaq down 184.6 points (-1.4%) at 13285.99.

- Friday focus: S&P Global PMIs, while Fed speakers return from policy blackout: both at 1300ET, separate events: SF Fed Daly on economy, policy and MN Fed Kashkari fireside chat, audience Q&A, livestreamed.

SHORT TERM RATES

SOFR Benchmark Settlements:

- 1M -0.00373 to 5.31972 (-0.00732/wk)

- 3M +0.00396 to 5.40009 (-0.00169/wk)

- 6M +0.00378 to 5.47283 (+0.00699/wk)

- 12M +0.00710 to 5.46596 (+0.04452/wk)

- Daily Effective Fed Funds Rate: 5.33% volume: $89B

- Daily Overnight Bank Funding Rate: 5.32% volume: $253B

- Secured Overnight Financing Rate (SOFR): 5.30%, $1.492T

- Broad General Collateral Rate (BGCR): 5.30%, $568B

- Tri-Party General Collateral Rate (TGCR): 5.30%, $554B

- (rate, volume levels reflect prior session)

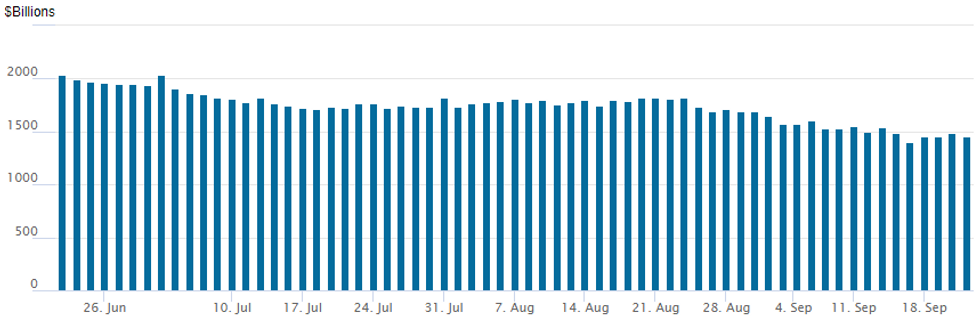

FED REVERSE REPO OPERATION

NY Federal Reserve/MNI

Repo operation recedes to 1,454.115B w/99 counterparties, compared to $1,486.984B in the prior session. The high for 2023 stands at $2,375.171B on Friday March 31, 2023; all-time record high of $2,553.716B reached December 30, 2022.

SOFR/TREASURY OPTION SUMMARY

Traders rushed off the sidelines in the aftermath of the latest FOMC and BoE's hawkish hold policy announcements, generating a surge in SOFR/Treasury option volumes as underlying futures extended lows.

- Treasury curves bear steepened after the Fed left rates steady Wednesday, but kept the door open to one more increase in borrowing costs this year, while reducing the number of rate cuts officials see in 2024.

- Rate hike projections into early 2024 receded slightly: November at 29.0% w/ implied rate change of +7.2bp to 5.40%, December cumulative of 12.9bp at 5.457%, January 2024 13.5bp at 5.463%. Fed terminal at 5.46% in Jan'24-Feb'24.

- SOFR Options:

- Block/screen, over 40,000 SFRF4 94.75/95.25/95.75 call flys, 3.75 ref 94.61

- 8,500 SFRZ3 96.06 calls, 1.25 ref 94.525

- Block, 11,111 SFRG4 94.00/94.25 put spds, 2.5 ref 94.61, opener

- +10,000 SFRU4 94.50/94.75 put spds, 11.25

- 4,000 SFRF4 94.75/95.25/95.75 call flys

- -10,000 0QV3 95.18/95.25 put spds, 3.0

- 4,500 SFRM4 94.50/95.00 2x1 put spds ref 94.73

- Block, 6,000 0QZ3 95.00/95.25/95.50 put trees, 2.0 ref 95.29

- Block, 2,500 SFRF4 94.75/95.25/95.75 call flys, 3.5 ref 94.59

- 4,500 SFRF4 94.25/94.37 put spds

- 2,000 SFRM4 94.75/94.50/96.25 call flys

- 4,000 0QZ3 95.50/96.50 call spds vs. 3QZ3 96.25/97.25 call spds

- 4,500 SFRF4 94.25/94.37 put spds

- 5,300 SFRZ3 94.56/94.62/94.68 call flys

- Block, 3,500 SFRZ3 94.56/94.62/94.75/94.81 call condors

- Block, 3,000 3QV3 95.75 puts, 2.5 vs. 96.12/0.15%

- over 12,000 0QZ3 94.87/95.12/95.25/95.37 put condors, ref 95.31

- 1,500 SFRX3 94.31/94.37/94.50 put flys ref 94.52

- 3,000 SFRH4 94.75 puts, 33.0 ref 94.58

- 2,500 SFRZ3 94.56/94.62/94.68 call flys ref 94.52

- over 5,000 0QZ3 95.00/95.25/95.50 put trees ref 95.31

- over 5,000 0QZ3 95.25 puts covered ref 95.32 to -.325

- over 14,000 0QZ3 95.25/95.75 put spds ref 95.32 to -.325

- 4,000 0QV3 95.37/95.50/95.62 call flys ref 95.315

- 2,300 0QZ3 95.75/95.87 put spds ref 95.285

- 3,500 0QZ3 95.50/95.62 put spds ref 95.285

- over 8,600 2QV3 95.87 puts, 8.5 ref 95.975 to -.98

- Treasury Options:

- over 26,700 TYX3 107.5/109.5 put spds, 62 ref 108-14.5

- Over +7,400 USX3 112 puts, 33-35 ref 116-12

- 6,000 TYX3 115 calls, 2 ref 108-14.5

- 5,000 TYX3 112 calls, 6 ref 108-14

- 10,000 TYX3 108 puts, 44 ref 108-16.5, prior trades puts volume >33k

- 2,000 TUV3 101.5 calls ref 101-06.5

- 4,000 TYX3 109.5 calls, 31 ref 108-14.5

- over 8,500 TYV3 108.5 puts, 10-14

- 3,000 TYZ3 103/105/107 put flys, 20 ref 108-22

- over 4,000 FVX3 105/105.5 put spds ref 105-09.25

- 1,000 FVZ3 106.25/107.25/108.25/109.25 call condors ref 105-11.75

- 4,500 TYX3 109/110 call spds ref 108-22.5

- over 4,500 TYX3 111.5 calls, 8 ref 108-23

- over 4,300 TUV3 101.5 puts, 16.5 ref 101-07.62

- over 7,100 TUV3 101.37 puts, 9.5-10 ref 101-07.75 to -07.38

- 4,000 TYX3 107/108 2x1 put spds ref 108-22

- 2,200 TYX3 107.5/108.5 put spds, 21 ref 108-22.5

- 2,000 TYV3 109 puts, 31 ref 108-22

- 5,000 TYV3 107.75 calls, 58 ref 108-20

- 1,500 FVX3 106.25 puts, ref 105-10

- 2,500 FVV3 104.75/105 put spds, 4.5 ref 105-08.5

- 2,500 TYX3 108/112 strangles, 45 ref 108-23

EGBs-GILTS CASH CLOSE: UK Curve Steepens As BoE Holds

The Bank of England's decision to hold rates saw the UK curve steepen Thursday, with the German curve following suit.

- After global bonds sold off overnight in the wake of the Fed's hawkish rate hold, a dovish tone was restored in early European trade with the SNB's unexpected hold and in-line hikes by the Riksbank and Norges Bank. The BoE's 5-4 decision to hold rates - which was only 45% priced in vs a 25bp hold - marked the peak for European core FI for the day.

- After selling off in the afternoon, UK and German yields fell back and finished off session highs.

- Helping the recovery were multiple comments by ECB participants across the hawk-dove spectrum pointing to prospects of an extended hold including Stournaras, Wunsch, and Knot.

- The UK curve finished sharply bear steeper with Germany's modestly twist steepening.

- Periphery EGB spreads widened, led by Italy, amid a broader risk-off move that accelerated in the afternoon as equities dropped and curves re-steepened.

- Friday sees UK retail sales data and September flash PMIs.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is down 0.3bps at 3.257%, 5-Yr is up 2.2bps at 2.756%, 10-Yr is up 3.5bps at 2.737%, and 30-Yr is up 2.8bps at 2.87%.

- UK: The 2-Yr yield is up 2.5bps at 4.873%, 5-Yr is up 3.3bps at 4.426%, 10-Yr is up 9bps at 4.305%, and 30-Yr is up 7.7bps at 4.709%

- .Italian BTP spread up 5.5bps at 180.4bps / Greek up 4.6bps at 142bps

EGB Options: Some Unwinding Thursday

Friday's Europe rates / bond options flow included:

- RXX3 130.00/131.50/133.00 call fly paper paid 25 on 4K

- RXX3 130.50/133.00 call spread paper paid 52.5 & 53 on 3.75K

- ERV3 96.00/95.75/95.50 1x3x2 put fly 5K given at 3.5, looks like a closer

FOREX Greenback Rally Fails To Extend Following Fed-Inspired Impulse

- Early on Thursday, the greenback showed initial strength, extending on topside momentum following the hawkish hold from the FOMC. The USD index narrowed in on the best levels for 2023, reaching a high print of 105.74.

- However, a reversal lower for front-end US yields and considerable weakness for US equity indices dampened the initial greenback optimism which now sees the DXY trade at unchanged levels as we approach the APAC crossover. It is worth noting that we still remain roughly half a percent above pre-FOMC levels.

- Remaining the underperformer on the session is the Swiss Franc following the surprise hold by the SNB at 1.75%. While Chairman Jordan pointed to the potential for further hikes and noted that the inflation battle is not yet over, some of the language deployed and the SNB playing down the idea of a hawkish pause has also weighed on the CHF, prompting EURCHF to establish a new range around 0.9640, up ~0.60%.

- Cable remains down 0.4% on the session, although is unchanged from the surprise decision by the Bank of England to hold rates at 5.25%. Initial pressure did see GBPUSD print a fresh near-six month low at 1.2239 before consolidating back around the 1.2300 mark in late Thursday trade.

- One of the more interesting moves across US hours was the decline for USDJPY, posting an impressive turnaround and reversing the entirety of the Fed inspired gains overnight. The pair printed as high as 148.46 overnight, briefly piercing noted resistance at the Nov 4 2022 high but failed to garner any momentum across the APAC session. A subsequent move back below the 148.00 handle has kept the short-term path of least resistance as lower, with pressure on equities and the lower front-end US yields providing additional JPY tailwinds, that saw a move down to 147.32 as we approach the Bank of Japan decision overnight.

- The BOJ meeting caps off a busy week for major central bank decisions. Considering the adjustments made to the BOJ’s YCC framework in July, our analysis aligns with the prevailing consensus, anticipating that the BOJ will maintain its existing policies in the upcoming announcement, including the short-term interest rate remaining at -0.1%.

- Elsewhere on Friday, UK retail sales and Eurozone flash PMI’s will provide the latest signals regarding the health of the Eurozone economy.

Late Equity Roundup: Real Estate, Cons Disc, Materials Underperform

- Stocks continue to gradually extend session lows in the aftermath of this morning's "hawkish hold" policy announcement from the BOE. Currently, DJIA is down 218.24 points (-0.63%) at 34223.35, S&P E-Mini Futures down 55.5 points (-1.25%) at 4392, Nasdaq down 184.6 points (-1.4%) at 13285.99.

- Laggers: Reversing the prior session gains as Tsy yields climbed to new 16Y highs this morning (10YY 4.881%), Real estate sector weighed by property management names: CoStar Group -3.45%, CBRE Group -3.35%.

- Consumer Discretionary and Materials sectors followed, with broadline retailers weighing on the former: Amazon -3.75%, CarMax -2.0%, Ebay -1.88%. Construction materials stocks weighed on Materials sector: Martin Marietta Materials -3.4%, Vulcan Materials -3.15%.

- Leaders: Utilities, Health Care and Consumer Staples sectors outperformed in the second half. Electrical and multi-energy providers buoyed Utilities: Eversource +.75%, Public Service Ent +0.35% while Ameren gained +0.25%.

- Equipment and service providers buoyed the Health Care sector: Humana +2.5%, Centene +2.35%, UnitedHealth Group +2.15%. Meanwhile, Consumer Staples sector were buoyed by household and personal products makers: Kenvue +0.85%, Kimberly-Clark +0.75%.

- Technicals: A bear cycle in S&P E-minis remains in play and this week’s break lower reinforces current conditions. Today’s sell-off has resulted in a break of support at 4397.75, the Aug 18 low that reinforces bearish conditions and signals scope for a continuation lower near-term. Sights are on 4377.85, a Fibonacci projection. Further out, scope is seen for a move to 4352.50, the Jun 8 low. Initial firm resistance is 4507.79, the 50-day EMA.

E-MINI S&P TECHS: (Z3) Trades Through Key Support

- RES 4: 4673.50 High Aug 1

- RES 3: 4617.40 76.4% retracement of the Jul 27 - Aug 18 sell-off

- RES 2: 4566.00/4597.50 High Sep 15 / 1 and a near-term bull trigger

- RES 1: 4447.00/4507.79 Intraday high / 50-day EMA

- PRICE: 4391.25 @ 19:30 BST Sep 21

- SUP 1: 4377.85 0.764 proj of the Jul 27 - Aug 18 - Sep 1 price swing

- SUP 2: 4352.50 Low Jun 8

- SUP 3: 4318.00 Low Jun 2

- SUP 4: 4300.62 50.0% retracement of the Mar 13 - Jul 27 bull cycle

A bear cycle in S&P E-minis remains in play and this week’s break lower reinforces current conditions. Today’s sell-off has resulted in a break of support at 4397.75, the Aug 18 low. The breach reinforces bearish conditions and signals scope for a continuation lower near-term. Sights are on 4377.85, a Fibonacci projection. Further out, scope is seen for a move to 4352.50, the Jun 8 low. Initial firm resistance is 4507.79, the 50-day EMA.

COMMODITIES Crude Rangebound Whilst Gold Comes Under Further Post-FOMC Pressure

- Crude has been largely rangebound on the day, relinquishing the earlier gains as the USD index pulled back but ultimately consolidated yesterday’s post-FOMC strength and wider demand concerns offset Russia’s ban on diesel and gasoline exports.

- Despite the price pull back the market remains over 10$/bbl higher than the low in August with support from OPEC+ cuts and demand optimism for US and China leading to a drawdown in global inventories.

- Morgan Stanley has raised its Q4 Brent forecast to $95/b, up from $82.5/b, although it remains sceptical that prices could surpass $100/bbl

- A federal appeals court in New York ruled that Venezuela’s PDVSA is unable to use sanctions as an excuse for not paying $348mn in defaulted debt.

- WTI is -0.1% at $89.57 as it holds above support at the 20-day EMA of $86.25.

- Brent is -0.3% at $93.23 as it holds above support at the 20-day EMA of $90.36.

- Gold is -0.5% at $1920.36, coming under pressure from the sizeable twist steepening seen in Treasuries with longer-dated yields up strongly. It’s a significant retracement off yesterday’s pre-FOMC high of $1947.5, although the low of $1913.98 didn’t test support at $1901.1 (Sep 14 low).

FRIDAY DATA CALENDAR

| Date | GMT/Local | Impact | Flag | Country | Event |

| 22/09/2023 | 2300/0900 | *** |  | AU | Judo Bank Flash Australia PMI |

| 22/09/2023 | 2301/0001 | ** |  | UK | Gfk Monthly Consumer Confidence |

| 22/09/2023 | 0030/0930 | ** |  | JP | Jibun Bank Flash Japan PMI |

| 22/09/2023 | 0200/1100 | *** | | JP | BOJ policy announcement |

| 22/09/2023 | 0600/0700 | *** | | UK | Retail Sales |

| 22/09/2023 | 0700/0900 | *** |  | ES | GDP (f) |

| 22/09/2023 | 0715/0915 | ** |  | FR | S&P Global Services PMI (p) |

| 22/09/2023 | 0715/0915 | ** | | FR | S&P Global Manufacturing PMI (p) |

| 22/09/2023 | 0730/0930 | ** |  | DE | S&P Global Services PMI (p) |

| 22/09/2023 | 0730/0930 | ** | | DE | S&P Global Manufacturing PMI (p) |

| 22/09/2023 | 0800/1000 | ** |  | EU | S&P Global Services PMI (p) |

| 22/09/2023 | 0800/1000 | ** | | EU | S&P Global Manufacturing PMI (p) |

| 22/09/2023 | 0800/1000 | ** | | EU | S&P Global Composite PMI (p) |

| 22/09/2023 | 0830/0930 | *** | | UK | S&P Global Manufacturing PMI flash |

| 22/09/2023 | 0830/0930 | *** | | UK | S&P Global Services PMI flash |

| 22/09/2023 | 0830/0930 | *** | | UK | S&P Global Composite PMI flash |

| 22/09/2023 | 1000/1100 | ** | | UK | CBI Industrial Trends |

| 22/09/2023 | 1100/1300 | | EU | ECB's de Guindos Speaks at Event | |

| 22/09/2023 | 1230/0830 | ** |  | CA | Retail Trade |

| 22/09/2023 | 1250/0850 |  | US | Fed Governor Lisa Cook | |

| 22/09/2023 | 1345/0945 | *** | | US | IHS Markit Manufacturing Index (flash) |

| 22/09/2023 | 1345/0945 | *** | | US | S&P Global Services Index (flash) |

| 22/09/2023 | 1400/1000 | | US | Boston Fed's Susan Collins | |

| 22/09/2023 | 1700/1300 | | US | San Francisco Fed's Mary Daly | |

| 22/09/2023 | 1700/1300 | | US | Minneapolis Fed's Neel Kashkari |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.