Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

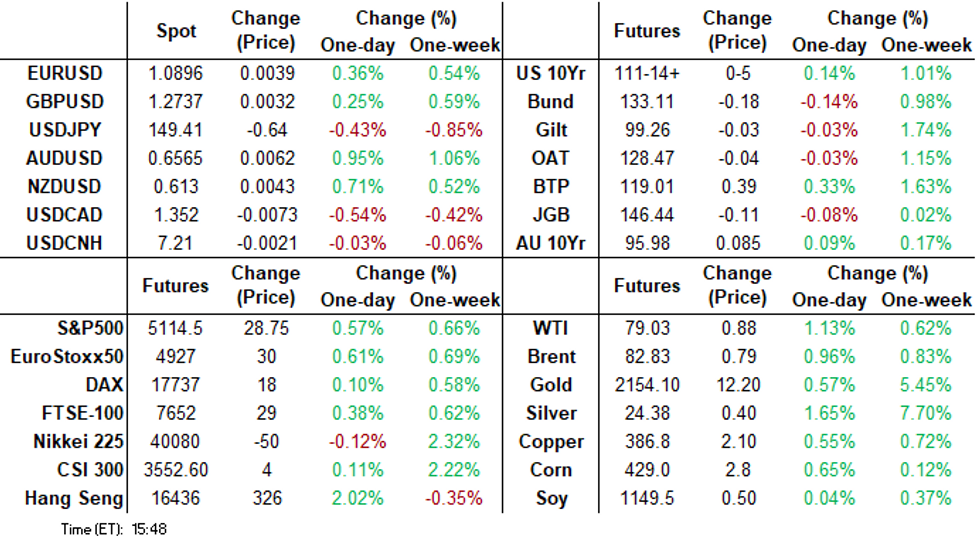

- Treasuries pared early losses following lower than expected ADP jobs gain and prior JOLTS down-revision

- Markets also reacted positively to Fed Chairman Powell's policy testimony, deemed less hawkish than expected

- Gold surged to new record high of $2152.25, West Texas Crude rallied over 80.60 amid ongoing geopol tensions.

US TSYS Positive Reaction to Jobs Data, Powell Policy Testimony

- Tsy futures hold narrow range since climbing to session highs at noon. Tsys pared early shorts following marginally lower than expected ADP at 140k (cons 150k) after a modestly upward revised 111k in Jan (initial 107k).

- Support for Treasury futures has gained traction as markets continue to digest text of Fed Chairman Powell's testimony to congress (as well as down-revision to the prior JOLTS job openings from 9.026M to 8.889M), focus on cutting interest rates "at some point this year" but not until it becomes more confident that inflation will keep falling.

- Little if any reaction to Fed Beige Book release: "Economic activity increased slightly, on balance, since early January, with eight Districts reporting slight to modest growth in activity, three others reporting no change, and one District noting a slight softening.”

- Rates pared late gains in reaction to headlines that NYCB has raised more than $1B in equity from "LIBERTY STRATEGIC, HUDSON BAY, REVERENCE" Bbg.

- Jun'24 10Y futures are currently at 111-14 (+4.5) after breaching resistance on way to 111-23 high at noon. Next resistance level at 111-27 50% (retracement of the Feb 1 - 23 bear leg). Curves flatter, 2s10s -4.468 at -45.218; 10Y yield at 4.1098 -.0428 vs. 4.0768% low.

- Thursday Data Calendar: Weekly Claims, Unit Labor Cost, and day two of Chairman Powell's testimony.

SOFR FIXES AND PRIOR SESSION REFERENCE RATES

SOFR Benchmark Settlements:

- 1M -0.00105 to 5.31983 (-0.00279/wk)

- 3M -0.00185 to 5.32454 (-0.00658/wk)

- 6M -0.00663 to 5.24582 (-0.02149/wk)

- 12M -0.02144 to 5.01413 (-0.04241/wk)

- Secured Overnight Financing Rate (SOFR): 5.31% (+0.00), volume: $1.807T

- Broad General Collateral Rate (BGCR): 5.30% (+0.00), volume: $680B

- Tri-Party General Collateral Rate (TGCR): 5.30% (+0.00), volume: $670B

- (rate, volume levels reflect prior session)

- Daily Effective Fed Funds Rate: 5.33% (+0.00), volume: $101B

- Daily Overnight Bank Funding Rate: 5.32% (+0.01), volume: $288B

FED Reverse Repo Operation

NY Federal Reserve/MNI

- RRP usage climbs to $456,847B from $444.474B Tuesday. Compares to $439.793B on Monday -- the lowest since May 2021.

- Meanwhile, the latest number of counterparties slips to 68 from 74 Monday (compares to 65 on January 16, the lowest since July 7, 2021).

SOFR/TEASURY OPTION SUMMARY

Mixed SOFR and Treasury option flow segued to better call volume Wednesday as underlying futures bounced off lows. Initially on the the back of lower than expected ADP private employment data and Federal Reserve Chairman Powell's testimony to congress deemed less hawkish than it could have been.

In turn, projected rate cut pricing gained slightly on the day: March 2024 chance of 25bp rate cut currently -5.4% w/ cumulative of -1.4bp at 5.318%; May 2024 at -20.7% w/ cumulative -5.7bp at 5.271%; June 2024 -63.2% from -61.8% earlier w/ cumulative cut -21.8bp at 5.113%. July'24 cumulative -36.1bp at 4.970%.

- SOFR Options:

- +12,000 0QH4 96.00/96.25 call spds 5.25 ref 95.90

- +8,500 SFRZ4 95.25/95.50/95.75/96.25 broken call condors, 0.25

- +2,000 SFRN4 95.25 straddles, 45.5 ref 95.24

- -5,000 SFRJ4 95.37/95.75 call spds, 0.75 ref 94.925

- -3,000 SFRU4 95.75/96.75 call spds 8.25, ref 95.24

- -3,000 SFRH4 94.62/94.68/94.75/94.81 put condors 4.75 ref 94.69

- +5,000 0QK4 95.62/96.25 call over risk reversals, 3.0 vs. 96.15/0.42%

- +5,000 SFRM4 94.68/94.81 2x1 put spds 1.75 ref 94.935

- +3,000 2QH4 96.50 straddles, 20.25, still bid

- Block, 8,000 SFRK4 94.75/94.81/94.87/94.93 put condors, 1.5 ref 94.93

- 2,000 SFRH4 94.75/94.87 2x1 put spds ref 94.6925

- 6,000 SFRJ4 95.00/95.12 call spds ref 94.93

- 8,000 SFRK4 94.75/94.81/94.87/94.93 put condors ref 94.93

- 2,000 SFRM5 97.75/98.25 call spds ref 96.105

- 2,000 SFRM4 94.68/94.81 2x1 put spds

- 2,000 0QH4 96.06/96.18 call spds ref 95.86

- Treasury Options:

- -10,000 TYJ4 110/113 call over risk reversals, 2 vs. 111-19/0.37%

- 12,000 TYM4 118/119/120/121 call condors

- 1,000 USJ4 116/117/119 broken put flys

- -15,000 TYJ4/TYM4 112 call calendar spds, 46 ref 111-16 to -15, Jun sold over

- 5,000 USJ4 112/114/116/118 put condors, 6 ref 121-03

- 5,600 TYM4 109 puts, 34 ref 111-16.5

- 3,600 TYJ4 110.25/111.5 strangles, 57 ref 111-08.5

- over 9,800 FVJ4 106.75 puts ref 107-13.25

- 1,700 TYJ4 111.25 calls, 43 ref 111-03

FOREX USD Index Declines 0.5%, Trades To One-Month Lows

- Lower US yields and higher equity benchmarks have weighed on the greenback on Wednesday, with G10 currency ranges showing some signs of life ahead of further event risk scheduled later this week. The USD Index's leg lower puts the greenback at the weakest since early February and further slippage through 102.918 would entirely erase the upleg posted on the back of the bumper US payrolls release.

- The most notable beneficiaries of the weaker dollar have been AUD and NZD, with the former surging 1.15% and extending the bounce off yesterday's pullback low of 0.6478, and is rebuffing the bearish outlook that should hold below key S/T resistance at 0.6595, the Feb 22 high.

- Much of the AUD strength stems from the China NPC growth targets suggesting scope for both fiscal and monetary easing in China - disappointment with which could prompt an AUD reversal and re-orient focus on the downside. Sizeable AUD options are set to roll-off at Thursday's NY cut between $0.6520-25, with A$1.1bln notional seen expiring.

- Similarly, the Canadian dollar has risen 0.7%, after the Bank of Canada stuck to its perceived continued threat of persistent underlying inflation. USDCAD fell around 30 pips to ~1.354 in the direct aftermath, and gradually extended to a 1.3501 session low, narrowing the gap with support at 1.3494 (50-day EMA).

- Gains for both the Japanese Yen and the Euro have matched the size of adjustment in the broad USD index. EURUSD made above 1.0888 resistance to print the best levels since Feb02 and recapture the 1.0900 handle in the process with 1.0932 the next notable level.

- Price action should keep EUR levels in focus headed into tomorrow's ECB decision - with Friday's NFP likely to add to FX volatility. Elsewhere, China trade data will cross overnight before German factory orders and Swiss currency reserves in early European hours.

FX Expiries for Mar07 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0775-90(E1.9bln), $1.0810-25(E2.5bln), $1.0635-40(E1.0bln)

- USD/JPY: Y149.50($1.1bln), Y150.00($858mln), Y150.25-35($1.6bln), Y150.50-60($1.1bln), Y150.90-05($1.9bln)

- GBP/USD: $1.2480-85(Gbp2.1bln), $1.2650(Gbp538mln)

- AUD/USD: $0.6520-25(A$1.1bln)

- AUD/NZD: N$1.0600(A$664mln)

- USD/CAD: C$1.3605-15($1.0bln), C$1.3630-35($1.1bln)

- USD/CNY: Cny7.1940-50($1.1bln)

Late Equities Roundup: Off Highs, IT Leads; NYCB Gets $1B Investment

- Still bid, stocks have pared gains in the second half with large sell programs reported in S&P Eminis (appr 40,000 from 5125.5 to 5107.0). Still off Monday's highs, stocks had reacted positively to lower than expected ADP private employment data and Federal Reserve Chairman Powell's testimony to congress deemed less hawkish than it could have been. Currently, DJIA is up 58.14 points (0.15%) at 38640.83, S&P E-Minis up 25.25 points (0.5%) at 5110.5, Nasdaq up 102.6 points (0.6%) at 16040.48.

- Leading Gainers: Information Technology and Health Care sectors outperformed in late trade. Continued demand for high end chips for AI applications supported IT: Skyworks +5.17%, Hewlett Packard Ent +4.97%, Nvidia +3.85% Qualcomm +3.65%. Health Care outpaced earlier gains in the Energy sector: Dexcom surged +8.62% after receiving FDA clearance for a glucose sensor, ResMed +2.56%, GE Healthcare Tech +2.33%.

- Laggers: Communication Services and Consumer Discretionary sectors continued to underperform late, with a mix of media/entertainment and telecom shares weighing on the former: Charter Communications -3.4%, Disney -2.6%, Verizon -1.15%. Automakers weighed on the Consumer Discretionary sector for the third day running, led by Tesla again -2.06%, while Ford traded -1.59%, GM -1.67%.

- Of note, NY Community Bank shares stopped trading after falling over 40% after announcing the beleaguered regional bank was looking for a capital infusion. Shares surged over 30% in late trade after headlines announced the bank received over $1B from a consortium of investors that included "LIBERTY STRATEGIC, HUSDON BAY and REVERENCE", Bbg.

E-MINI S&P TECHS: (H4) Trend Needle Points North

- RES 4: 5193.61 3.0% Bollinger Band

- RES 3: 5172.19 2.0% 10-dma envelope

- RES 2: 5170.86 2.236 proj of Nov 10 - Dec 1 - 7 price swing

- RES 1: 5157.75 High Mar 1

- PRICE: 5105.00 @ 1500 ET Mar 6

- SUP 1: 5049.64 20-day EMA

- SUP 2: 4935.76 50-day EMA

- SUP 3: 4866.00 Low Jan 31 and key support

- SUP 4: 4808.50 Low Jan 19

The trend condition in S&P E-Minis remains bullish and the latest move lower appears to be a correction. Price action continues to highlight the fact that corrections are shallow - this is a bullish signal that highlights positive market sentiment. Support to watch is 5049.64, the 20-day EMA. A clear break of this average would signal potential for a deeper retracement towards 4935.76, the 50-day EMA. Sights are on 5170.86, a Fibonacci projection.

COMMODITIES Gold Sets New Record High, WTI Pares Earlier Strong Gains

- Gold is +0.8% at $2144.34, off an earlier new record high of $2152.25. It’s been buoyed by continued Houthi attacks plus the sizeable depreciation of the US dollar after no hawkish surprises in ADP employment, the JOLTS report or Fed Chair Powell’s testimony.

- Next resistance is seen at $2177.6 (Fibo proj of Oct 6 – 27 – Nov 13 price swing).

- WTI meanwhile has tapered some of its earlier strong gains but remains up on the day. Upside comes from a weakening greenback and a build in US crude stocks in-line with expectations.

- A Houthi missile strike on the container ship True Confidence in the Gulf of Aden killed two crew members and injured six.

- EIA Weekly US Petroleum Summary - w/w change week ending Mar 01: Crude stocks +1,367 vs Exp +1,720, Crude production -100, SPR stocks +706, Cushing stocks +701

- WTI is +1.1% at $79.00. The prior pullback was deemed corrective with resistance seen at $80.85 (Mar 1 high), which it got close to today with $80.67.

- Brent is +1.0% at $82.85, off a high of $84.05 that also came close to resistance at $84.34 (Mar 1 high).

THURSDAY DATA CALENDAR

| Date | GMT/Local | Impact | Flag | Country | Event |

| 07/03/2024 | 0030/1130 | ** |  | AU | Trade Balance |

| 07/03/2024 | 0030/1130 | ** | | AU | Lending Finance Details |

| 07/03/2024 | 0645/0745 | ** |  | CH | Unemployment |

| 07/03/2024 | 0700/0800 | ** |  | DE | Manufacturing Orders |

| 07/03/2024 | 0930/0930 |  | UK | BOE's Monthly Decision Maker Panel Data | |

| 07/03/2024 | - | *** |  | CN | Trade |

| 07/03/2024 | 1315/1415 | *** |  | EU | ECB Deposit Rate |

| 07/03/2024 | 1315/1415 | *** | | EU | ECB Main Refi Rate |

| 07/03/2024 | 1315/1415 | *** | | EU | ECB Marginal Lending Rate |

| 07/03/2024 | 1330/0830 | *** |  | US | Jobless Claims |

| 07/03/2024 | 1330/0830 | ** | | US | WASDE Weekly Import/Export |

| 07/03/2024 | 1330/0830 | * |  | CA | Building Permits |

| 07/03/2024 | 1330/0830 | ** | | US | Trade Balance |

| 07/03/2024 | 1330/0830 | ** | | US | Non-Farm Productivity (f) |

| 07/03/2024 | 1330/0830 | ** | | CA | International Merchandise Trade (Trade Balance) |

| 07/03/2024 | 1345/1445 | | EU | ECB Monetary Policy Press Conference | |

| 07/03/2024 | 1500/1000 | | US | Fed Chair Jay Powell | |

| 07/03/2024 | 1500/1600 | | EU | ECB Podcast - Lagarde presents latest monpol | |

| 07/03/2024 | 1530/1030 | ** | | US | Natural Gas Stocks |

| 07/03/2024 | 1630/1130 | | US | Cleveland Fed's Loretta Mester | |

| 07/03/2024 | 1630/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 07/03/2024 | 1630/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 07/03/2024 | 1700/1200 | | US | BLS webinar on CPI rent and OER | |

| 07/03/2024 | 2000/1500 | * | | US | Consumer Credit |

| 08/03/2024 | 2350/0850 | ** |  | JP | Trade |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.