Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- MNI EXCLUSIVE: Fed Could Signal QE Debate By Summer -Ex-Offls

- MNI BRIEF: Fed's Williams Says Growth Could Be Best in Decades

- MNI BRIEF: Fed Bostic Says Yields Still Low, QE Twist An Option

- MNI INSIGHT: BOE's 'Outdated' QE Unwind Strategy Set To Change

US

FED: The Federal Reserve could signal that it intends to begin debating changes to its bond-buying program by summer time, although an announcement on tapering would not come until at least several months later, former Fed officials told MNI.

- While Fed Chair Jay Powell has resisted talk about exiting from its accommodative stance, massive fiscal programs coupled with declining virus cases and an improved rollout of vaccines has boosted the outlook and pulled forward the timeline for winding down QE, the former officials said.

- A message could be sent in the summer, possibly at the annual Jackson Hole conference in August, to "signal that discussions are starting" in the Fed system about how it would want to dial down its asset purchase program, said Steven Kamin, a former director of the division of international finance at the Fed Board. For more see MNI Policy main wire at 0943ET.

- "With strong federal fiscal support and continued progress on vaccination, GDP growth this year could be the strongest we've seen in decades," Williams said. "We will continue to watch and learn and remain committed to using our full range of tools to help assure that the recovery will be as robust as possible."

- "Yields have definitely moved at the higher end and the longer end. But right now I'm not worried about that," Bostic told reporters. "We're going to keep an eye out."

EUROPE

BOE: The Bank of England looks set to ditch its outdated strategy for exiting quantitative easing but is keen to ensure that investors understand that its review of alternative strategies for unwinding bond purchases is open ended and does not signal any preset timetable for tightening.

- The BOE's current strategy is for QE only to be unwound when Bank Rate hits 1.5%, but, with the market not pricing that in during the next 50 years, this seems ripe for replacement. Hence the review into exit strategy announced at the past policy meeting. For more see MNI Policy main wire at 0731ET.

OVERNIGHT DATA

- US Q4 GDP +4.1%

- US JOBLESS CLAIMS -111K TO 730K IN FEB 20 WK

- US PREV JOBLESS CLAIMS REVISED TO 841K IN FEB 13 WK

- US CONTINUING CLAIMS -0.101M to 4.419M IN FEB 13 WK

- US JAN DURABLE NEW ORDERS +3.4%; EX-TRANSPORTATION +1.4%

- US DEC DURABLE GDS NEW ORDERS REV TO +1.2%

- US JAN NONDEF CAP GDS ORDERS EX-AIR +0.5% V DEC +1.5%

- US NAR JAN PENDING HOME SALES INDEX 122.8 V 126.4 IN DEC

MARKET SNAPSHOT

Key late session market levels:

- DJIA down 528.79 points (-1.65%) at 31426.41

- S&P E-Mini Future down 91 points (-2.32%) at 3830.75

- Nasdaq down 452 points (-3.3%) at 13140.14

- US 10-Yr yield is up 15.6 bps at 1.532%

- US Mar 10Y are down 53.5/32 at 133-15.5

- EURUSD up 0.0001 (0.01%) at 1.2167

- USDJPY up 0.4 (0.38%) at 106.27

- Gold is down $33.83 (-1.87%) at $1771.94

- EuroStoxx 50 down 20.71 points (-0.56%) at 3685.28

- FTSE 100 down 7.01 points (-0.11%) at 6651.96

- German DAX down 96.67 points (-0.69%) at 13879.33

- French CAC 40 down 14.09 points (-0.24%) at 5783.89

US TSY SUMMARY: Huge Range, Volatile Session, 10s Track Weaker Stocks

Unexpectedly hectic day for rates, broadly weaker 10Y futures in lock-step with S&P futures on the day. The dramatic rise in Tsy yields has been fast if not a smooth transition since the start of the year: 10YY 0.9132% Jan 1 to 1.6085% high post auction, 30YY 1.8347% on Jan 1 to 2.3944% high.

- Yld curves mixed: short end steeper while 5s30s fell below 148.5 from 165.39 high earlier. Yields had pull back from 1Y highs/futures pared losses after mixed data: lower than expected weekly claims, stronger durables, softer GDP.

- Second half trigger: Tsys gapped lower after a terrible $62B 7Y Note auction tailed 4bp: US Tsy $62B 7Y Note auction (91282CBP5) drew high yield 1.195% vs. 1.155% WI; (had stopped through last month on high yield of 0.754% vs. 0.757% WI) ; 2.30 bid/cover vs. 2.04 prior.

- Dealers are cranking out their negative convexity trigger points ahead of today's move -- may need to expand their horizons: one stated convexity selling doesn't start until doesn't start until around 1.35% 10YY and tapers off at 1.60% -- which happens to be near TODAY's range for 10YY! TD Security had it right unwinding their long 5s30s steepener at 159 (165 high today, it collapsed to 148.456 low, 150.652 last).

- Official central bank line: not worried about a spike in inflation etc, while mkt basically right where we were at start of pandemic. Opinions vary around banks trying to talk economy up after telegraphing willing to let market run hot for a while -- remains to be seen. No surprise reveal from NY Fed Williams on YCC or other measures after today's volatile session.

- The 2-Yr yield is up 4.9bps at 0.172%, 5-Yr is up 21.8bps at 0.8181%, 10-Yr is up 15.5bps at 1.5303%, and 30-Yr is up 6.3bps at 2.2956%.

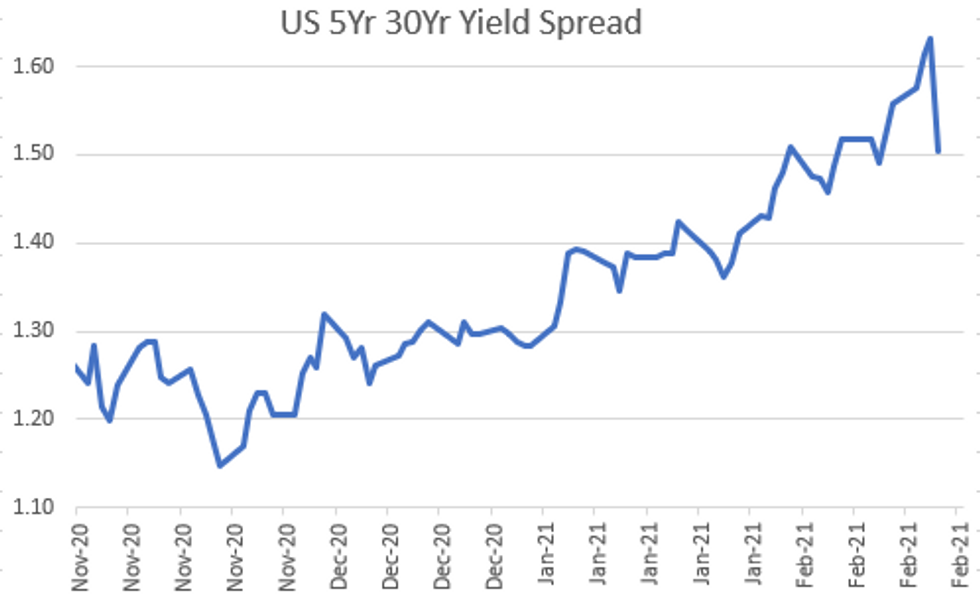

US TSY FUTURES CLOSE: 5s30s Yld Curve Reversal: 5s Underperform Bond Rout

Broadly weaker/off lows. Already weaker, moving in step with equities, Tsys gapped lower after $62B 7Y Note auction tailed a full 4Bp. Yld curves mixed: short end steeper while 5s30s that had tapped Aug 2014 high around 166.0 yesterday fell to 147.184 low today. Reminder, June takes lead quarterly tomorrow.

- 3M10Y +9.88, 143.894 (L: 133.166 / H: 156.542)

- 2Y10Y +6.639, 131.506 (L: 124.722 / H: 141.882)

- 2Y30Y -0.868, 209.683 (L: 209.683 / H: 220.388)

- 5Y30Y -15.304, 147.812 (L: 147.184 / H: 165.39)

- Current futures levels:

- Mar 2Y down 3/32 at 110-12.25 (L: 110-10.75 / H: 110-15.25)

- Mar 5Y down 27.25/32 at 124-11.25 (L: 124-00.25 / H: 125-08)

- Mar 10Y down 1-10/32 at 133-27 (L: 133-02.5 / H: 135-09)

- Mar 30Y down 1-12/32 at 160-5 (L: 157-23 / H: 161-24)

- Mar Ultra 30Y down 2-1/32 at 187-30 (L: 183-29 / H: 190-10)

US EURODOLLAR FUTURES CLOSE: Futures Crater, Massive Volumes, March'23 Over 1M!

ED futures followed Tsy sharply lower Thu, massive volumes: 10.1M aggregate while Green Mar'23 lead with just over 1.089M after the close. Not wasting much time pricing in economic rebound and tighter policy. Lead quarterly -0.020 late, weaker since 3M LIBOR set +0.00075 to 0.19050% (+0.01525/wk).

- Mar 21 -0.020 at 99.815

- Jun 21 -0.015 at 99.830

- Sep 21 -0.010 at 99.815

- Dec 21 -0.010 at 99.770

- Red Pack (Mar 22-Dec 22) -0.115 to -0.02

- Green Pack (Mar 23-Dec 23) -0.255 to -0.14

- Blue Pack (Mar 24-Dec 24) -0.255 to -0.22

- Gold Pack (Mar 25-Dec 25) -0.21 to -0.17

US TSY: Short Term Rates

US DOLLAR LIBOR: Latest settles:

- O/N +0.00025 at 0.08038% (+0.00225/wk)

- 1 Month +0.00063 to 0.11513% (-0.00032/wk)

- 3 Month +0.00075 to 0.19050% (+0.01525/wk) ** (Record Low of 0.17525% on 2/19/21)

- 6 Month +0.00125 to 0.20063% (+0.00463/wk)

- 1 Year +0.00225 to 0.28025% (-0.00625/wk)

- Daily Effective Fed Funds Rate: 0.07% volume: $70B

- Daily Overnight Bank Funding Rate: 0.07%, volume: $212B

- Secured Overnight Financing Rate (SOFR): 0.02%, $870B

- Broad General Collateral Rate (BGCR): 0.01%, $371B

- Tri-Party General Collateral Rate (TGCR): 0.01%, $340B

- (rate, volume levels reflect prior session)

- Tsy 20Y-30Y, $1.735B accepted vs. $5.530B submission

- Next scheduled purchases:

- Fri 2/26 1010-1030ET: Tsy 0Y-2.25Y, appr 12.825B

PIPELINE: Daimler Launched Despite Market Vol

- Date $MM Issuer (Priced *, Launch #)

- 02/25 $3B #Daimler Finance $1.5B 3Y +48, $1B 5Y +70, $500M 10Y +95

- 02/25 $1.25B #Truist Financial 6NC5 fix-FRN +50

- 02/25 $900M #Williams Cos 10Y +115

- 02/25 $520M *Development Bank Japan (DBJ) 3Y +14

FOREX: A Volatile US Yield Curve Leads USD to Outperform

After a shaky start to the Thursday session, the US dollar rallied into the close after the US Treasury yield curve underwent an acute bout of volatility. After a sloppy 7yr bond auction, US 10y yields shot higher to the best levels since February last year and just above 1.6%. This prompted a short, sharp bout of risk-off, with the US dollar benefiting as a result.

- The poorest performers were commodity-tied currencies after oil markets flatlined near recent highs. This led the likes of NOK, AUD and NZD to underperform most others, and dragged AUD/USD off a new multi-year high.

- Spiralling equity markets on yield volatility fears fed into a strong move for haven currencies, with CHF and JPY close to the top of the pile.

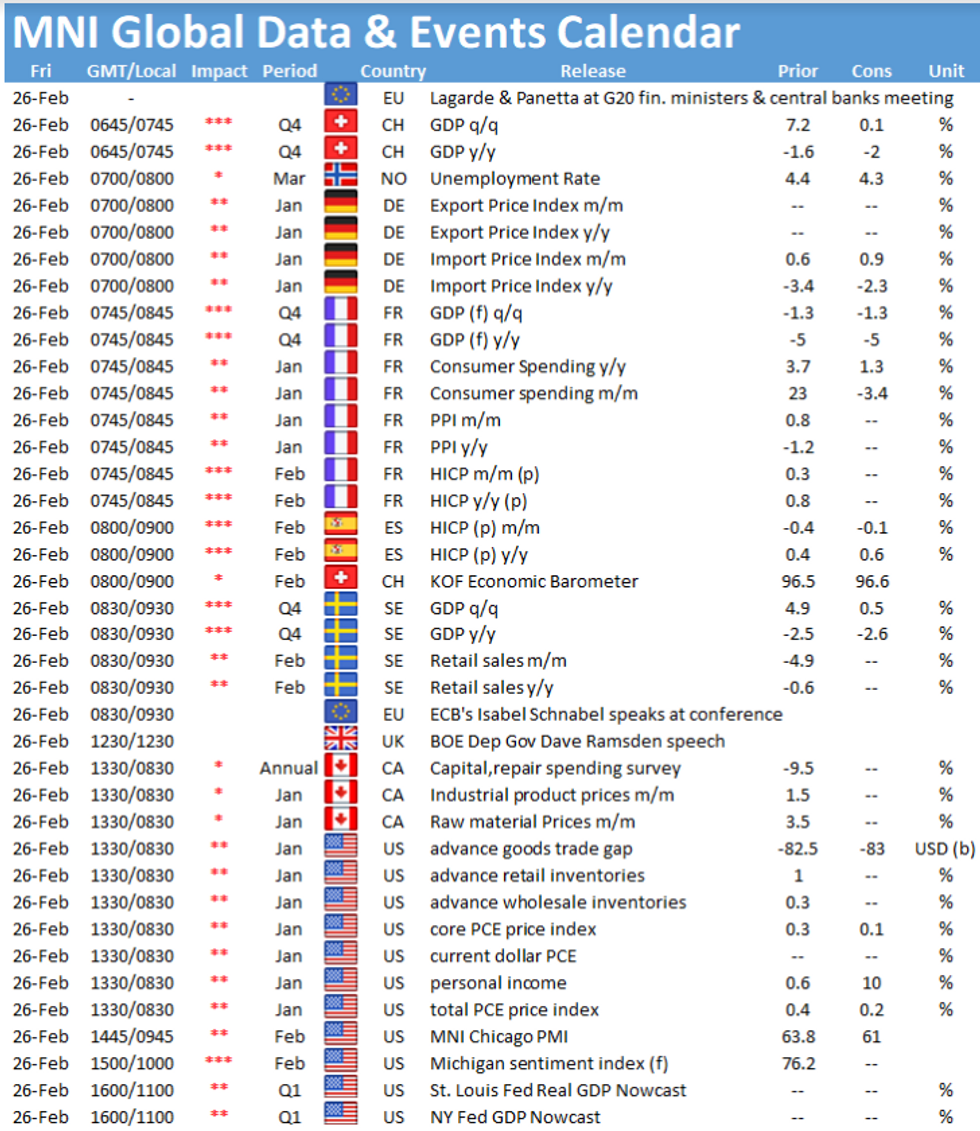

- Focus Friday turns to French prelim CPI, US trade balance and personal income/spending numbers for January and the MNI Chicago PMI. Speakers include ECB's Schnabel and BoE's Haldane & Ramsden.

BONDS/EGBs-GILTS CASH CLOSE: Tough Day For The Belly

Bunds and Gilts found a bit of a footing toward the end of Thursday's session, but make no mistake that it was a very tough day across the curves. BTP spreads widened too, with French 10-Yr yields going positive for the first time since June 2020.

- While the main theme globally was belly/10-Yr weakness, perhaps notable was the relatively stronger performance in 30-Yr Gilts - the UK curve bear flattened as BoE cuts were priced out.

- Italy saw lowest cover ratio for a 5-yr BTP since June 2020 (though this was somewhat expected due to large size); Tesoro released Green Bond framework.

- Bunds briefly ticked higher on comments by ECB's Lane reiterating the bank watching yields closely. But mixed confidence data this morning largely shrugged off.

- Friday sees some prelim inflation data and a few cenbank speakers (Schnabel, Haldane).

Closing yields/10-Yr Spreads to Bunds:

- Germany: The 2-Yr yield is up 3bps at -0.652%, 5-Yr is up 6.5bps at -0.545%, 10-Yr is up 7.2bps at -0.232%, and 30-Yr is up 3.5bps at 0.244%.

- UK: The 2-Yr yield is up 7.5bps at 0.107%, 5-Yr is up 8.8bps at 0.366%, 10-Yr is up 5.2bps at 0.784%, and 30-Yr is up 1.2bps at 1.389%.

- Italian BTP spread up 4bps at 103.1bps / Spanish spread up 1.3bps at 70.8bps

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.