Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- MNI US FED: Beige Book: Slight Expansion In Activity

- MNI US FED: Beige Book: Considerable Weakening In Ability To Pass Cost Increases On

- MNI US DATA: Mortgage Applications Rise Despite Higher Rates, Especially Jumbo Loan Rates:

US

US FED (MNI): Beige Book: Slight Expansion In Activity: "Overall economic activity expanded slightly, on balance, since late February. Ten out of twelve Districts experienced either slight or modest economic growth—up from eight in the previous report, while the other two reported no changes in activity.

- Consumer spending barely increased overall, but reports were quite mixed across Districts and spending categories. Several reports mentioned weakness in discretionary spending, as consumers’ price sensitivity remained elevated."

US FED (MNI): Beige Book: Considerable Weakening In Ability To Pass Cost Increases On: Dovish tinges with a considerable weakening in recent months in ability to pass cost increases on to consumers, contracts expecting that inflation would hold steady at at slow pace moving forward and upside risks mostly confined to manufacturers.

NEWS

US (MNI): Johnson Bucks Conservatives, Targets Saturday For Foreign Aid Vote: House Speaker Mike Johnson (R-LA) has issued a statement confirming that he will press forward with his plan to hold votes on new supplemental aid for Ukraine, Israel, and allies in the Indo-Pacific. Votes are expected to take place on Saturday evening. Johnson says he will hold votes on four separate bills under one House rule. Johnson will need Democrat support to move the package out of the Rules Committee, which they are likely to provide.

US-CHINA (MNI): USTR Tai: We Have To Take Early, Decisive Action On China Overcapacity: US Trade Representative Katherine Tai said, in testimony to the Senate Finance Committee on President Biden 2024 trade agenda, that the US has to take "decisive" action to counter China's overcapacity in electric vehicles, solar panel, and other clean energy goods.

Ireland, Luxembourg Resist Joint EU Supervision Proposal (MNI): Differences over the European Union's Capital Markets Union project look set to divide leaders at a summit starting in Brussels on Wednesday, officials told MNI, as countries with significant stock markets push to accelerate progress while others including Luxembourg and Ireland resist any moves towards joint rules on supervision and corporate taxation.

BOE (MNI): VIEW CHANGE: RBC still looks for first cut in August but then shallower cutting cycle: RBC continues to look for the first cut in August but rather than 100bp of cuts this year, it now expects 2x25bp cuts in August and November to leave Bank Rate at 4.75% by end-2024. It continues to look for 50bp of cuts in 2025 to leave the terminal rate 50bp higher than previously at 4.25%.

BOE (MNI): VIEW CHANGE: Nomura looks for shallower rate cut path but lower terminal rate: Nomura notes that "while we remain comfortable with our view of an August BoE rate cut , sticky inflation and wages suggest back-to-back cuts are more difficult to justify." Nomura changes its call to look for cuts every other meeting (MPR meetings) until Bank Rate reaches a terminal 3.75% by end-2025.

US/RUSSIA (MNI): Adeyemo: Working Towards Unlocking Russian Sov. Assets To Aid UKR: Wires carrying comments from US Deputy Treasury Secretary Wally Adeyemo stating that the G7 is, "working towards unlocking value of Russian sovereign assets to aid Ukraine," describing the discussions as a "work in progress."

ISRAEL (MNI): Ex-Mossad Chief-'Everything On Table' In Response To Iran Strikes: Sky News reporting comments from former Mossad Director of Intelligence Zohar Palti regarding potential Israeli retaliation to Iran's drone/missile strikes over the weekend.

IRAN (MNI): Speculation IAEA Head Could Visit Amid Regional Tensions: Iran's state-run Hamshahri reporting that International Atomic Energy Agency (IAEA) Director General Rafael Grossi could visit the country in the near future. Head of the Iranian Atomic Energy Organization Mohammed Eslami claimed that the visit would come "soon".

TURKEY (MNI): Erdogan To Host Hamas Leader After Blaming Netanyahu For Iranian Strikes: Reports claiming that President Recep Tayyip Erdogan intends to host Chairman of the Hamas Political Bureau (effectively Hamas' leader) Ismail Haniyeh in Turkey over the weekend.

US TSYS Near Late Session Highs Ahead Thu's Weekly Claims, Existing Home Sales

- Treasuries marched off early session lows Wednesday, following EGBs lead despite pickup in inflation metrics. Jun'24 10Y marked 108-08 session high well after futures rallied following the second consecutive stop for the 20Y auction reopen: 4.818% high yield vs. 4.840%.

- Limited economic data, US mortgage applications rose despite higher rates: seasonally adjusted 3.3% last week after a flag week prior.

- Fed Beige Book: overall economic activity expanded slightly on balance since late February. Ten out of twelve Districts experienced either slight or modest economic growth—up from eight in the previous report, while the other two reported no changes in activity.

- Short end rates lagged the rally while Projected rate cut pricing steady vs. late Tuesday levels: May 2024 steady at -2.6% w/ cumulative -0.6bp at 5.322%; June 2024 steady at -16.2% w/ cumulative rate cut -4.7bp at 5.282%. July'24 cumulative at -12.6bp, Sep'24 cumulative -24.9bp.

- Thursday Data Calendar: Weekly Claims, Exist Home Sales, Fed Speak from Fed Gov Bowman, NY Fed Williams, Atlanta Fed Bostic and Boston Fed Collins.

OVERNIGHT DATA

US DATA (MNI): Mortgage Applications Rise Despite Higher Rates, Especially Jumbo Loan Rates: MBA mortgage applications increased a seasonally adjusted 3.3% last week after a flag week prior.

- Purchases bounced (+5.0% after -4.7%) whilst refis pausing after a strong increase (+0.5% after +9.9%).

- The overall increase came despite the conforming 30Y mortgage rate increasing 12bps to 7.13% for its highest since early December.

- In a sign of some tightening over the week, the regular to jumbo spread fell from -12bps to -27bps (the jumbo loan rate increased 27bps over the week), its lowest since mid-Dec and before that in early 2021.

US (MNI): NY Fed Report Shows Projection With Portfolio Reduction Ending 2025: The NY Fed’s annual report on its open market operations during 2023 (see here) shows projections with portfolio reduction stopping in 2025 and reserves bottoming out at $2.5.3tn in 2026.

MARKETS SNAPSHOT

- Key market levels of markets in late NY trade:

- DJIA down 27.47 points (-0.07%) at 37768.6

- S&P E-Mini Future down 21.25 points (-0.42%) at 5071

- Nasdaq down 135.9 points (-0.9%) at 15728.14

- US 10-Yr yield is down 7.8 bps at 4.5894%

- US Jun 10-Yr futures are up 14.5/32 at 108-4

- EURUSD up 0.0048 (0.45%) at 1.0667

- USDJPY down 0.34 (-0.22%) at 154.38

- WTI Crude Oil (front-month) down $2.66 (-3.12%) at $82.70

- Gold is down $14.6 (-0.61%) at $2368.14

- European bourses closing levels:

- EuroStoxx 50 down 2.86 points (-0.06%) at 4914.13

- FTSE 100 up 27.63 points (0.35%) at 7847.99

- German DAX up 3.79 points (0.02%) at 17770.02

- French CAC 40 up 48.9 points (0.62%) at 7981.51

US TREASURY FUTURES CLOSE

- 3M10Y -9.755, -81.936 (L: -83.37 / H: -72.04)

- 2Y10Y -2.512, -34.697 (L: -35.098 / H: -30.85)

- 2Y30Y -0.33, -23.1 (L: -23.896 / H: -19.545)

- 5Y30Y +2.474, 8.295 (L: 5.204 / H: 11.09)

- Current futures levels:

- Jun 2-Yr futures up 1.75/32 at 101-18.875 (L: 101-14.7487999999998 / H: 101-20.125)

- Jun 5-Yr futures up 8/32 at 105-7.25 (L: 104-26.75 / H: 105-10)

- Jun 10-Yr futures up 14/32 at 108-3.5 (L: 107-15.5007999999998 / H: 108-08)

- Jun 30-Yr futures up 25/32 at 114-24 (L: 113-20 / H: 114-31)

- Jun Ultra futures up 1-02/32 at 121-5 (L: 119-21 / H: 121-11)

US 10Y FUTURES TECHS: (M4) Bears Remain In The Driver’s Seat

- RES 4: 110-06 High Apr 4 and the 50-day EMA

- RES 3: 109-26+ High Apr 10

- RES 2: 109-02/12 Low Apr 8 / 20-day EMA

- RES 1: 108.25+ High Apr 12

- PRICE: 108-06 @ 1420 ET Apr 17

- SUP 1: 107-13+ Low Apr 16

- SUP 2: 107-07+ 76.4% of the Oct - Dec ‘23 bull leg (cont)

- SUP 3: 106-27 2.764 proj of Dec 27 - Jan 19 - Feb 1 price swing

- SUP 4: 106-08 3.00 proj of Dec 27 - Jan 19 - Feb 1 price swing

A bear cycle in Treasuries remains in play and this week’s move lower reinforces the current bear theme. The move down has resumed this year’s downtrend and in the process a number of short-term support points have been breached. Scope is seen for a move to 107.07+ next, a Fibonacci retracement. Initial resistance has been defined at 109-25+, the Apr 12 high. Key short-term resistance is 110-06, the Apr 4 high.

SOFR FUTURES CLOSE

- Jun 24 steady at 94.740

- Sep 24 +0.005 at 94.905

- Dec 24 +0.010 at 95.10

- Mar 25 +0.025 at 95.295

- Red Pack (Jun 25-Mar 26) +0.045 to +0.075

- Green Pack (Jun 26-Mar 27) +0.070 to +0.080

- Blue Pack (Jun 27-Mar 28) +0.065 to +0.070

- Gold Pack (Jun 28-Mar 29) +0.065 to +0.070

SOFR FIXES AND PRIOR SESSION REFERENCE RATES

SOFR Benchmark Settlements:

- 1M -0.00007 to 5.31882 (-0.00047/wk)

- 3M -0.00037 to 5.32656 (-0.00100/wk)

- 6M -0.00328 to 5.30154 (-0.00183/wk)

- 12M -0.00992 to 5.21009 (+0.01097/wk)

- Secured Overnight Financing Rate (SOFR): 5.31% (-0.01), volume: $1.809T

- Broad General Collateral Rate (BGCR): 5.31% (+0.00), volume: $705B

- Tri-Party General Collateral Rate (TGCR): 5.31% (+0.00), volume: $696B

- (rate, volume levels reflect prior session)

- Daily Effective Fed Funds Rate: 5.33% (+0.00), volume: $83B

- Daily Overnight Bank Funding Rate: 5.32% (+0.00), volume: $244B

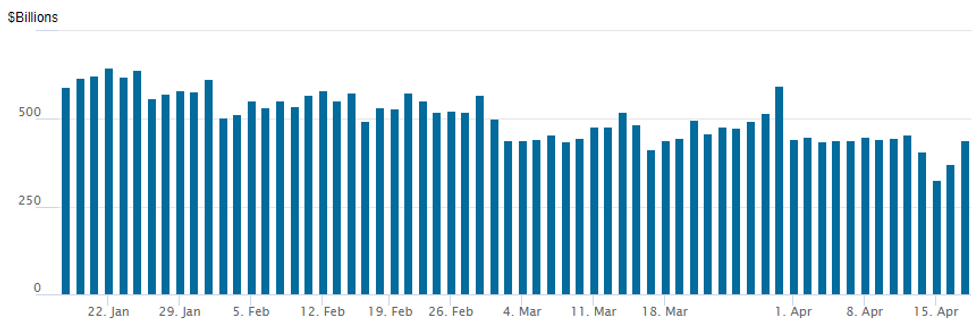

FED Reverse Repo Operation: Back Over $400B

NY Federal Reserve/MNI

- RRP usage climbs back over $400B to $440.508B vs. $371.554B yesterday. Compares to $327.066B on Monday -- the lowest level since mid-May 2021 as desks cited Federal tax deadline for the drop.

- Meanwhile, the latest number of counterparties surges to 89 vs. 68 prior.

PIPELINE $1B RBC 60NC5 Bond Launched

$14.5B to price Wednesday

- Date $MM Issuer (Priced *, Launch #)

- 4/17 $8B #Morgan Stanley $1.5B 4NC3 +90, $1B 4NC3 SOFR+102, $2.5B 6NC5 +105, $3B 11NC10 +125

- 4/17 $3B *KFW 2Y +16

- 4/17 $2.5B #Province of British Colombia 5Y SOFR+51

- 4/17 $1B #RBC 60NC5 7.5%

- 4/17 $1.25B Jane Street 7NC3 investor calls

EGBs-GILTS CASH CLOSE: Gilts Rally Despite Robust Inflation Data

Gilts outperformed Bunds Wednesday despite stronger-than-expected UK CPI data

- An initial post-UKI CPI sell off in Gilts proved limited and yields began heading decisively lower in the early afternoon.

- Overall the gains in core FI were more of a bounce from extreme weakness earlier in the week, with a risk-off tone and softer energy prices also contributing.

- BoE's Greene sounded slightly more dovish on the inflation situation than expected.

- The German and UK curves bull flattened, with Gilt yields closing on the lows as equities faded in late afternoon and BoE Gov Bailey commented that inflation was due for a "strong drop".

- Periphery spreads closed tighter on the day, led by BTPs.

- Multiple speakers feature Thursday, including ECB's Nagel.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is up 0.8bps at 2.944%, 5-Yr is down 1bps at 2.475%, 10-Yr is down 2.1bps at 2.465%, and 30-Yr is down 2.8bps at 2.599%.

- UK: The 2-Yr yield is down 1.3bps at 4.463%, 5-Yr is down 1.7bps at 4.185%, 10-Yr is down 3.8bps at 4.261%, and 30-Yr is down 5.5bps at 4.694%.

- Italian BTP spread down 1.4bps at 144.5bps / Spanish bond spread down 0.6bps at 83.8bps

FOREX G10 Ranges Relatively Subdued Despite Lower Core Yields, EM FX Recovers

- Lower core rates on Wednesday have had little impact on G10 currencies throughout the session, with any dollar weakness perhaps offset by the renewed negative sentiment across equity markets. The USD index sits moderately in the red, however, has broadly been consolidating at its most recent lofty levels.

- USDJPY sprung to life late in the session with a small downtick to print fresh session lows at 154.17. The move likely driven by a breach of the overnight lows following an extremely tight trading range on Wednesday. Relatively low volumes support this theory, and the move is much less aggressive than yesterday's sharp selloff during US hours, exacerbated by markets speculating over potential MOF action.

- Overall, the USDJPY uptrend is overbought, however, this is not - for now - a concern for bulls. Sights are on the 155.00 handle next. Support lies much lower at 152.00 and 151.84, 20-day EMA.

- Despite the equity weakness, AUD and NZD are outperforming although these are similarly partial reversals from the steep selloffs this week. In similar vein, emerging market currencies such as PLN, MXN and CLP have traded on the front foot as short-term price action stabilised.

- GBP was only moderately in the green despite the above-expectation CPI data. A bearish theme in GBPUSD remains intact and scope is seen for an extension towards 1.2364, a Fibonacci retracement.

- Fed’s Mester is due to speak late on Wednesday before Australia unemployment data headlines the Thursday APAC calendar. US jobless claims, Philly Fed manufacturing and existing home sales are all scheduled.

THURSDAY DATA CALENDAR

| Date | GMT/Local | Impact | Flag | Country | Event |

| 17/04/2024 | 2315/1915 |  | US | Fed Governor Michelle Bowman | |

| 18/04/2024 | 0130/1130 | *** |  | AU | Labor Force Survey |

| 18/04/2024 | 0715/0915 |  | EU | ECB's De Guindos ECB Report Presentation | |

| 18/04/2024 | 0800/1000 | ** | | EU | Current Account |

| 18/04/2024 | 0900/1100 | ** | | EU | Construction Production |

| 18/04/2024 | 1230/0830 | *** | | US | Jobless Claims |

| 18/04/2024 | 1230/0830 | ** | | US | WASDE Weekly Import/Export |

| 18/04/2024 | 1230/0830 | ** | | US | Philadelphia Fed Manufacturing Index |

| 18/04/2024 | 1305/0905 | | US | Fed Governor Michelle Bowman | |

| 18/04/2024 | 1315/0915 | | US | New York Fed's John Williams | |

| 18/04/2024 | 1315/0915 | | US | Fed's Miki Bowman | |

| 18/04/2024 | 1400/1000 | *** | | US | NAR existing home sales |

| 18/04/2024 | 1430/1030 | ** | | US | Natural Gas Stocks |

| 18/04/2024 | 1500/1100 | | US | Atlanta Fed's Raphael Bostic | |

| 18/04/2024 | 1500/1600 |  | UK | BOE's Greene with Atlantic Council GeoEconomics Center | |

| 18/04/2024 | 1530/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 18/04/2024 | 1530/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 18/04/2024 | 1700/1300 | ** | | US | US Treasury Auction Result for TIPS 5 Year Note |

| 18/04/2024 | 1730/1930 | | EU | ECB's Schnabel Speaks At 2024 EU-US Symposium | |

| 18/04/2024 | 2145/1745 | | US | Atlanta Fed's Raphael Bostic |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.