Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

US TSYS: Low Mkt Conviction Ahead Nov FOMC

Tsys currently mixed after a strong start and ongoing debate over step-down to a 50bp hike in December as data cools. Little new in WSJ's Fed watcher Timiraos article overnight.- Support evaporates after midmorning JOLTS data (job openings rise unexpectedly to 10.717M vs. 9.75M est (above prior 10.053M) showed labor market remains tight - dampening speculation over step-down to 50bp hike at Dec FOMC.

- Lack of strong convictions over forward policy evident in market swings ahead Wednesday's FOMC at 1400ET and Chair Powell's presser at 1430ET. Friday sees latest employment data for October.

- Case in point: Bonds had started to bounce off midday lows following misinterpreted BBG headline: BIDEN HAS ENDORSED FED'S POLICY PIVOT: BERNSTEIN (Jared Berstein, sits on the White House Council of Economic Advisers).

- Since the Fed is in blackout ahead Wed's FOMC, there has been no mention of a policy pivot which spurred confusion until Bbg ran correction: BIDEN ENDORSED FED PIVOT TO TIGHTEN THIS YR, Bbg. Tsys receded again despite the continued use of "PIVOT" in the statement.

- At the moment: 2-Yr yield is up 6.2bps at 4.5447%, 5-Yr is up 3.9bps at 4.267%, 10-Yr is up 1.3bps at 4.0606%, and 30-Yr is down 4bps at 4.1235%.

US

US TSY: US Tsy Refunding, following 4 consecutive rounds of reductions, Treasury is widely expected to keep auction sizes basically unchanged in the upcoming quarter.

- There are risks that there are reductions to 20Y Bond sizes, and increases to TIPS sizes.

- The other main area of focus is on potential Treasury buybacks, but an announcement may have to wait until February at least.

- Our Deep Dive includes an estimated U.S. issuance schedule, review of October's auctions, and sell-side Refunding expectations.

- "I think we're going to end up in contraction, but that doesn't mean we're headed for a recession," he said. "We are seeing a gradual shift."

- Fiore's view of the manufacturing sector has darkened since the summer. The ISM manufacturing PMI is likely to settle in a range around 48 to 52 but not crater further to the low 40s, he said in an interview. For more see MNI Policy main wire at 1351ET.

UK

BOE: The Bank of England must keep raising interest rates aggressively for the foreseeable future, possibly bringing its policy rate up to 6% to deal with increasingly-entrenched inflation, former Monetary Policy Committee member Willem Buiter told MNI.

- The BOE meets this week under the shadow of gilt market turbulence that forced an emergency central bank intervention to protect pension funds, and is expected to deliver a 75-basis-point rate hike.

- “The prospect for the foreseeable future, for all of 2023, is for significantly higher interest rates. In the UK, certainly higher than 5, possibly up to 6%,” said Buiter, also former Citigroup global chief economist, in an interview with MNI’s FedSpeak podcast.

BOE: The MNI Markets team expects a 75bp hike at this week’s MPC meeting, albeit with risks of a smaller 50bp hike.

- UK markets have moved back to close to their prevailing levels ahead of the September MPC meeting but with inflation still in double digits and still flagging concerns in the Bank’s DMP surveys, and still a great deal of uncertainty surrounding the magnitude of fiscal consolidation, we think that the majority of the MPC will not want to disappoint a strong analyst and market consensus of a 75bp hike.

- With growth already starting to falter, however, we do think there is a risk that the Bank delivers a smaller 50bp hike (but do not see the need for a larger 100bp hike at this stage).

OVERNIGHT DATA

- US OCT S&P MANUF. PMI FINAL 50.4 (FLSH 49.9); SEP 52.0

- US SEP CONSTRUCT SPENDING +0.2%

- US SEP PRIVATE CONSTRUCT SPENDING +0.4%

- US SEP PUBLIC CONSTRUCT SPENDING -0.4%

- US ISM OCT MANUF PURCHASING MANAGERS INDEX 50.2

- US ISM OCT MANUF PRICES PAID INDEX 46.6

- US ISM OCT MANUF NEW ORDERS INDEX 49.2

- US ISM OCT MANUF EMPLOYMENT INDEX 50

- US ISM OCT MANUF PRODUCTION INDEX 52.3

- US ISM OCT MANUF SUPPLIER DELIVERY INDEX 46.8

- US JOB OPENINGS ROSE TO 10.72MLN IN SEPT. FROM 10.28MLN

MARKETS SNAPSHOT

Key late session market levels:

- DJIA down 74.8 points (-0.23%) at 32662.29

- S&P E-Mini Future down 15.5 points (-0.4%) at 3868.25

- Nasdaq down 89.8 points (-0.8%) at 10899.26

- US 10-Yr yield is up 1.1 bps at 4.0585%

- US Dec 10Y are down 2/32 at 110-17

- EURUSD down 0.0003 (-0.03%) at 0.9879

- USDJPY down 0.48 (-0.32%) at 148.23

- WTI Crude Oil (front-month) up $1.85 (2.14%) at $88.37

- Gold is up $13.68 (0.84%) at $1647.29

- EuroStoxx 50 up 33.48 points (0.93%) at 3651.02

- FTSE 100 up 91.63 points (1.29%) at 7186.16

- German DAX up 85 points (0.64%) at 13338.74

- French CAC 40 up 61.48 points (0.98%) at 6328.25

US TSY FUTURES CLOSE

- 3M10Y -4.173, -8.602 (L: -24.664 / H: -7.876)

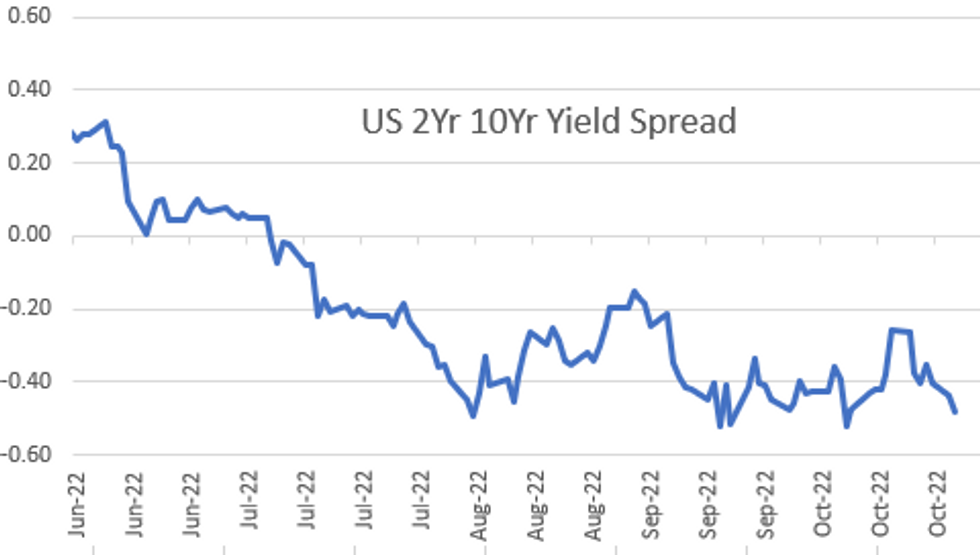

- 2Y10Y -4.536, -48.615 (L: -50.899 / H: -42.609)

- 2Y30Y -10.061, -42.427 (L: -43.82 / H: -29.966)

- 5Y30Y -7.834, -14.626 (L: -15.223 / H: -2.903)

- Current futures levels:

- Dec 2Y down 3.375/32 at 102-2.75 (L: 102-02.5 / H: 102-11.875)

- Dec 5Y down 3.5/32 at 106-15.5 (L: 106-15 / H: 107-07.75)

- Dec 10Y down 2.5/32 at 110-16.5 (L: 110-15.5 / H: 111-20.5)

- Dec 30Y up 14/32 at 120-30 (L: 120-25 / H: 122-28)

- Dec Ultra 30Y up 1-22/32 at 129-11 (L: 127-31 / H: 130-29)

US 10YR FUTURE TECHS: (Z2) Finds Support

- RES 4: 113-30 High Oct 4

- RES 3: 113-03 50-day EMA

- RES 2: 112-22+ High Oct 6

- RES 1: 111-31 High Oct 27

- PRICE: 111-14 @ 10:31 BST Nov 1

- SUP 1: 110-12 Low Oct 31

- SUP 2: 109-20/108-26+ Low Oct 25 / 21 and the bear trigger

- SUP 3: 108-06+ Low Oct 2007 (cont)

- SUP 4: 107.05 3.0% 10-dma envelope

Treasuries have recovered from Monday’s low. The primary trend direction remains down, however, attention is on resistance at 111-31, the Oct 27 high. A break of this hurdle would signal scope for an extension higher near-term and this would expose the 50-day EMA at 113-03. Monday’s low is first support where a break is required to signal scope for a deeper pullback, ahead of 108-26+, the Oct 21 low and a bear trigger.

US EURODOLLAR FUTURES CLOSE

- Dec 22 -0.010 at 94.880

- Mar 23 -0.075 at 94.675

- Jun 23 -0.085 at 94.710

- Sep 23 -0.085 at 94.915

- Red Pack (Dec 23-Sep 24) -0.06 to -0.045

- Green Pack (Dec 24-Sep 25) -0.04 to -0.03

- Blue Pack (Dec 25-Sep 26) -0.02 to -0.01

- Gold Pack (Dec 26-Sep 27) -0.005 to +0.015

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements:

- O/N -0.00428 to 3.05886% (-0.00500/wk)

- 1M +0.03671 to 3.84157% (+0.07386/wk)

- 3M -0.00058 to 4.45971% (+0.02014/wk) * / **

- 6M +0.00271 to 4.91857% (-0.01229/wk)

- 12M -0.00286 to 5.44543% (+0.07643/wk)

- * Record Low 0.11413% on 9/12/21; ** New 14Y high: 4.46029% on 10/31/22

- Daily Effective Fed Funds Rate: 3.08% volume: $82B

- Daily Overnight Bank Funding Rate: 3.06% volume: $249B

- Secured Overnight Financing Rate (SOFR): 3.05%, $1.075T

- Broad General Collateral Rate (BGCR): 3.00%, $414B

- Tri-Party General Collateral Rate (TGCR): 3.00%, $386B

- (rate, volume levels reflect prior session)

FED Reverse Repo Operation

NY Federal Reserve/MNI

NY Fed reverse repo usage fell to $2,200.5109B w/ 102 counterparties vs. $2,275.459B in the prior session. Prior record high stands at $2,425.910B on Friday, September 30.

Ford Motor Co, State Street Bank Launched Earlier

- Date $MM Issuer (Priced *, Launch #)

- 11/01 $1.5B #Ford Motor Co 5Y 7.35%

- 11/01 $1B #State Street Bank $500M 4NC3 +125, $500M 6NC5 +155

EGBs-GILTS CASH CLOSE: Short-End Gilts Rally As BoE QT Begins

Short-end Gilt yields fell sharply Tuesday in a bull steepening move on the UK curve. The German curve twist flattened, with periphery spreads slightly tighter.

- Yields fell sharply across the board on the open, but reversed from session lows after midday when a high US job openings figure dealt a late hawkish twist to Wednesday's Fed decision.

- German yields sustained their rise, though Gilts rallied toward the close after the BoE sold short-dated instruments in its first QT operation.

- All attention turns to the Fed decision Wednesday, though one eye remains on the BoE (and its likely 75bp hike) Thursday - our preview ("Downside Risks To 75bp") went out this afternoon.

CLOSING YIELDS / 10-YR PERIPHERY EGB SPREADS TO GERMANY:

- Germany: The 2-Yr yield is up 0.5bps at 1.941%, 5-Yr is down 2.2bps at 1.983%, 10-Yr is down 1.1bps at 2.131%, and 30-Yr is up 0.5bps at 2.14%.

- UK: The 2-Yr yield is down 14.8bps at 3.185%, 5-Yr is down 12.7bps at 3.504%, 10-Yr is down 4.6bps at 3.47%, and 30-Yr is down 2.2bps at 3.586%.

- Italian BTP spread down 2.7bps at 213.1bps / Spanish down 0.1bps at 108.2bps

FOREX: Greenback Erases Early Losses, EURUSD Approaches Support

- Despite the US Dollar showing early signs of weakness on Tuesday, a large rise in Jolts job openings and firm ISM Manufacturing data in the US provided solid impetus for a greenback recovery in the latter half of Tuesday trade.

- The USD index had fallen roughly 0.75%, making new marginal lows for the week before recovering and extending gains on the data. There was one brief dip for the greenback (of around 35 pips) on a misinterpreted headline over Biden endorsing the Fed’s pivot, however, USD strength immediately resumed.

- EURUSD has settled back below the 0.99 handle and support to watch is 0.9830, the former bear channel resistance, which was broken last week.

- Technically, trend conditions remain bullish and the recent pullback is considered corrective. It is worth noting that there are some large option expiries between 0.99 and 1.00 which may limit the pairs downside at this juncture, especially given the proximity to the FOMC and US jobs data later this week.

- Showing similar underperformance to the Euro is AUD, following the RBA meeting overnight and being weighed on by softer equity indices. The Reserve Bank of Australia raised rates 25bp to 2.85%, warning inflation will peak at "around" 8% later this year as it cut its growth forecasts out to 2024. Despite holding up for much of the session, AUDUSD crashed back below 0.64 following the US data, trading to within close proximity of initial support at 0.6368, the Oct 31 low.

- Interestingly, AUDNZD traded at the lowest level since May 25, trading within 4 pips of noted support at 1.0922.

- In emerging markets, the Brazilian Real continued to outperform after an election victory for Former President Lula. Most recent rhetoric suggests that President Bolsonaro intends there to be a peaceful transition which continues to underpin BRL strength. USDBRL (-1.42%) has now breached support at 5.1121, the Oct 4 low.

- Final PMI releases in Europe on Wednesday as well as ADP employment data in the US. However, all focus will be on the November FOMC decision and Chair Powell’s press conference.

Wednesday Data Calendar

| Date | GMT/Local | Impact | Flag | Country | Event |

| 02/11/2022 | 0001/0001 | * |  | UK | BRC Monthly Shop Price Index |

| 02/11/2022 | 0030/1130 | ** |  | AU | Lending Finance Details |

| 02/11/2022 | 0030/1130 | * | | AU | Building Approvals |

| 02/11/2022 | 0700/0800 | ** |  | DE | Trade Balance |

| 02/11/2022 | 0815/0915 | ** |  | ES | IHS Markit Manufacturing PMI (f) |

| 02/11/2022 | 0845/0945 | ** |  | IT | IHS Markit Manufacturing PMI (f) |

| 02/11/2022 | 0850/0950 | ** |  | FR | IHS Markit Manufacturing PMI (f) |

| 02/11/2022 | 0855/0955 | ** | | DE | Unemployment |

| 02/11/2022 | 0855/0955 | ** | | DE | IHS Markit Manufacturing PMI (f) |

| 02/11/2022 | 0900/1000 | ** |  | EU | IHS Markit Manufacturing PMI (f) |

| 02/11/2022 | 1100/0700 | ** |  | US | MBA Weekly Applications Index |

| 02/11/2022 | 1215/0815 | *** | | US | ADP Employment Report |

| 02/11/2022 | 1400/1000 | ** | | US | housing vacancies |

| 02/11/2022 | 1430/1030 | ** | | US | DOE weekly crude oil stocks |

| 02/11/2022 | 1515/1115 |  | CA | BOC director Ron Morrow speaks on payments supervision | |

| 02/11/2022 | 1800/1400 | *** | | US | FOMC Statement |

| 03/11/2022 | 2200/0900 | * | | AU | IHS Markit Final Australia Services PMI |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.